PBOC Cuts Post Close as Hong Kong Internet Stocks Rebound, Week in Review

3 Min. Read Time

Week in Review

- On Tuesday, the China Cyberspace Administration initiated an investigation into Didi’s data practices. The regulator has suspended new users from downloading the app while it completes a data security review, though current users can still access the app.

- Mainland markets saw growth outperform, led by clean energy-related stocks such as lithium, rare earth, solar, electric vehicles, and STAR Board securities after the National Development and Reform Commission said more policy and financial support is needed for China to meet its carbon and environmental goals on Wednesday.

- Several internet companies were fined $77k for past mergers and acquisitions this Thursday. Investors appear to be stringing several events into a single narrative though they may not be directly related. The regulation has had no effect on Q4 2020 or Q1 2021 earnings.

Key News

Asian equities followed US equities lower with some concern about the delta variant threatening the global reopening. Nonetheless, Hong Kong rebounded led by Chinese internet names. At the market’s open, June inflation data (year-over-year) was released with CPI declining to 1.1% from last month’s 1.3% and expectations of 1.2%. PPI declined slightly from last month’s 9% to 8.8%, in line with expectations with many opining that PPI has likely peaked.

After the close, we had June’s new loans and aggregate financing both beat expectations and rising from last months, which is indicative of a growing economy. We also had the PBOC cutting bank’s reserve requirement ratio (RRR), the amount of money banks need to hold on the books, from 12.5% to 12% (US banks' RRR is currently zero in response to the pandemic). This is expected to release RMB 1 trillion of additional lending for businesses. The nattering nabobs of negativity will say "look at the aggressive move", which must mean the economy is weakening. Not necessarily, as the action is getting ahead of economic data, which will slow due to the year-over-year comparison.

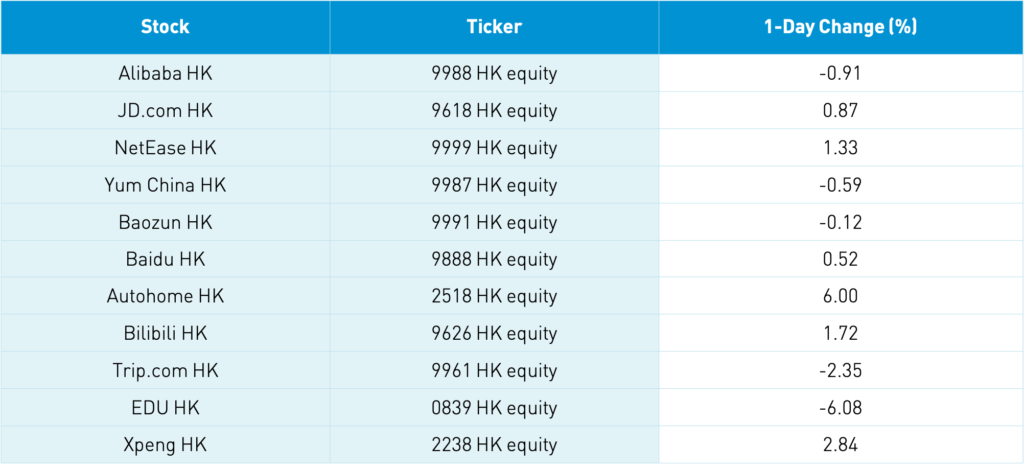

Hong Kong saw bottom fishing in internet stocks, though fintech and education/tutoring are still in the pain cave. Healthcare had a nice rebound in Hong Kong while electric vehicle (EV) ecosystem names, particularly metals, had a strong day on expectations for strong 2021 EV sales in both Hong Kong and Mainland China.

In the Mainland, liquor stocks and tech saw profit-taking. CNY appreciated a touch versus the US dollar while Mainland bonds sold off a touch along with copper. FTSE Russell indexes added Didi to its indexes at Wednesday’s close. Post-close, MSCI confirmed that Didi will be added to its indexes with trading occurring at the close next Wednesday.

H-Share Update

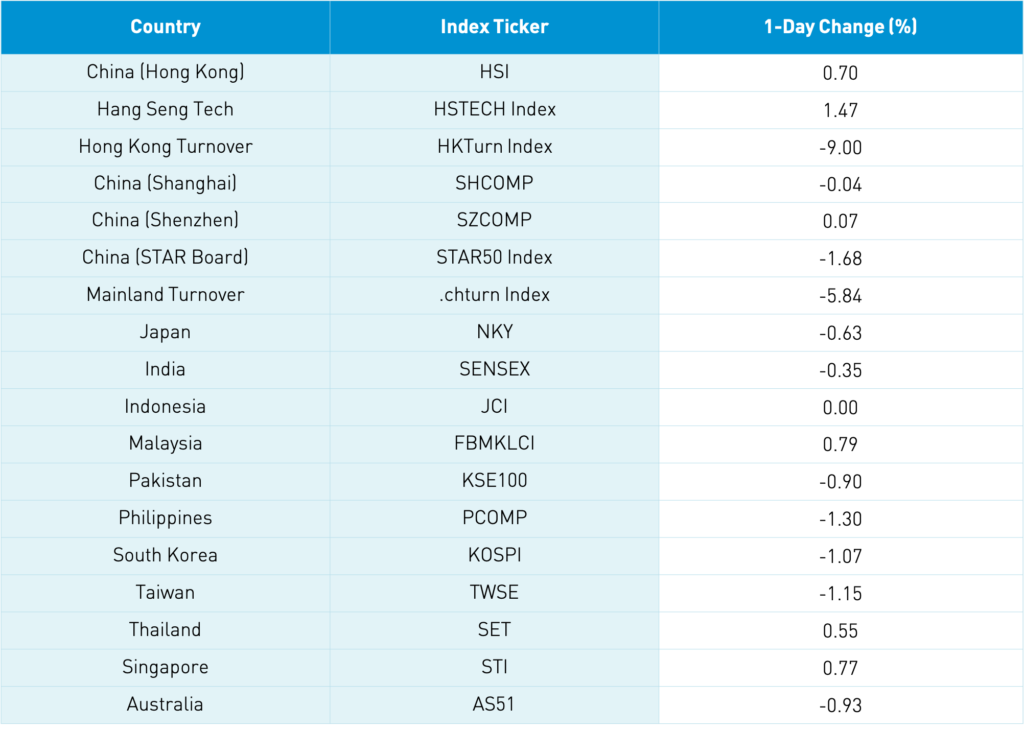

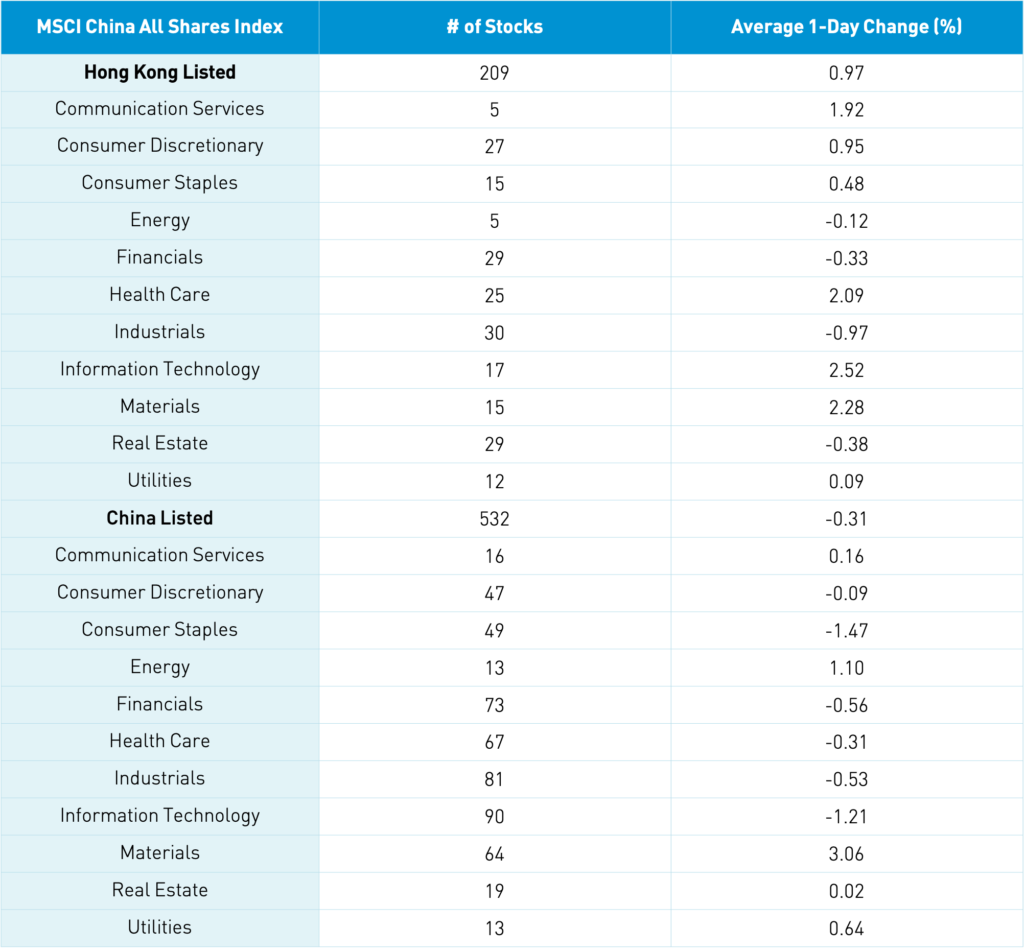

The Hang Seng Index and Hang Seng TECH Index overcame a midmorning swoon to gain +0.7% and +1.47% as volume decreased 9% from yesterday, which is still 114% of the 1-year average. The 209 Chinese companies listed in Hong Kong within the MSCI China All Shares Index gained +0.97%, led by tech +2.52%, materials +2.28%, healthcare +2.09%, communication +1.92%, discretionary +0.95%, and staples +0.48%, while industrials fell -0.97%, real estate -0.38%, and financials -0.33%. Hong Kong’s most heavily traded by value were Tencent, which rose +1.99%, Meituan, which rose +4.33%, Alibaba Hong Kong, which fell -0.91%, Xiaomi, which rose +5.12%, Hong Kong Exchanges, which was flat, Ping An, which fell -0.56%, BYD, which fell -1.64%, COSCO Shipping, which fell -10.71%, Wuxi biologics, which rose +5.0%, and Geely Auto, which fell -2.07%. Southbound Stock Connect volume was elevated.

A-Share Update

Shanghai, Shenzhen, and STAR Board mitigated early morning sell-offs closing -0.04%, James Bond +0.07, and -1.68% respectively as volume declined -5.84% from yesterday, though still 121% of the 1-year average. The 532 Mainland stocks within the MSCI China All Shares declined -0.28% with materials +3.08%, energy +1.13%, and utilities +0.66% while staples -1.45%, tech -1.18%, and financials -0.53%. The Mainland’s most heavily traded stocks by value were COSCO Shipping, which fell -7.19%, Longi Green Energy, which rose +1.36%, China Three Gorges Renewables, which rose +2.96%, Tianqi Lithium, which rose +8.42%, BYD, which fell -1.25%, CATL, which fell -2.37%, China Northern Rare Earth, which rose +10%, Ganfeng Lithium, which rose +5.64%, GEM, which rose +10.01%, and broker East Money, which rose +0.93%. Northbound Stock Connect volumes were elevated as foreign investors sold -$32.6mm of Mainland stocks today.