One Step Forward and One Step Back

2 Min. Read Time

Key News

Asian equities were mixed following the US equity slide and increasing fears of the Delta variant contagion with Australia headed into a lockdown.

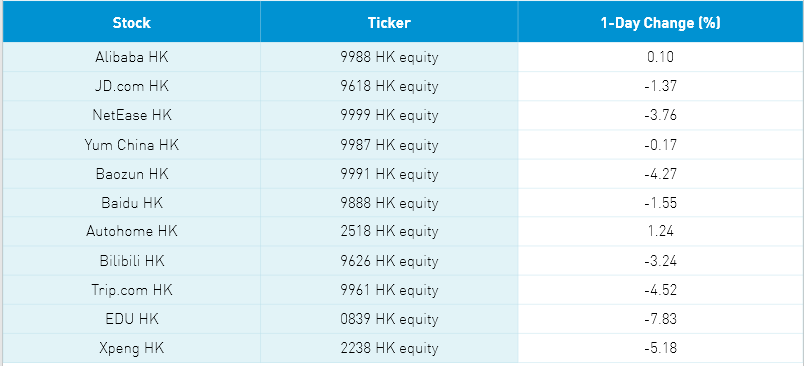

We took one step forward as Tencent’s social media platform, WeChat, was allowed to take on new users following a user data security review. We then took a step back as a Mainland media source reported that online gaming companies shouldn’t receive discounted tax rates, sending Tencent and NetEase lower. Mainland investors were net sellers of Tencent but not in significant size via Southbound Stock Connect, following yesterday’s first net buying day in two weeks.

A Mainland media source noted “China’s stock market has experienced some volatility recently, partly due to a certain degree of worry in the market with the recent regulatory policies for the platform economy and tutoring industry.” The article noted this reaction is “misinterpreting the regulatory moves…” and instead stressed the long-term development goals as well as the importance of protecting user data and privacy.

We also had a Mainland media article noting the problem of vaping among kids and the dangers of alcohol, which sent related stocks including liquor giant, Kweichow Moutai, down. Hopefully, the source of today’s market volatility is recognized.

Hong Kong was solidly off as even healthcare was down despite the delta fears. Elements of the EV ecosystem managed gains in the Mainland along with semiconductor stocks following strong results from SMIC. BYD was off despite reporting 50,492 EVs were sold in July, which is an increase of 170% over the same period last year.

H-Share Update

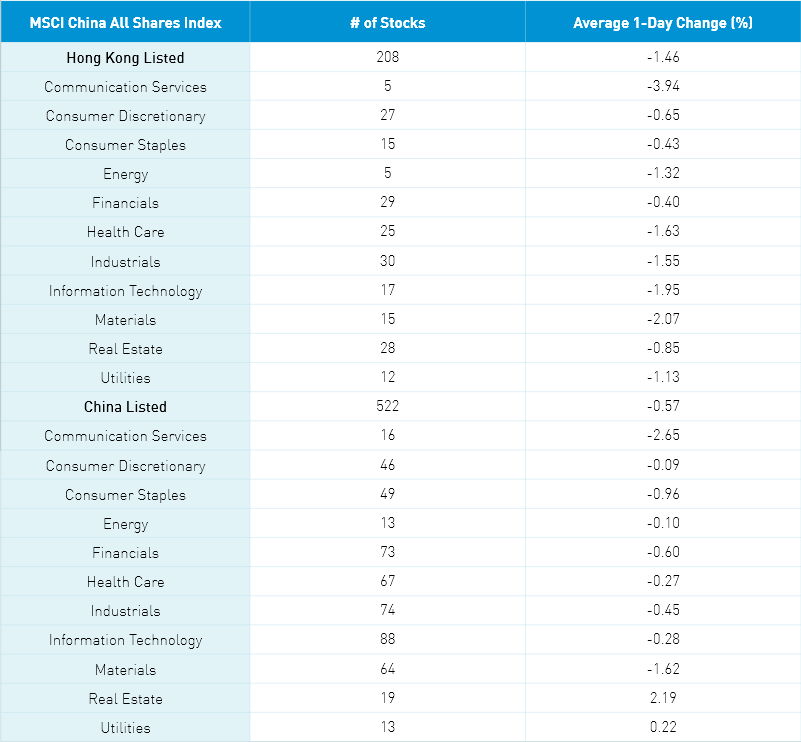

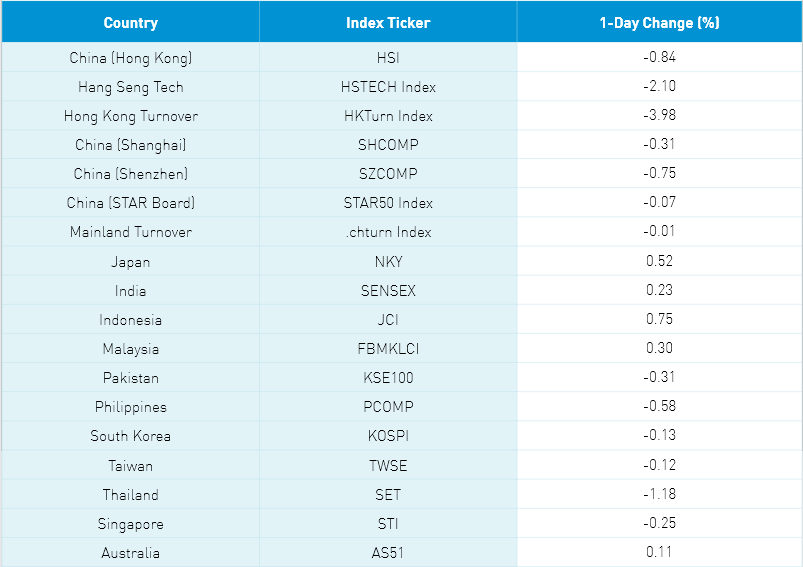

The Hang Seng opened higher but slid in the afternoon session closing -0.84% while the Hang Seng TECH down -2.1% as volumes slid -4.01% which is 97%. The 208 Chinese companies within the MSCI China All Shares were off -1.47% led lower communication -3.94%, materials -2.08%, tech -1.96%, healthcare -1.64%, industrials -1.56%, energy -1.33%, utilities -1.13% and real estate -0.86%. Hong Kong’s most heavily traded by value were Tencent -3.9%, SMIC +3.91%, Alibaba HK +0.1%, Kuaishou -15.3%, Meituan -1.12%, BYD -3.49%, Geely Auto -0.53%, Xiaomi -2.05%, NetEase -3.76%, and Hong Kong Exchanges +0.77%. Southbound Stock Connect volumes were elevated as Mainland investors sold -$148mm. Southbound trading accounted for 15% of Hong Kong turnover.

A-Share Update

Shanghai, Shenzhen and STAR Board had a choppy session opening lower, rallying into the green and then sold off closing -0.31%, 0.75% and James Bond’s -0.07%. volumes were off -0.01% which is 141% of the 1-year average. The 522 Mainland stocks within the MSCI China All Shares was off -0.57% with real estate and utilities gaining +2.19% and +0.22% while communication -2.65%, materials -1.62%, staples -0.96%, financials -0.6%, industrials -0.45%, tech -0.28%, healthcare -0.27%, energy -0.09% and discretionary -0.09%. China’s most heavily traded by value were China Northern Rare Earth -2.22%, Longi Green Energy +1.29%, BYD -2.8%, Tianqi Lithium +0.91%, Tongwei +1.87%, Kweichow Moutai -1.45%, Sany Heavy Industry -0.56%, Changchun High & New Technology -10%, CATL -2.11%, and SMIC +5.08%. Northbound Stock Connect volumes were moderate as foreign investors sold -$304mm of Mainland stocks with Northbound trading accounted for 5.5% of Mainland turnover. Bonds rallied while the renminbi was flat versus the US $ and copper was off.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.46 versus 6.46 yesterday

- CNY/EUR 7.66 versus 7.66 yesterday

- Yield on 10-Year Government Bond 2.80% versus 2.83% yesterday

- Yield on 10-Year China Development Bank Bond 3.19% versus 3.19% yesterday

- Copper Price -0.60% overnight