Retail Sales & Industrial Output Slow in August, PBOC Indicates Policy Support

2 Min. Read Time

Upcoming Virtual Conference:

Join us on Wednesday, 22 September 2021, for a two-hour virtual conference for UK/European investors starting at 13:00 BST / 14:00 CET.

Policy, Performance, and the Two Sides to Reform in China

Click here to register.

Key News

Asian equities were mostly lower overnight on continuing delta concerns and lower-than-expected economic data coming out of China. US-listed China internet stocks were down yesterday on SEC Gary Gensler’s op-ed in the Wall Street Journal reminding us that the clock is ticking for US-listed Chinese companies to allow their audit papers to be reviewed by the PCAOB. As I said yesterday, this is nothing new and regulators from both countries need to develop a solution.

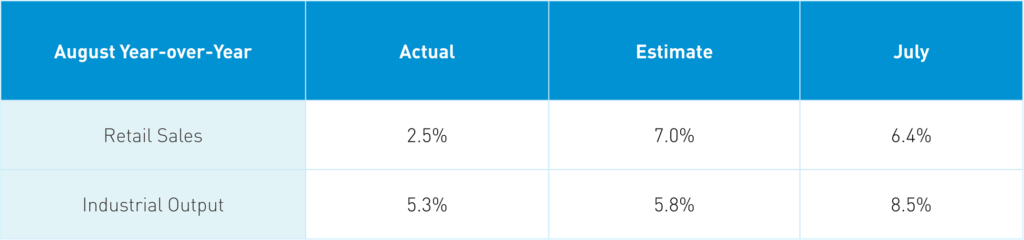

Retail sales were disappointing and can be linked to the worst outbreak of Covid-19 in the country since early 2020. Online retail sales most likely rose. China’s industrial output also came in below estimates and July’s 6.4% reading. We knew this was going to be a less than ideal release as massive flooding and lockdowns in August were bound to hurt production. From a long-term perspective, China is transitioning from being the world’s factory. Therefore, industrial production is likely to fall before rising again as the government supports the domestic semiconductor industry. The transition will take some time and cause some disruption.

Perhaps in response to the nonideal economic release, the People’s Bank of China (PBOC) rolled over RMB 600 billion worth of medium-term lending facilities (MLF) that came due today, in a sign of continuing policy support. As a reminder, the central bank has ample dry powder to counteract economic slowdowns.

Embattled developer Evergrande saw its shares fall -5.4% overnight as the government announced that its creditors should not expect interest payments due next week.

Macau gaming stocks were sold off overnight on news of new regulations for the casino industry. New rules include the requirement of government approval for profit distributions. The gaming industry has been a key target of Xi’s anti-corruption campaign and these regulations appear to be the final word. As we have noted in multiple commentaries, we believe regulators will focus on industries other than the internet sector to close out 2021.

H-Share Update

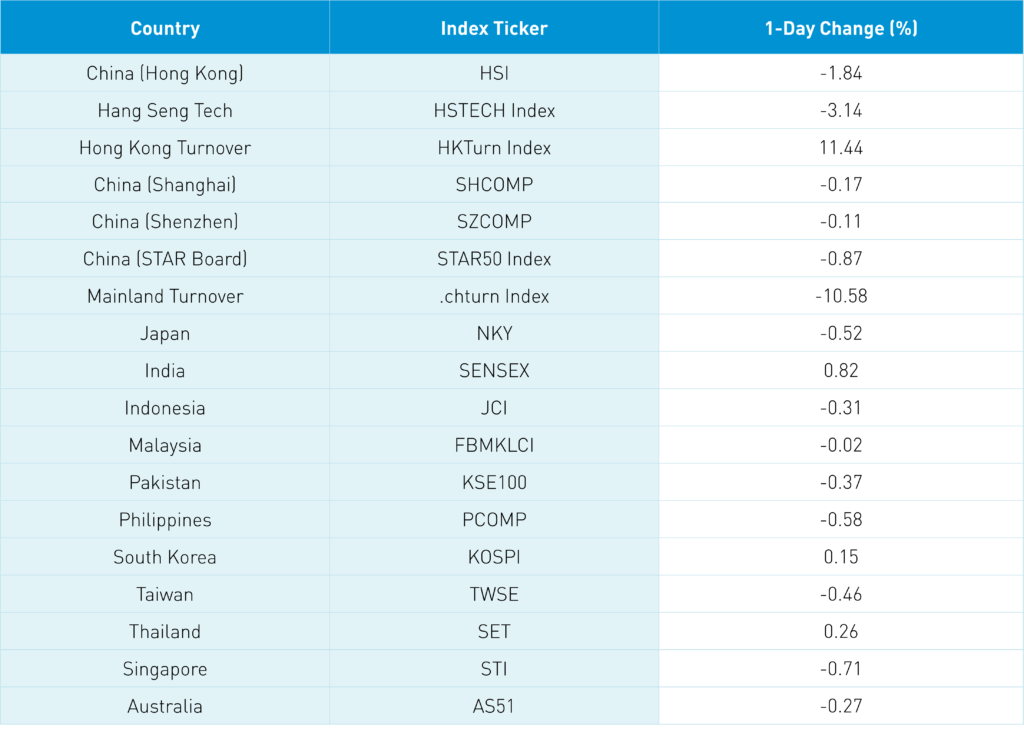

The Hang Seng Index fell -1.84% on volume that was +11% higher then yesterday. The Hang Seng Tech Index was fell -3.14% overnight. The most heavily traded stocks by Mainland investors via Southbound Stock Connect were Tencent, which fell -4.10%, Meituan, which fell -4.49%, Sunac, which fell -5.15%, and Dongyue Group, which gained +4.43%.

A-Share Update

Shanghai, Shenzhen, and the STAR Board closed -0.17%, -0.11%, and -0.87%, respectively, overnight. The most heavily traded stocks by foreign investors via Northbound Stock Connect were Kweichow Moutai, which fell -2.49%, Longi Green Energy Technology, which gained +2.67%, China Merchants Bank, which fell -1.34%, and Jiangxi Ganfeng Lithium, which gained +7.91%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.44 versus 6.43 yesterday

- CNY/EUR 7.60 versus 7.61 yesterday

- Yield on 1-Day Government Bond 1.78% versus 1.83% yesterday

- Yield on 10-Year Government Bond 2.90% versus 2.89% yesterday

- Yield on 10-Year China Development Bond 3.22% versus 3.21% yesterday

- Copper Price -0.54% overnight