CSRC Extends an Olive Branch as Hong Kong Internet Rebounds

3 Min. Read Time

Webinar Tomorrow:

Join us tomorrow at 11:00 am EDT for:

China Market Volatility Update and Q&A With KraneShares

Click here to register.

Key News

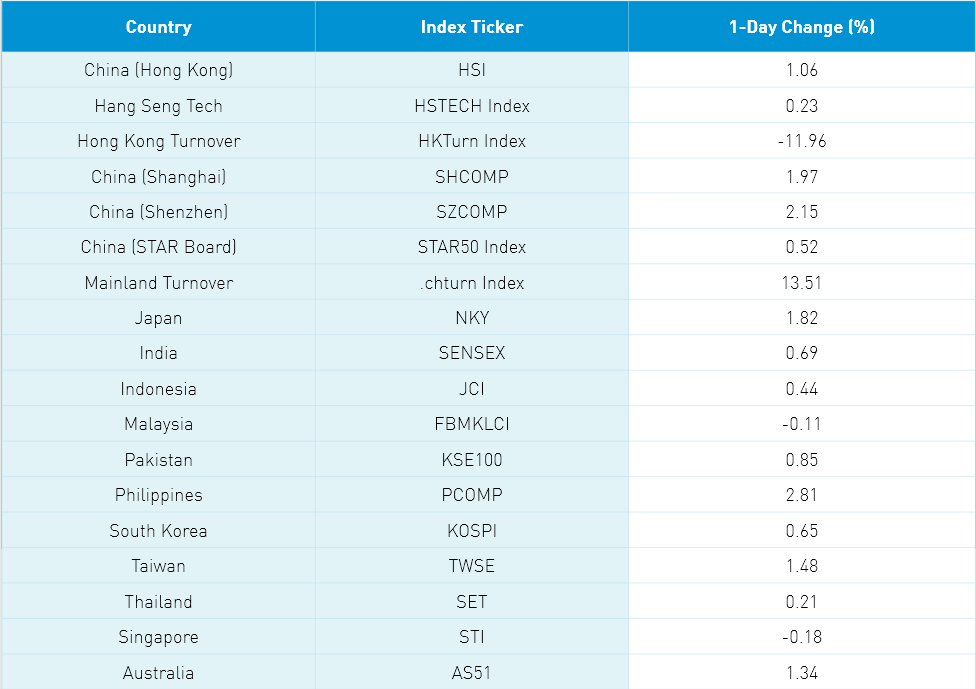

Asian equities were a screen of green as Japan, Hong Kong, China, Taiwan, and Australian stock markets outperformed.

Over the weekend, China’s SEC/financial regulator, the China Securities Regulatory Commission (CSRC), held a press conference with potentially strong implications. First, they stated, “The CSRC has always been open to companies to list their securities on international or domestic markets…”. So, rumors of US listings’ demise might be exaggerated. Second, they stated “companies shall abide by applicable laws, regulations, and regulatory requirements in both their listing jurisdiction and operating jurisdiction.” To abide by US rules means US-listed Chinese companies should allow audit reviews by the PCAOB. They also stated, “It is our belief that Chinese and U.S. regulators shall continue to enhance communication with the principle of mutual respect and cooperation, and properly address the issues related to the supervision of China-based companies listed in the U.S….”. Communication is key to solving the audit review issue. Hopefully, that is taking place.

Ray Dalio of the prestigious hedge fund, Bridgewater, had a very good piece on the topic that I recommend. Ultimately the regulatory pendulum swung too far in what felt like an ad hoc manner. Clearly, there needs to be better communication and an end game provided.

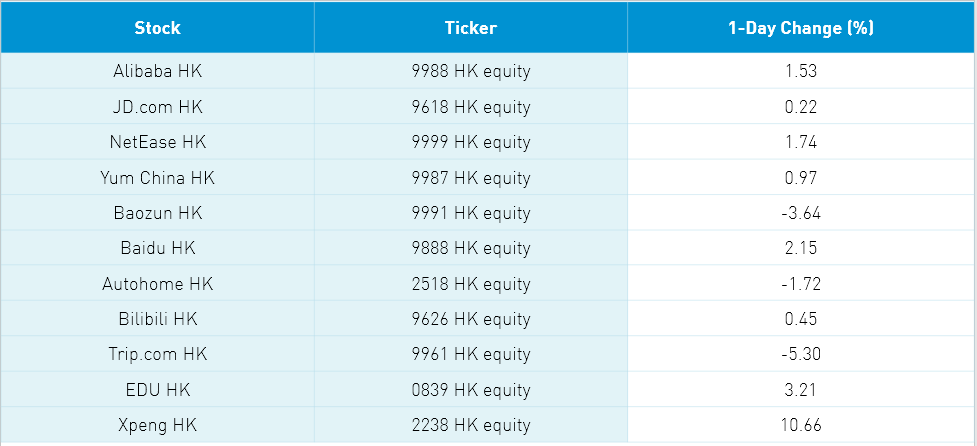

Hong Kong listed internet companies with listings in the US rallied in Hong Kong today, though Tencent (700 HK) was off -0.84% with heavy selling from Mainland investors via Southbound Stock Connect.

July’s Caixin Manufacturing PMI came in a touch light at 50.2 versus expectations of 51 and June’s 51.3 driven by slowing export orders, new orders, output, and higher input prices. Massive rainfall and flooding were likely factors as well. The market’s positive reaction is likely driven by the belief that supporting policies such as the July bank reserve requirement ratio cut will continue into the second half of 2021. Last Friday’s policy meeting appears to support this thesis.

The EV ecosystem was a strong performer today in Hong Kong and the Mainland as July auto sales data trickles out. I’ve not seen the data as of yet, but chatter appears to be strong. Liquor stocks rebounded in the Mainland following last week’s swoon while Mainland semiconductors were off in profit-taking.

Remember Alibaba reports earnings tomorrow after the Hong Kong close. I suspect topline growth will be strong though capital expenditures will crimp on margins and thus net income and earnings per share growth. Investing in one’s business is a strong indication that it isn’t’ going away. The Q&A with analysts will be very interesting!

Education stocks TAL and EDU announced they won’t release their earnings reports this week as they try to ascertain policies in the space.

H-Share Update

The Hang Seng Index initially fell at the open morning -0.84% but rallied back to close +1.06% while the Hang Seng TECH +0.23%. Volumes were down -11.98% from Friday which is is just above the 1-year average. The 208 Chinese companies listed in Hong Kong within the MSCI China All Shares gained +1.18% led by materials +4.82%, real estate +3.54%, staples +3.05%, utilities +2.16%, industrials +1.89%, discretionary +1.46%, tech +1.42%, energy +1.34%, financials +1.11% and healthcare +0.91% while communication was off -0.77%. Hong Kong’s most heavily traded were Tencent -0.84%, BYD +8.03%, Meituan +0.47%, SMIC -0.37%, Alibaba HK +1.53%, Hong Kong Exchanges +4.33%, Geely Auto +3.08%, Ping An Insurance +-.15%, Xiaomi +1.58% and Anta Sport 0.0%. Southbound Stock Connect volumes were moderate as Mainland investors sold $111mm of Hong Kong stocks as Southbound trading accounted for 15.8% of Hong Kong turnover.

A-Share Update

Shanghai, Shenzhen, and STAR Board also opened lower but rallied back closing +1.97%, +2.15% and +0.52% on volume +13.51% from Friday which is nearly 3X the 1-year average. The 522 Mainland stocks with in the MSCI China All Shares gained +2.29% led by staples +4.72%, discretionary +3.37%, industrials +2.69%, materials +2.46%, financials +2.17%, communication +1.56%, real estate +1.45%, healthcare +1.22%, and tech +0.61% while energy -0.79%. The Mainland’s most heavily traded by value were BYD +10%, liquor company Kweichow Moutai +4.53%, China Northern Rare Earth +2.31%, broker East Money +6.38%, Ganfeng Lithium -3.21%, liquor company Wuliangye Yibin +6.21%, CATL +0.29%, SMIC +4.13% and Sungrow Power -4.29%. Northbound Stock Connect volumes were elevated as foreign investors bought $802mm of Mainland stocks today as Northbound trading accounted for 6.7% of Mainland turnover.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.46 versus 6.46 Friday

- CNY/EUR 7.68 versus 7.69 Friday

- Yield on 10-Year Government Bond 2.82% versus 2.84% Friday

- Yield on 10-Year China Development Bank Bond 3.20% versus 3.24% Friday

- Copper Price -0.89% overnight