Economic Data Spurs Rally as Foreign Investors Buy in Size

2 Min. Read Time

Upcoming Webinar:

Join us on Tuesday, July 27th at 11:00 am EDT for:

What’s Driving Electric Vehicles? Dissecting the Boom & New Investment Opportunities

Featuring experts from Bloomberg Indices, BI, BNEF and KraneShares

Click here to register.

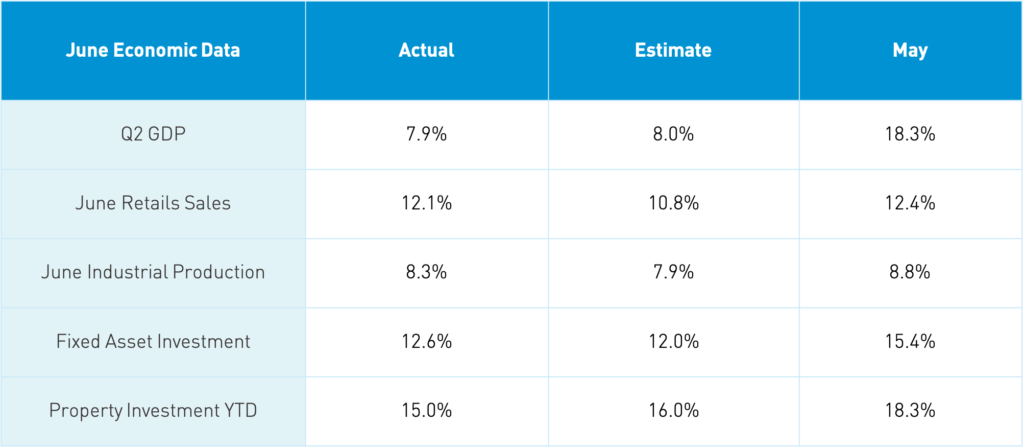

June Economic Data Release

Takeaway: The release broadly beat expectations as Q2 and June 2021 comparisons to last year when China was first coming out of quarantine is a low bar. We should expect that year-over-year comparisons will become more difficult as the low bar moves higher. Industrial Production has several interesting nuggets, for example 273k EVs were produced in June versus May’s 237k while total car production eased from May’s 780k to 743k. Mobile phone production increased from 132.35mm in May to June’s 143.22mm. Production of coal declined 5% year-over-year while natural gas increased 13.1%. Pharmaceutical saw the largest industry percentage gain at 32.5%. Within retail sales, online retail sales were up 23.2% year-over-year in June. But I thought internet companies were hurt by regulation? The data doesn’t agree. Today’s release was a positive catalyst for the market.

Key News

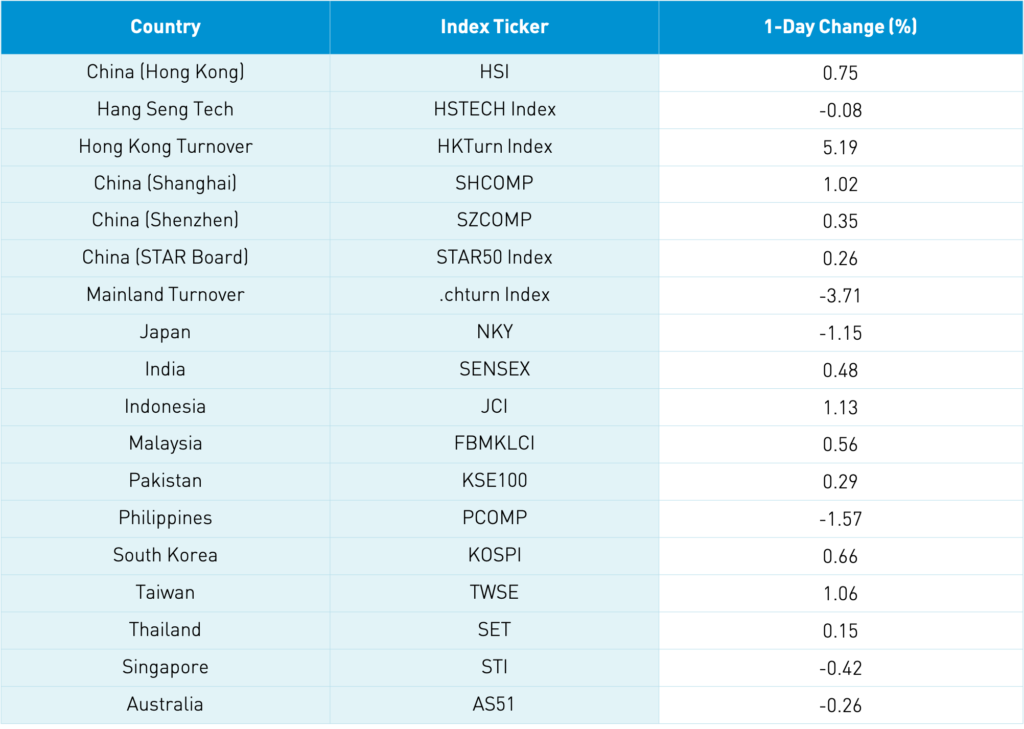

Asian equities were largely higher though Japan underperformed. As mentioned, China’s economic June/Q2 data largely beat expectations. Chinese internet stocks were up in Hong Kong led by Alibaba Hong Kong, which gained +2.03%, and Tencent, which rose +1.53%. This can be attributed to yesterday’s WSJ article on the two behemoths cooperating, which shows how the companies are adhering to the new regulations. While this was “news”, we’ve mentioned in the past how the companies are now opening up to one another. It just shows how sentiment is a bigger driver than fundamentals.

Online retail sales in June increased +23.2% year-over-year, showing that Chinese consumers continue to use the offerings of internet companies. Alibaba is apt to see inflow based on a market cap adjustment for Hang Seng Indexes tomorrow.

The EV ecosystem less auto manufacturers had a strong day with metal/rare earth stocks outperforming. China’s expected announcement tomorrow on launching its carbon emissions trading lifted cleantech plays. Financials had a strong day on optimism for the first half of 2021 results. Foreign investors bought a healthy $1.919B of Mainland stocks today, which raises YTD inflow to $36.754B.

According to South China Morning Post, there's been some chatter about a Biden-Xi meeting at the G-20 summit with Deputy Secretary of State Wendy Sherman headed towards China next week.

H-Share Update

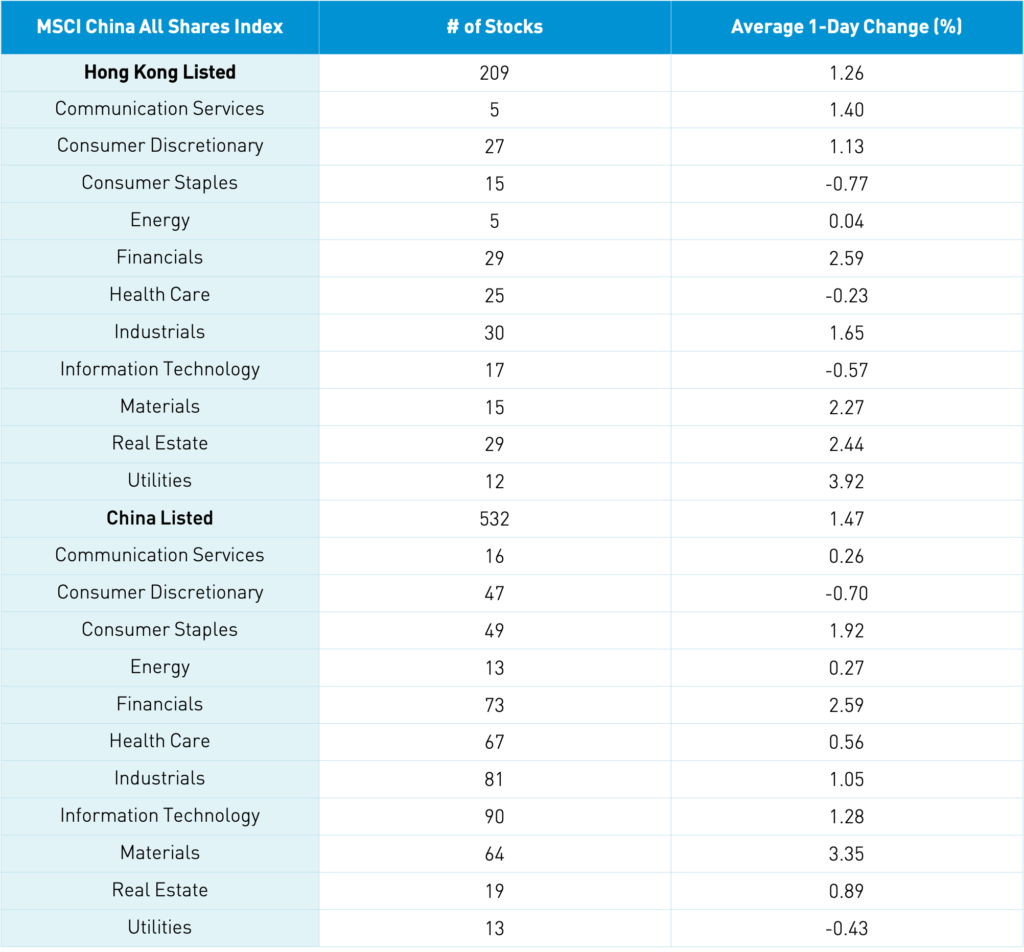

The Hang Seng Index and Hang Seng TECH Index diverged gaining +0.75% and falling -0.08% respectively as volume increased +5% from yesterday, which is 92% of the 1-year average. The 209 Chinese companies listed in Hong Kong within the MSCI China All Shares Index gained +1.27%, led by utilities +3.92%, financials +2.59%, real estate +2.44%, materials +2.27%, industrials +1.65%, communication +1.41%, and discretionary +1.14%, while staples -0.76%, tech -0.57%, and healthcare -0.23%. Hong Kong’s most heavily traded by value were Tencent, which rose +1.53%, Alibaba HK, which rose +2.03% Meituan, which rose +0.14%, Ping An, which rose +3.69%, Medlive Technology’s IPO, which rose +13.97%, BYD, which fell -3.26%, HK Exchanges, which fell -0.39%, Xiaomi, which fell -0.74%, COSCO Shipping, which fell -1.16%, and Wuxi Biologics, which fell -1.5%. Southbound Stock Connect volumes were light as Mainland investors bought $2.832mm of Hong Kong stocks as Southbound trading accounted for 11.2% of Hong Kong turnover.

A-Share Update

Shanghai, Shenzhen, and STAR Board gained +1.02%, +0.35%, and +0.26% respectively as volume declined -3.7% from yesterday, which is still 128% of the 1-year average. The 532 Mainland stocks within the MSCI China All Shares Index gained +1.45%, led by materials +3.32%, financials +2.55%, staples +1.88%, tech +1.24%, industrials +1.01%, and real estate +0.84%, while discretionary fell -0.74% and utilities -0.47%. The Mainland’s most heavily traded by volume were BYD, which fell -3.62%, Longi Green Energy, which rose +6.43%, China Northern Rare Earth, which rose +10%, Tianqi Lithium, which rose +9.51%, COSCO Shipping, which fell -6.3%, broker East Money, which rose +2.92%, Kweichow Moutai, which rose +1.83%, Ganfeng Lithium, which rose +5.05%, CATL, which rose +3.02%, and BOE Tech, which fell -3.36%. Northbound Stock Connect volumes were elevated as foreign investors bought $1.919B of Mainland stocks as Northbound Stock Connect trading accounted for 5.6% of Mainland turnover.