China Carbon Trading Kicks Off, Week in Review

4 Min. Read Time

Upcoming Webinars:

Join us on Wednesday, July 21st at 8:00 am EDT for:

Q2 China Internet, STAR Market, & ESG Update

Click here to register.

Week in Review

- Growth stocks and Asian markets in general rose Monday as the People’s Bank of China (PBOC) reduced banks’ reserve requirement ratio (RRR). The central bank’s decision reflects China’s having some left over dry powder from the pandemic. This differs from the US and Europe, where policy rates likely remain close to their lower bounds.

- China released June import/export data Tuesday. Import and export growth remain strong, though import growth has clawed back from its whopping May reading of +51% year-over-year as commodity prices have stabilized.

- Regulators approved Tencent’s proposed acquisition of search engine Sogou Tuesday. Markets rallied on the news as positive regulatory news is a rare sight in today’s market.

- The US CPI reading of above 5% in June sent Asian stocks lower on Wednesday. However, some foreign investors used the downdraft to buy A shares on Thursday.

Friday’s Key News

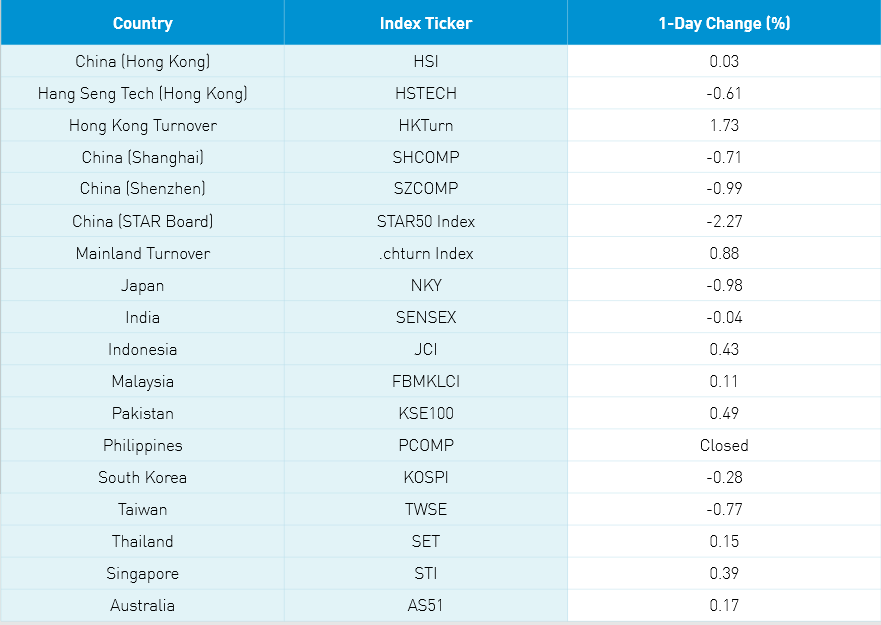

Northern Asia was off as Hong Kong managed a small gain while Southern Asia was largely higher. Despite today’s downdraft, the Hang Seng, Shanghai Composite, and Shenzhen Component Indexes were all up this week. Hong Kong rallied on news that IPO listings in the financial center will not require cybersecurity reviews though US listings will likely require such reviews in most cases. Hong Kong Exchanges gained +3.76% overnight.

Trading in China’s carbon emission allowance program started today. The price of emitting one ton of carbon jumped to the daily limit, gaining +10% to reach RMB 52.78 with 4.1 million tons of contract trading according to Climate Finance Partners. According to Bloomberg, 2,200 power companies need to buy contracts to offset the pollution they generate. It is widely expected that more industries will participate in the future, though the market is currently limited to power companies.

Hong Kong-listed China internet companies were largely higher though Alibaba HK and Tencent were off -0.57% and -0.18%, respectively. Overnight, it was reported that Didi will be investigated by multiple regulatory bodies. Didi is in a unique position, having pushed its US IPO through without getting an implicit green light from Mainland regulatory bodies. We still have not seen an instance where regulation has hurt the financials of a company as evidenced in Q4 2020 and Q1 2021 financial results. However, after school tutoring companies are likely to see a material impact on their financials due to new regulations as the number of hours kids can study will be curtailed. We do not yet know the rules. Nonetheless, the market has hammered the names in the space, which are down, on average, -70% year-to-date in some cases. We continue to observe Mainland investors buying a mainland listed ETF that holds US and Hong Kong-listed Chinese internet stocks. Why are they buying? Because they are using the services of these companies every day!

Mainland markets were off, though there did not appear to be any single catalyst for their underperformance.

There was news that China will not meet with Deputy Secretary of State Wendy Sherman, according to the Financial Times, while she is in Asia.

Growth names were off today as healthcare, consumer discretionary, and consumer staples were all off -2%. Foreign investors sold -$640 million worth of Mainland stocks today though they were net buyers of Shenzhen-listed stocks and net sellers of Shanghai-listed stocks. CNY was off a touch versus the US dollar while bonds rallied.

Over the last decade, the number of mutual funds in China has grown from 652 with RMB 2.386 trillion in assets to 8,216 with 22.413 trillion in assets (Q3 2010 to July 2021). As of July 15, equity funds represent 8.87% of the total (RMB 1.988 trillion), hybrid (balanced) funds 26.07% (RMB 5.843 trillion), bonds funds 23.16% (RMB 5.191B), and money market mutual funds 40.62% (RMB 9.104). Interesting right? Why the mention? Because bonds have been rallying in China. When do Chinese investors reallocate out of bonds and money market funds into stocks? The yield on the Chinese 1-year government bond yielded over 3% in November 2020 now yields 2.9%. Lots of dry powder!

After yesterday’s strong economic data release, this was the Financial Times’ headline: “China warns of economic uncertainty despite moderate recovery in Q2”. Retail sales, industrial production, fixed-asset investment (FAI), and property investment all beat expectations. Q2 GDP was expected at 8% but came in at 7.9%. Their headline seems a tad exaggerated.

H-Share Update

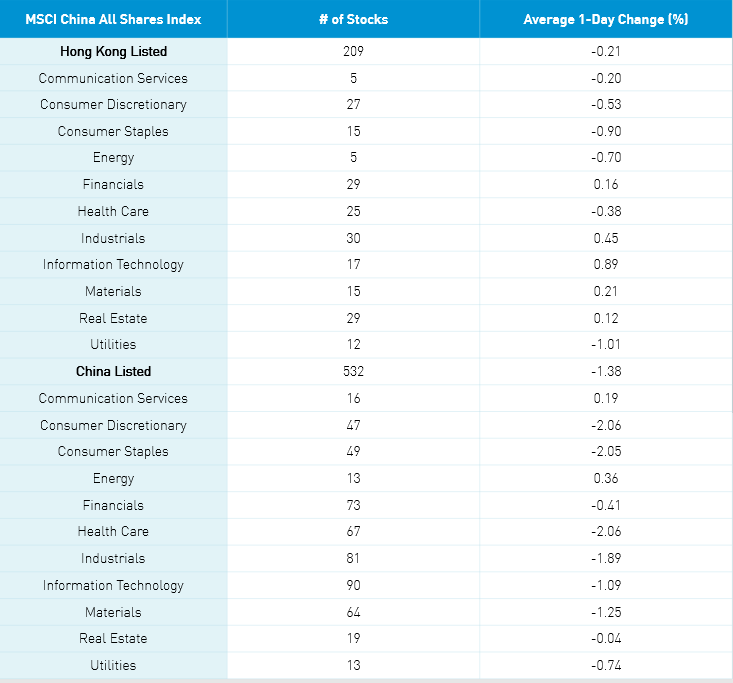

The Hang Seng Index and Hang Seng TECH Indexes diverged +0.03% and -0.61% as volume increased +1.7% from yesterday, which is 94% of the 1-year average. The 209 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index eased -0.21% with tech +0.89%, industrials +0.45%, materials +0.21% while utilities -1.01%, staples -0.9%, energy -0.7% and discretionary -0.53%. Hong Kong’s most heavily traded stocks by value were Alibaba HK, which fell -0.57%, HK Exchanges, which gained +3.76%, Tencent, which fell -0.18%, Xiaomi, which gained +4.82%, Meituan, which gained +0.14%, Ping An Insurance, which gained +0.48%, BYD, which fell -0.65%, Wuxi Biologics, which gained +1.6%, Dongyu Group, which fell -2.75%, and AIA, which gained +0.1%. Southbound Stock Connect volumes were moderate as Mainland investors bought $74 million worth of Hong Kong stocks as Southbound trading accounted for 11.6% of Hong Kong turnover.

A-Share Update

Shanghai, Shenzhen, and the STAR Board sold off into the close to finish the session down by -0.71%, -0.99%, and -2.27%, respectively, on volumes that were +0.88% higher than yesterday, which is 130% of the 1-year average. The 532 Mainland stocks within the MSCI China All Shares Index lost -1.4% with energy +0.35% and communication +0.18 while discretionary -2.07%, healthcare -2.07%, staples -2.06%, industrials -1.9%, materials -1.27%, tech -1.1% and utilities -0.75%. The mainland’s most heavily traded stocks by value were BYD, which fell -5.7%, China Northern Rare Earth, which fell -4.59%, CATL, which fell -6.51%, Longi Green Energy, which fell -4.43%, Hoperun Software, which fell -3.46%, broker East Money, which fell -1.78%, Tianqi Lithium, which fell -3.42%, BOE Tech, which gained +2.53%, Shenghe Resources, which gained +6.02%, and Kweichow Moutai, which fell -2.11%. Northbound Stock Connect volumes were moderate/high as foreign investors sold -$640 million worth of Mainland stocks as Northbound Connect trading accounted for 5.7% of Mainland turnover. CNY was off slightly versus the US dollar, bonds rallied, and copper rallied.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.47 versus 6.46 yesterday

- CNY/EUR 7.64 versus 7.63 yesterday

- Yield on 1-Day Government Bond 1.72% versus 1.70% yesterday

- Yield on 10-Year Government Bond 2.94% versus 2.96% yesterday

- Yield on 10-Year China Development Bank Bond 3.34% versus 3.35% yesterday

- Copper Price +0.92%