Investors Lighten Up In Advance of Market Holiday

3 Min. Read Time

Upcoming Virtual Conference:

Join us on Wednesday, 22 September 2021, for a two-hour virtual conference for UK/European investors starting at 13:00 BST / 14:00 CET.

Policy, Performance, and the Two Sides to Reform in China

Click here to register.

Key News

I am speaking at the CFA Society Buffalo today at noon EST. Joining is free/open to all if interested! Not had a buffalo wing yet...click here to register.

It was an ugly night in Asia as India and the Philippines overperformed and Mainland China prepared for a market holiday on Monday and Tuesday. A brutal washout in Hong Kong with only 56 advancers versus 431 decliners in the broader Hang Seng Composite. I had hoped we would have a rally at quarter-end as many active managers are overweight in India and underweight in China. Global and EM mandates would “force” them back into China if a rally materialized. Markets are not cooperating with my thesis. The Financial Times had an article from a global manager who has 1% in China weight despite China being 4% of global equity benchmarks as evidence of active managers being underweight.

Leveraged real estate developer Evergrande continues to weigh on investor sentiment along with the recent regulatory consultation on Macao casinos and the weak August economic data. Evergrande has historically had nine lives having staved off historical solvency issues. I find it interesting that Southbound Bond Connect starts September 24th which will allow Mainland investors access to Hong Kong’s bond market. It would make sense to me to get the Evergrande situation stabilized prior to Mainland mutual funds loading up on Hon Kong bonds.

Hong Kong-listed internet stocks were largely off on some chatter of no new video games, but it’s hard to substantiate. Mainland markets were off on the Evergrande news and August economic data with lithium stocks getting hammered after an official from the Ministry of Industrial and Information Technology (MIIT) said EV prices are too high, being driven by high input prices including lithium, cobalt, and nickel, leading investors to shoot first and ask questions later.

The three most heavily traded Mainland stocks were lithium plays all limit down -10%. EV production increased to 309k units in August which is two times August 2020’s production and up 8% from July according to media outlet Yicai. We do have a market holiday in China next Monday and Tuesday so investors may have been looking for excuses to lighten up.

Investors will be looking for policy guidance following the August data. Yes, we had bad weather/flooding in August and Delta breakouts, but poor retail sales, driven by very poor restaurant activity, are problematic. Foreign investors lightened their Mainland exposure in advance of the holidays.

August FDI in China was a market non-event though it's worth noting August YTD FDI was 22.3% versus July’s 25.8%, indicating the pace of FDI is slowing. Hang Seng closed lower than the mid-August low while the Shanghai Comp broke out and is testing previous resistance as support. Shenzhen closed just below its 50-day moving average with the 100-day support nearby.

Tomorrow will be one of the biggest trading days of the year as we have Quad Witching, the expiration of stocks, index futures, and options, along with the FTSE Russell and S&P Index rebalances. Pro golfers call Saturday moving day as you need to get yourself in a position to win on Sunday. Similarly, professional investors use the surge of liquidity to position themselves as they can exit and add to positions. It will be interesting to read the tea leaves in tomorrow’s trading.

H-Shares Update

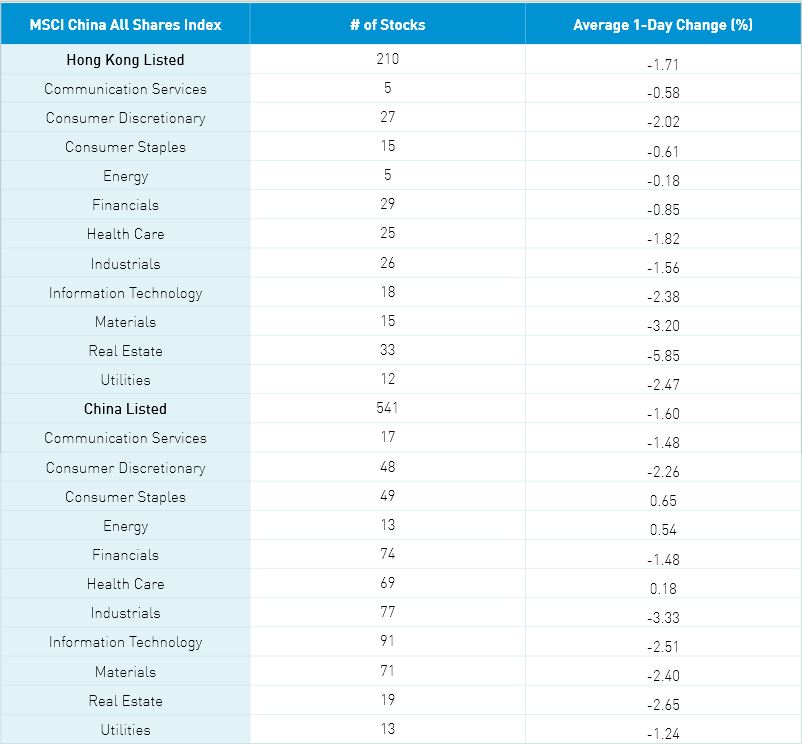

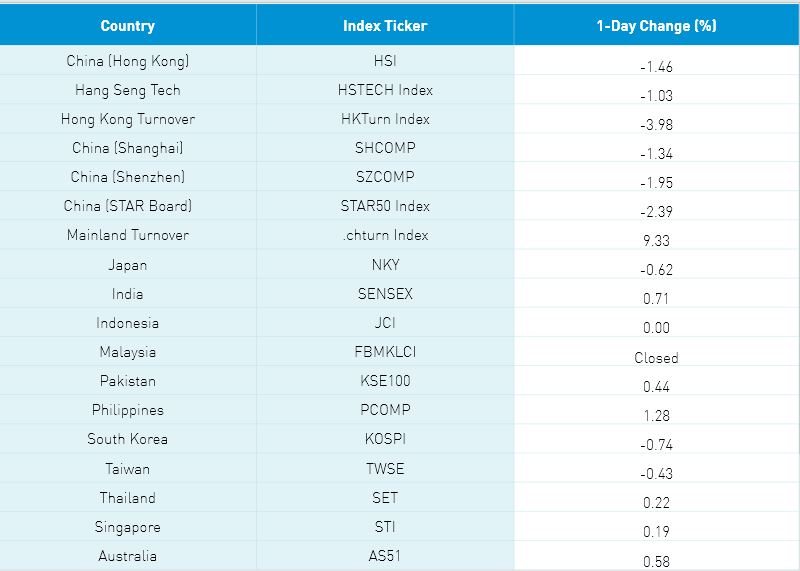

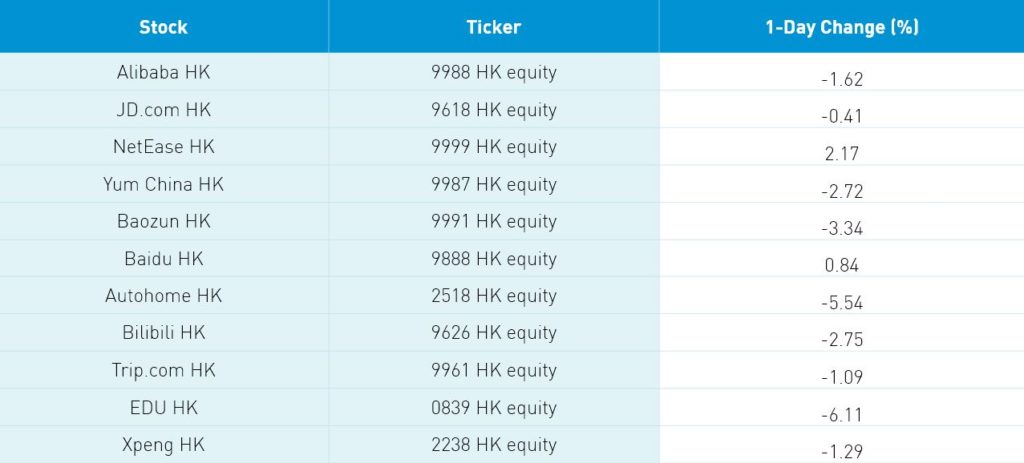

The Hang Seng opened lower and stayed there closing -1.46% as volume increased +23% from yesterday. The 210 Chinese companies listed in Hong Kong within the MSCI China All Shares fell -1.71% led by real estate -5.85%, materials -3.2%, utilities -2.47%, tech -2.38%, discretionary -2.02%, healthcare -1.82%, and industrials -1.56%. Hong Kong’s most heavily traded by value were Tencent -0.53%, Alibaba HK -1.62%, Meituan -0.6%, Galaxy Entertainment -0.13%, Sands China -7.96%, AIA -2.11%, Ping An +1.23%, BYD -3.64%, Xiaomi -2.37% and HK Exchanges -2.44%. Southbound Stock Connect is closed today due to the Mainland market’s being closed Monday and Tuesday.

A-Shares Update

Shanghai, Shenzhen, and STAR Board fell from start to finish closing -1.34%, -1.95% and -2.39% as volume increased +9.33% from yesterday which is 155% of the 1-year average. The 541 Mainland stocks within the MSCI China All Shares closed -1.6% with staples +0.65%, energy +0.54% and healthcare +0.18% while industrials -3.33%, real estate -2.66%, tech -2.51%, materials -2.41% and discretionary -2.26%. The Mainland’s most heavily traded stocks were Tianqi Lithium -10%, Ganfeng Lithium -10%, Qinghai Salt Lake Industry -10.01%, China Northern Rare Earth -4.23%, broker East Money -3.48%, Kweichow Moutai +1.38%, Jiangxi Special Electric Motor -6.27%, COSCO Shipping -5.54%, TBEA -5.61%, and liquor stock Wuliangye Yibin -0.76%. Foreign investors sold -$467mm of Mainland stocks today as Northbound Stock Connect trading accounted for 6.1% of Mainland turnover.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.45 versus 6.44 yesterday

- CNY/EUR 7.59 versus 7.60 yesterday

- Yield on 10-Year Government Bond 2.89% versus 2.90% yesterday

- Yield on 10-Year China Development Bond 3.21% versus 3.22% yesterday

- Copper Price +0.62% overnight