Flooding Rains on July Economic Data

2 Min. Read Time

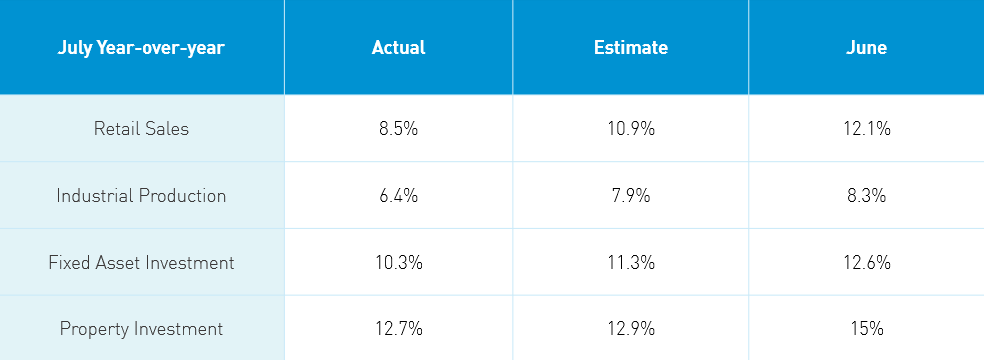

July Economic Release

Takeaway: July’s data release came in light despite lower expectations for month-over-month growth. We have often seen negative economic data lift equity markets as investors may anticipate policy support. However, that did not occur today, which I attribute to the summer slowdown. The release weighed on Hong Kong and the Mainland market’s sentiment, though we know that year-over-year comparisons will only look worse as we move farther afield from last year’s Q1 quarantine. Another factor was significant flooding in China last month, which undoubtedly weighed on economic output. Throw in some regional delta quarantines and today’s light read should not have been a surprise. Within retail sales, auto sales declined year-over-year -1.8% weighing on automakers and the electric vehicle ecosystem. Unemployment saw a slight uptick, which should also give policymakers pause and pave the way for further support.

Key News

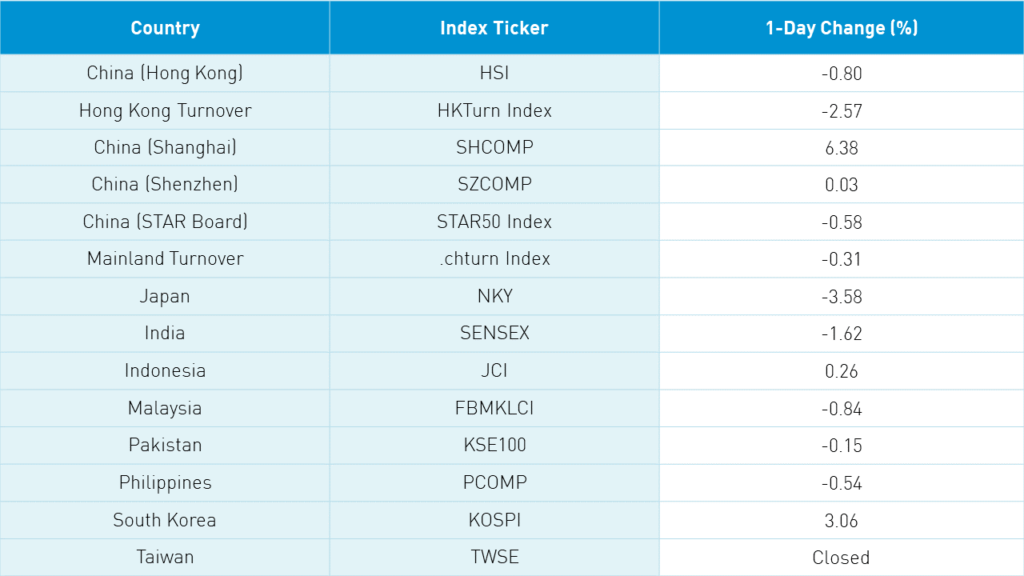

Asian equities were mostly lower except for the Philippines, which had a strong day. South Korea was on holiday today.

A single headline in Mainland media claiming that online games might be “distorting” history sent Hong Kong-listed internet stocks lower, which is indicative of the shoot-first mentality of investors and sentiment in the space. Frankly, I am not sure who uses a video game as a history lesson.

Mainland investors were net sellers of Tencent on the weakness today.

A Nio-made vehicle caught fire in an accident, killing its driver. The electric vehicles (EV) ecosystem was weak on the news including rare earths, metals, automakers, and EV automakers. On the positive side, Li Auto’s Hong Kong listing will be added to Hang Seng Indexes at the end of the month.

Value sectors held up today while growth names were weak in both Hong Kong and Mainland China.

We have the National People’s Congress beginning tomorrow.

Overnight, the People’s Bank of China (PBOC), China’s central bank, replaced medium-term notes due to expire with the full amount, which is a positive for market liquidity.

Foreign investors were active buyers of Mainland stocks overnight with nearly $1 billion of net buying.

H-Share Update

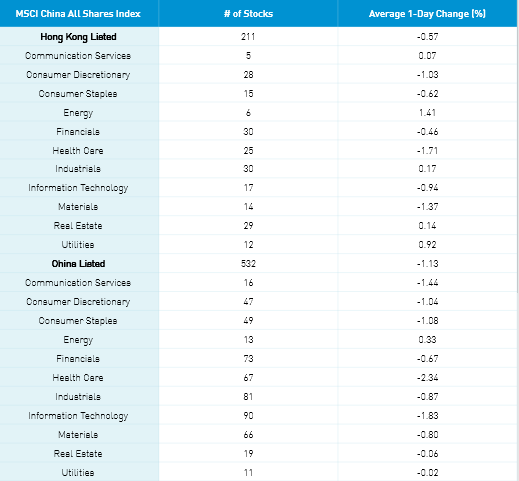

The Hang Seng was in the green for a nano-second before declining -0.8% on volume that rose +6% from Friday but was only 80% of the 1-year average. The 208 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index declined -1.56% with financials +0.74%, real estate +0.53%, energy +0.5%, and staples +0.21%. Meanwhile, communication -3.45%, discretionary -2.41%, tech -2.17%, materials -1.79%, healthcare -0.95%, and industrials -0.65%. Hong Kong’s most heavily traded stocks by value were Tencent, which fell -3.49%, Meituan, which fell -5.14%, BYD, which gained +7.24%, Alibaba HK, which fell -1.96%, Geely Auto, which fell -6.68%, Xiaomi, which fell -2.36%, HK Exchanges, which fell -2.36%, Ping An Insurance, which gained +2.01%, SMIC, which fell -2.04%, and AIA, which gained +1.24%. Southbound Stock Connect volumes were average as Mainland investors sold a net -$724 million worth of Hong Kong stocks.

A-Share Update

Shanghai, Shenzhen, and the STAR Board diverged to end the session +0.03%, -0.58%, and -0.31% as volume declined -3.58% from Friday, which is 136% of the 1-year average. The 522 Mainland stocks within the MSCI China All Shares Index were off -0.24% with real estate +1.89%, utilities +1.65%, energy +1.13%, communication +0.77%, staples +0.53%, discretionary +0.44%, financials +0.4% and healthcare +0.03% while industrials -2.14%, materials -2.03% and tech -0.01%. The Mainland’s most heavily traded stocks by value were China Northern Rare Earth, which fell -10.01%, CATL, which fell -4.99%, Shanxi Meijin Energy, which gained +10%, BYD, which fell -4.87%, Qinghai Salt Lake, which fell -7.15%, Sany Heavy Industry, which fell -4.87%, Ganfeng Lithium, which fell -7.03%, Zijin Mining, which fell -1.06%, Cosco Shipping, which fell -4.94%, and Shanghai Awinic Technology, which gained +240.56%. Northbound Stock Connect volumes were moderate as foreign investors bought $957 million worth of Mainland stocks overnight.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.48 versus 6.48 Friday

- CNY/EUR 7.62 versus 7.64 Friday

- Yield on 1-Day Government Bond 1.45% versus 1.48% Friday

- Yield on 10-Year Government Bond 2.89% versus 2.88% Friday

- Yield on 10-Year China Development Bank Bond 3.23% versus 3.23% Friday

- Copper Price +0.54%