Regulation Endgame: Alleviate the Burdens on Chinese Households

3 Min. Read Time

Key News

Asian equities were largely lower though Japan was an outlier to the upside. A typhoon hit the Shanghai area overnight though it felt more like a financial typhoon. Hong Kong and China were off as investors digested the after-school tutoring ban and its impact on for-profit companies, which was leaked after the local market’s close Friday. The news weighed on the broader Hong Kong market and spilled over onto the Mainland market for the first time. Volumes in Hong Kong were exceedingly high in what felt like a panic plunge.

Hong Kong-listed Meituan was off -13.67% upon news that wages for delivery staff will be examined. Meituan employs 69,000 employees, many of whom include delivery drivers who have limited education and employment opportunities. The wage they earn from Meituan is likely far better than what they could earn elsewhere. Real estate and healthcare were both weak as investors are worried that they might see regulatory action as well.

Policy appears to be alleviating the financial burdens on Chinese households to raise the birthrate. After-school tutoring (AST) may have eaten up to 25% of urban household income in many cases, according to a Mainland media source. Vast amounts of capital were directed to the AST space, which could have been allocated to the segments of the economy that China needs. High apartment prices have also been an issue for many years. Policy has looked to reducing healthcare costs, through the bulk buying of drugs, which has been in place for several years now.

However, the market’s shoot-first mentality is perplexing. If kids will not have to study as much, wouldn’t that open up more time to play video games? Shouldn’t Tencent and NetEase benefit from AST regulation? Yes. We had news that Tencent Music Entertainment’s exclusive music deals could be nullified, though that should help NetEase. There was a small indication that investors are starting to connect the dots as semiconductors stocks rallied on the Mainland. Why? All that private equity money that would have gone to AST might be redirected to an industry the economy needs.

The STAR Board was off by a touch. The other important issue is to recognize that many companies have adopted and adhered to the regulation. If policy can redirect money that would have gone into real estate, it would go a long way to building technology and economic sectors China needs as opposed to a concrete block.

Q2 financial results start next week with Alibaba. The most important part of the release will be management addressing analysts’ questions on regulation. I suspect they will reiterate that they paid the fine and have moved on.

Another factor was the report that US Deputy Secretary of State Wendy Sherman’s meeting in China went all right. Remember that China was not originally on her schedule, so I’ll take the fact they met as a positive.

H-Share Update

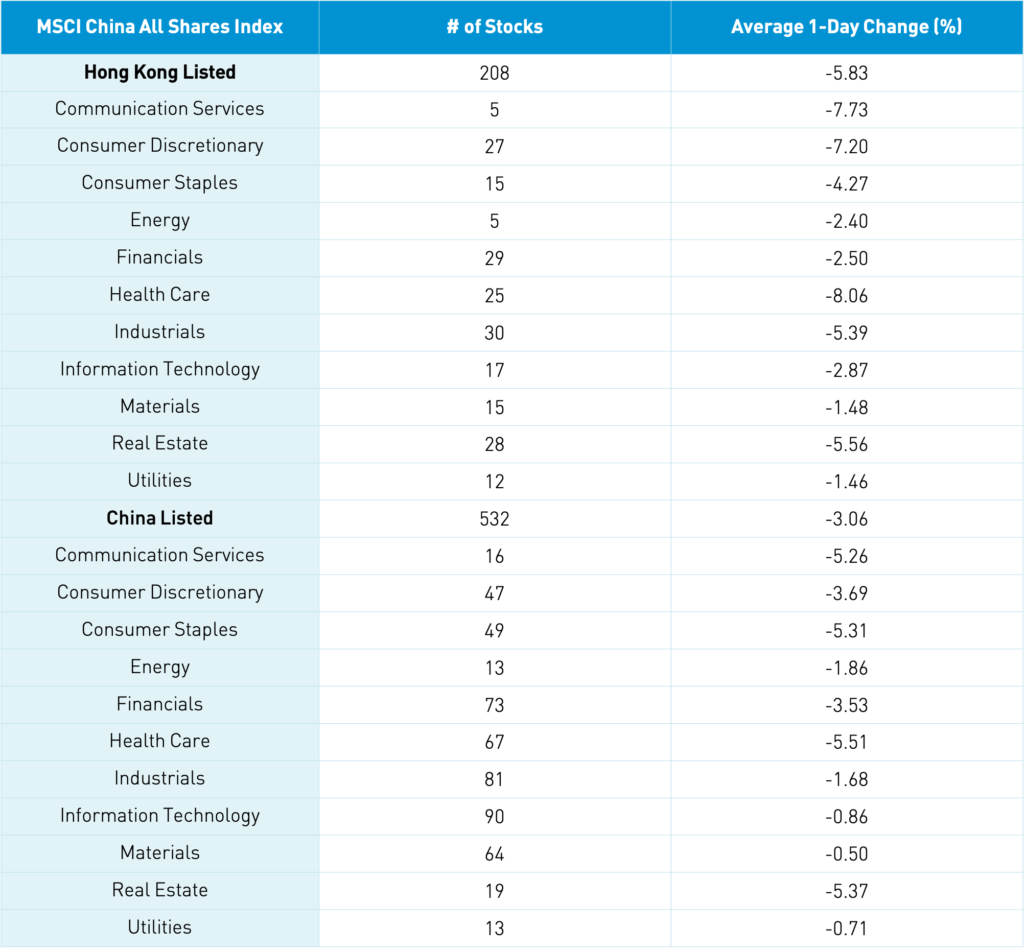

The Hang Seng Index opened lower and kept sliding to close -4.13% while the Hang Seng TECH Index was off -6.57% as volume surged +92% from Friday, which is 164% of the 1-year average. The 208 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index were off -5.81% led by healthcare -8.04%, communication -7.71%, discretionary -7.19%, real estate -5.54%, industrials -5.37%, staples -4.26%, tech -2.85%, financials -2.48%, energy -2.38%, materials-1.46% and utilities -1.44%. Hong Kong’s most heavily traded stocks by volume were Tencent, which fell -7.72%, Meituan, which fell -13.76%, Alibaba HK, which fell -6.38%, HK Exchanges, which fell -4.03%, Xiaomi, which fell -1.9%, SMIC, which gained +10.27%, Wuxi Biologics, which fell -9.79%, NetEase, which fell -13.29%, Ping An Insurance, which fell -5.05%, and BYD, which fell -4.14%. Southbound Stock Connect volumes moderate/light.

A-Share Update

Shanghai, Shenzhen, and the STAR Board were down -2.34%, -2.28%, and -0.42%, respectively, as volume increased +3.03%, which is 157% of the 1-year average. The 532 Mainland stocks within the MSCI China All Shares Index were off -3.07% led lower by healthcare, which fell -5.53%, real estate, which fell -5.39%, staples, which fell -5.33%, communication, which fell -5.28%, discretionary, which fell -3.71%, financials, which fell -3.55%, energy -1.88%, industrials -1.7%, tech -0.88%, utilities -0.73% and materials -0.52%. The mainland’s most heavily traded stocks by value were Kweichow Moutai, which fell -5.05%, Longi Green Energy, which fell -4.16%, Wuliangye Yibin, which fell -7.99%, East Money, which fell -3.81%, Tianqi Lithium, which gained +9.57%, BYD, which fell -3.92%, China Northern Rare Earth, which gained +4.06%, Hangzhou Silan Microelectronic, which gained +7.25%, and Sanan Optoelectronic, which gained +0.86%. Northbound Stock Connect volumes were high as foreign investors sold -$1.974 billion worth of Mainland stocks

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.48 versus 6.48 Friday

- CNY/EUR 7.65 versus 7.63 Friday

- Yield on 1-Day Government Bond 1.59% versus 1.63% Friday

- Yield on 10-Year Government Bond 2.87% versus 2.91% Friday

- Yield on 10-Year China Development Bank Bond 3.27% versus 3.30% Friday

- Copper Price +1.38% overnight