Alibaba Earnings Review: “We are confident of our long-term growth prospects”

4 Min. Read Time

Webinar Today:

Join us today at 11:00 am EDT for:

China Market Volatility Update and Q&A With KraneShares

Click here to register.

Alibaba reported quarterly results this morning. While headlines might scream about a “revenues miss,” the company beat analyst expectations otherwise. Alibaba increased its stock buyback from $10B to $15B as the company is “confident of our long-term growth prospects” having bought $3.7B of the US stock since April 1st, 2021. We knew Alibaba is investing in growing its business, which would curtail margins as capital expenditures/expenses would increase. However, management did a great job making sure it didn’t hurt net income nor EPS.

In addition to the stock buyback, the company is investing in itself to drive future growth. This is a great sign, as sentiment has weighed on the China internet space dramatically despite the strong fundamentals. If the company is investing in itself, shouldn’t we as well? In another example of this, headcount increased to 254,702 from last quarter’s 251,462.

The Q&A session of the earnings call was all about regulation. Alibaba consistently responded that they are adhering to the regulation. Chairman and CEO, Daniel Zhang, stated that Alibaba will continue to adhere to regulations with “strict and full compliance”.

- Revenue increased +35% to RMB 205.74B ($31.865B) versus analyst estimates of RMB 209.38B and last year’s quarterly result of RMB 153.751B

- Global users increased +45mm quarter over quarter to 1.18B with China users increasing +21mm quarter over quarter to 912mm

- Revenue Breakdown highlight: China commerce retail, 66% of total revenue,+34% to RMB 135.806B versus last year’s quarterly result of 101.321B

- Total commerce, 87% of revenue, grew 35% to RMB 180.241B from last year’s RMB 133.318

- Cloud computing, 8% of revenue, +29% to RMB 16.051B from last year’s quarterly result of RMB12.437B

- Adjusted EBITDA declined -5% to $7.532B/RMB 48.628B versus analyst expectations of RMB 48.628B and last year’s quarterly result of RMB 51.039B

- Adjusted EBITDA margin was 24% versus last year’s quarterly result of 33%

- Adjusted Net Income increased 10% to $6.728/RMB 43.441B versus analyst expectations of RMB 38.824B and last year’s quarterly result of RMB 39.373B

- Adjusted EPS was $2.57/RMB 16.60 versus analyst expectations of RMB 14.45

Key News

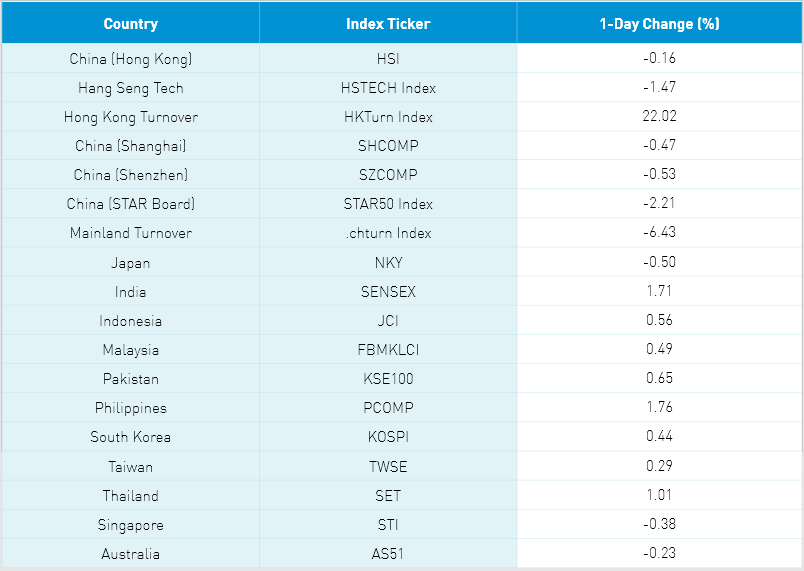

Asian equities were mixed as Southeast Asia outperformed while North Asia was largely off.

An article criticizing gaming as “spiritual opium” -- calling it “electronic drugs” led to a decline in online gaming companies Tencent and NetEase. The online article was removed though it weighed on online gaming stocks. Tencent (700 HK) came off intra-day lows of -10.82% closing at -6.11% while NetEase HK (9999 HK) closed down -7.77% but off the intra-day low of -15.68%. It was reported that Tencent has said it will restrict the number of hours kids under the age of twelve can play games, limiting them from 1 ½ hours to an hour. Analysts have said that the revenue generated from kids under the age of twelve is de minimis.

As we noted last week, Hong Kong has a big structured product market, which locals call warrants. Structured products are created by banks to give an investor exposure to stock but with principal protection by using the stock’s options. Many of these structured products have it written that once a price level is hit, the structured product is liquidated which puts further pressure on the underlying stock as the bank takes off its hedge.

The move from Tencent and NetEase was likely exacerbated by structured products being liquidated. Regardless, the new regulation headline is poor timing. It is important to note that the Mainland market was off today. When the Mainland market fell due to regulation concerns last week, there was an increasing number of Mainland financial media articles noting the health of the economy and stock market. Hopefully, today’s market action is recognized. More importantly, regulation has the potential to hurt the real economy as foreign companies hesitate to invest in factories and their China businesses.

Mainland markets were off though healthcare outperformed on Delta variant fears. Semis and autos were weak on news there will be an investigation into auto chip shortages and the rising price of autos. Semis, being off on the news, dragged the STAR Board lower in addition to the EV ecosystem. Advancers beat decliners in Shanghai and Shenzhen today, as the broader market held up.

H-Share Update

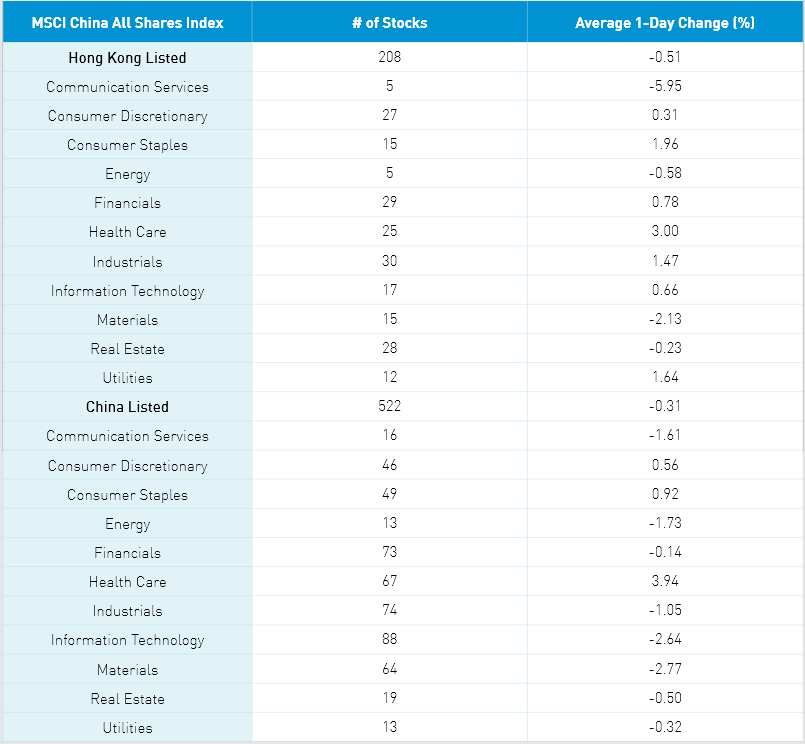

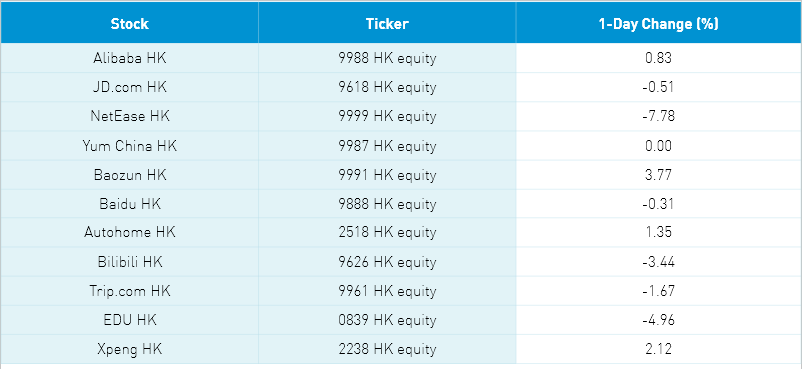

The Hang Seng bounced around the room, coming off morning lows to close -0.16% at 26,194 as volume increased +21.95% from yesterday which is 122% of the 1-year average. The 208 Chinese companies listed in Hong Kong within the MSCI China All Shares declined -0.51% with healthcare +3%, staples +1.96%, utilities +1.64%, industrials +1.47%, and financials +0.78% while communication -5.95%, materials -2.14%, energy -0.58% and energy -0.23%. Hong Kong’s most heavily traded by value was Tencent -6.11%, Meituan -2.04%, Alibaba HK +0.83%, BYD +0.31%, Geely Auto +0.37%, NetEase -7.77%, SMIC -5.91%, Xinyi Solar +8.35%, Ping An +1.32% and Hong Kong Exchanges +0.1%. Southbound Stock Connect volumes were very high as mainland investors sold -$635mm of Hong Kong stocks as Southbound trading accounted for 15.9% of Hong Kong turnover.

A-Share Update

Shanghai, Shenzhen & STAR Board opened lower, rebounded and sold off at the close -0.47%, -0.52% & -2.21% on volume off -6.43% from yesterday which is 155% of the 1-year average. The 522 mainland stocks within the MSCI China All Shares were off -0.3% with healthcare +3.95%, staples +0.92% and discretionary +0.57% while materials -2.76%, tech -2.63%, energy -1.72%, communication -1.61%, industrials -1.05% and real estate -0.49%. The mainland’s most heavily traded stocks by value were Sany Heavy Industry +5.35%, BYD -3.81%, China Northern Rare Earth -8.07%, Tianqi Lithium -6.97%, broker East Money +0.61%, Sungrow Power Supply -10.35%, Kweichow Moutai -0.32%, COSCOShipping +6.82%, Sanan Optoelectronic -0.39% and Ganfeng Lithium -7.01%. Northbound Stock Connect volumes were high as foreign investors bought $278mm of mainland stocks as Northbound trading accounted for 5.3% of mainland turnover.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.46 versus 6.46 yesterday

- CNY/EUR 7.68 versus 7.68 yesterday

- Yield on 10-Year Government Bond 2.83% versus 2.82% yesterday

- Yield on 10-Year China Development Bank Bond 3.21% versus 3.20% yesterday

- Copper Price -0.91% overnight