Here Comes the Rain Again

3 Min. Read Time

Key News

A very wet day here in the Northeast reminding me of the Eurythmics’ classic Here Comes the Rain Again. Market action suggests staying in bed would have been advised. Hopefully, we will be referencing the Eurythmics other hit Sweet Dreams soon enough.

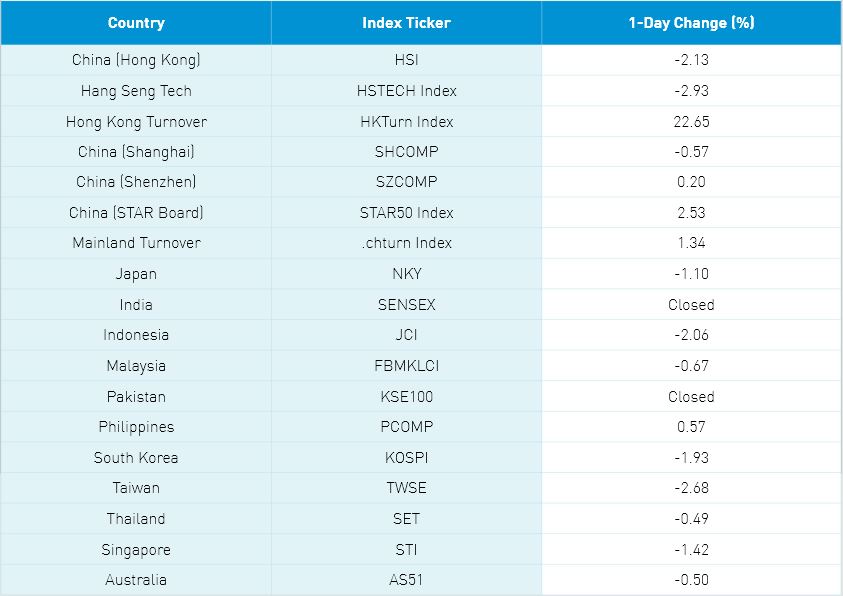

Asian equities were a sea of red as Taiwan, Japan, Hong Kong, Singapore, Indonesia, and South Korea underperformed. Mainland China held up well. US Fed bond tapering and Toyota auto production cuts were widely cited as negative catalysts. Markets appear to be increasingly worried about the delta variant’s effect on global growth, China’s Ningbo port shutdown being an example. Hong Kong suffered a broad sell-off with only 73 advancing stocks and 415 declining stocks with every sector lower.

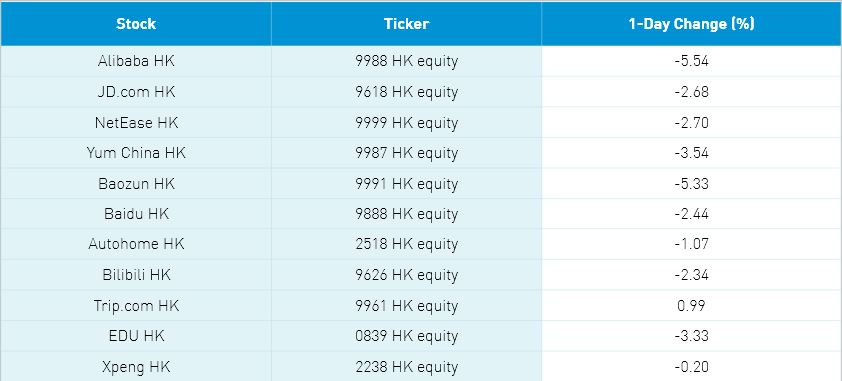

Tencent was hit despite yesterday's strong results as headlines scream about “regulation”. Yes, revenue growth was the slowest quarter in two years led by tepid game growth, though fintech growth was strong as it likely will be the largest revenue segment next quarter. Yesterday, I proposed my “air pocket” thesis that there are simply no professional buyers willing to step up to buy China internet stocks without clarity on regulation. Today’s price action leads me to believe that Asian active managers are late to the unload game. As evidence, Tencent experienced a large net sale day from Mainland investors via Southbound Stock Connect.

The internet space was off on reports that the Ministry of Industry and Information Technology (MIIT) mentioned several companies have a week to make their apps compliant with user data laws. I have no doubt they will! There was also chatter about Meituan having its commissions capped.

Luxury goods were smoked on “common prosperity” with Prada’s Hong Kong listing down -14.36%. The only bright spot in Hong Kong was the electric vehicle (EV) ecosystem, which also outperformed on the Mainland.

The Mainland market held up with growth names outperforming, such as the EV ecosystem, autos, rare earth metals, clean technology, and semiconductors. The STAR Board was up +2.53% as an exchange comprised of all things growth. Brokerage stocks had a very strong day while energy, materials, and industrial metal stocks were down as copper prices go off a cliff. Real estate was weak as “common prosperity” is being interpreted as a catalyst to implement a property tax.

Remember China’s census shows that incentivizing parents to have more kids is key. Making multi-bedroom apartments more affordable makes sense to me. Foreign investors were net sellers of Mainland stocks though the trend has been overweight Mainland stocks versus Hong Kong. Ping An Insurance and liquor stock Wuliangye Yibin saw the largest net selling. Mainland China bonds had a strong day.

H-Share Update

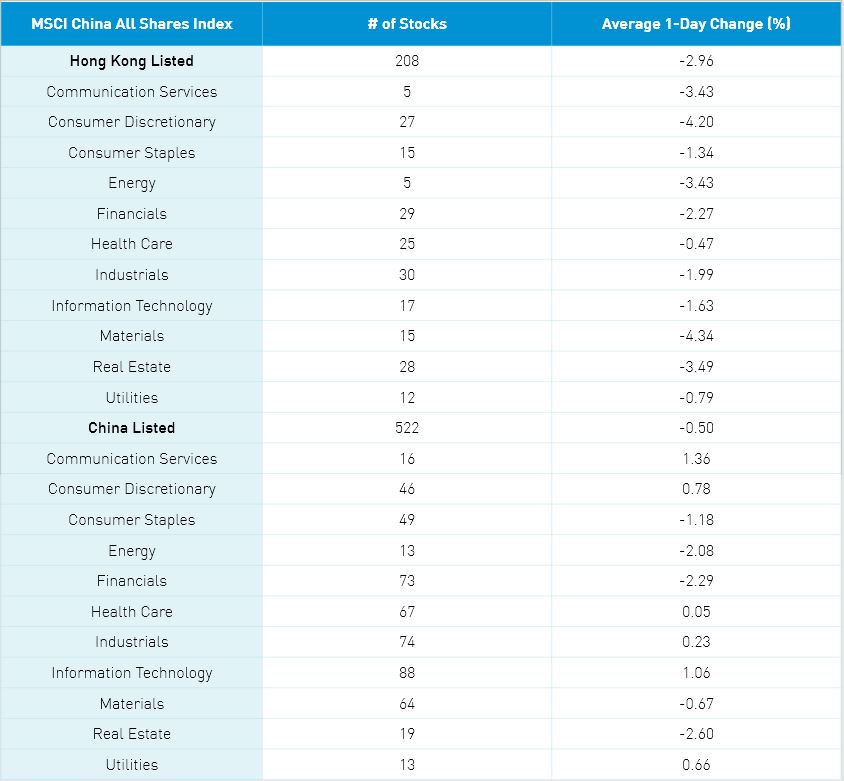

The Hang Seng opened lower and kept going in that direction closing -2.13% as volume increased +22.59% from yesterday which is 98% of the 1-year average. The 208 Chinese companies listed in Hong Kong within the MSCI China All Shares lost -2.93% led lower by materials -4.31%, discretionary -4.17%, real estate -3.45%, communication -3.4%, energy -3.39%, financials -2.23%, industrials -1.95%, tech -1.6%, staples -1.31%, utilities -0.76% and healthcare -0.43%. Hong Kong’s most heavily traded by value were Tencent -3.44%, Meituan -7.15%, Alibaba Hong Kong -5.54%, Ping An -5.78%, Geely Auto +2.1%, BYD +0.62%, Xiaomi -2.44%, Hong Kong Exchanges -2.03%, China Mobile flat, AIA +0.15%. Southbound Stock Connect volumes were moderate/high as Mainland investors sold $504mm of Hong Kong stocks as Southbound trading accounted for 14.8% of Hong Kong turnover.

A-Share Update

Shanghai, Shenzhen and STAR Board diverged closing -0.51%, +0.2% and +2.53% on volume +1.34% from yesterday which is 131% of the 1-year average. The 522 Mainland stocks within the MSCI China All Shares were off -0.49% as communication +1.37%, tech +1.07%, discretionary +0.79%, utilities +0.67%, industrials +0.23% and healthcare +0.06% while real estate -2.59%, financials -2.29%, energy -2.08%, staples -1.17% and materials -0.66%. The Mainland’s most heavily traded by value were Orient Securities +4.58%, broker East Money -3.4%, BYD +3.55%, China Northern Rare Earth +2.74%, Tianqi Lithium +10%, GF Securities +2.01%, Industrials Securities +2.14% and Ganfeng Lithium +6.33%. Southbound Stock volumes were elevated as foreign investors sold $1.662B of Mainland stocks today as Northbound trading accounted for 5% of Mainland turnover.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.49 versus 6.48 yesterday

- CNY/EUR 7.59 versus 7.59 yesterday

- Yield on 10-Year Government Bond 2.84% versus 2.85% yesterday

- Yield on 10-Year China Development Bank Bond 3.18% versus 3.18% yesterday

- Copper Price -2.00% overnight