Offshore RMB Does Not React to Evergrande Wind-Down, Week in Review

3 Min. Read Time

Upcoming Virtual Conference:

Join us on Wednesday, 22 September 2021, for a two-hour virtual conference for UK/European investors starting at 13:00 BST / 14:00 CET.

Policy, Performance, and the Two Sides to Reform in China

Click here to register.

Week in Review

- A Monday Financial Times article reported that Ant Group will separate its lending business from its payments business, quoting an unidentified source. While the company has yet to make an official announcement, the split would be in line with guidance received from regulators.

- Baidu began testing its “Apollo Go” robo-taxis this week in Shanghai. The test of the technology is significant as many global mobility players such as Uber are no longer working to make robo-taxis a reality.

- China’s retail sales grew by +2.5% year-over-year in August, according to a Wednesday economic release, far below the +7% growth forecast as the country’s consumer market was set back by the worst covid-19 outbreak since early 2020.

- Asian equities compounded weekly declines on Thursday as investors await policy guidance following China’s worse-than-expected economic release on Wednesday. The PBOC signaled a supportive stance by rolling over medium-term lending facilities (MLF) that were due to expire this week.

Key News

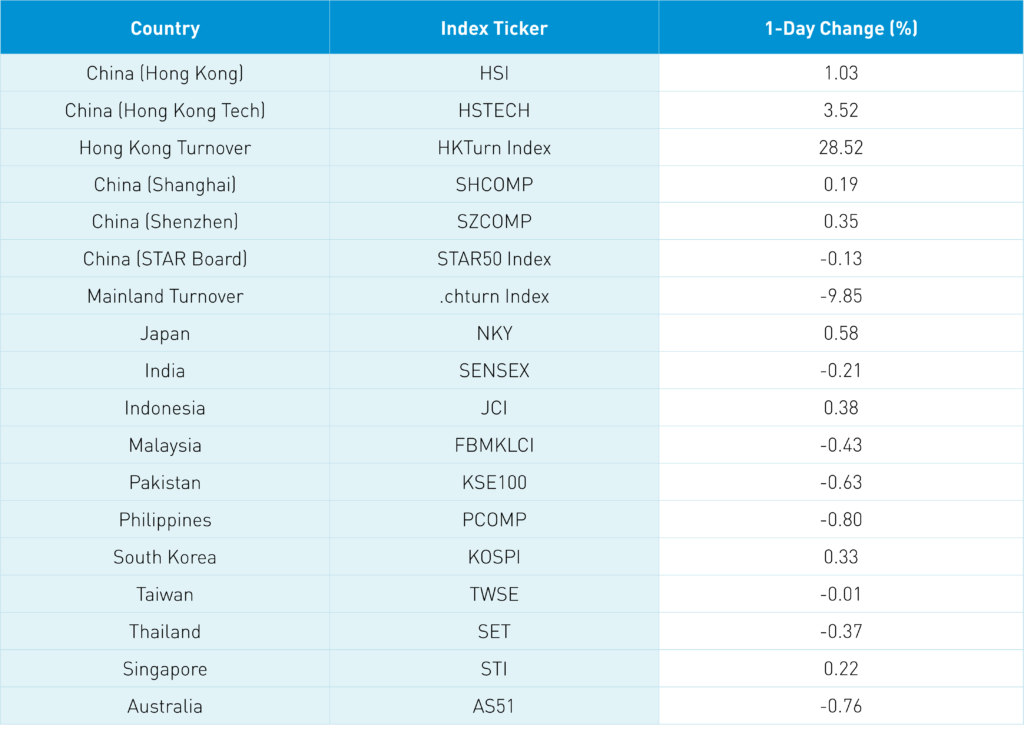

Asian equities were largely higher as Hong Kong outperformed led by internet stocks. Investors appeared to be in good spirits in advance of the long weekend as Mainland China, Japan, and Taiwan will be closed Monday. However, there was precious little to speak of from a “news” perspective. Meanwhile, regional volumes were driven higher by the FTSE Russell rebalance and Quad Witching (the expiration of options contracts).

The PBOC’s injection of $14 billion worth of liquidity into the financial system helped soothe investor concerns about Evergrande. However, the move was likely driven by the need for cash before the long weekend.

A People’s Daily editorial claimed that Evergrande is not too big to fail. However, we now know that it is. A few years ago, insolvent companies including HNA Group, Anbang Insurance, and Fosun were going to implode China, according to the media narrative. But, the companies were broken up, their debt was distributed, and life went on. China will not let the first domino, which could be Evergrande, fall. CNH, the version of China’s currency that trades during US market hours, shows little worry. CNH’s volatility is very low, indicating that the market is not concerned.

There were several interesting sector moves overnight. Healthcare absolutely ripped, driven by the EU marketing approval of a key drug produced by Beigene. Meanwhile, lithium stocks were hit again, bringing down miners and other metal plays. The lithium space, along with coal and steel, has outperformed recently so some profit-taking is not that surprising. Positive remarks from the National Development and Reform Commission on clean energy and the Ministry of Transportation on electric vehicle (EV) usage increasing, both of which helped the broader cleantech space including EV, wind, and solar names. Energy names took it on the chin as crude prices eased a touch overnight.

Both Northbound and Southbound Stock Connect were closed today in advance of China’s market holidays on Monday and Tuesday. Tencent bought back another 230,000 shares overnight.

H-Share Update

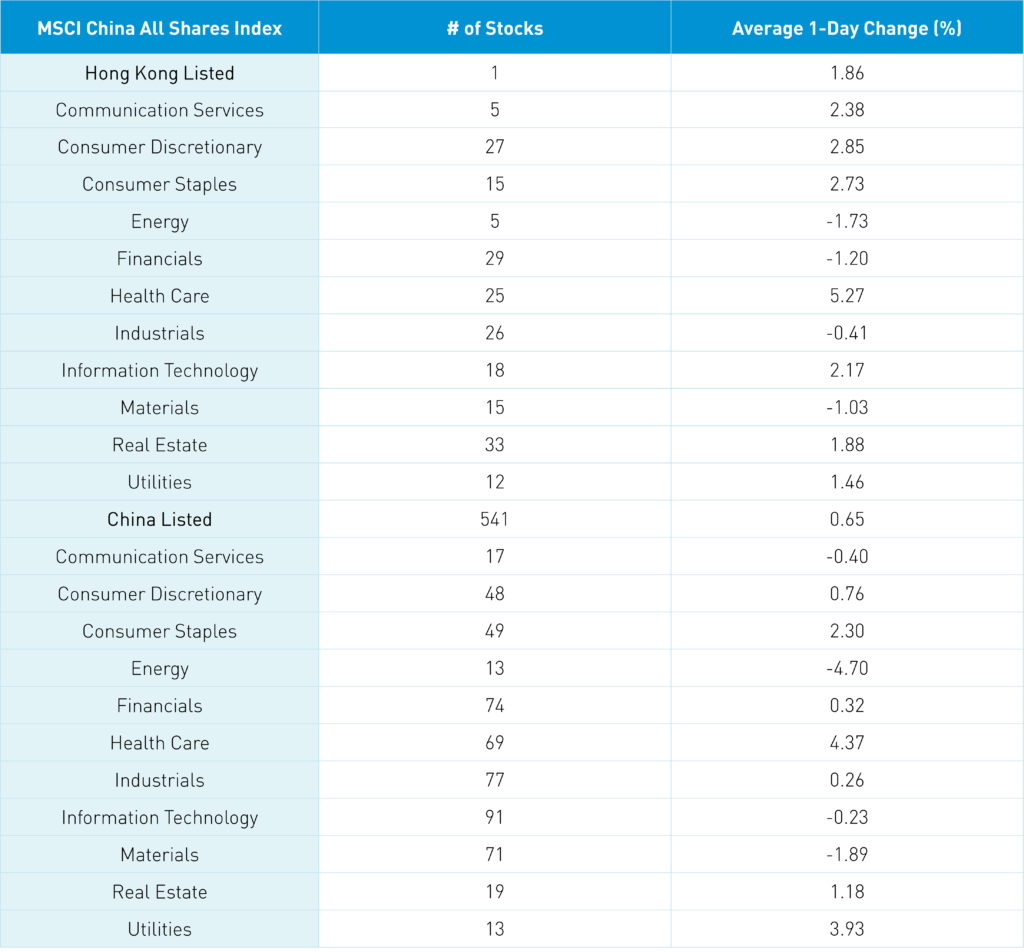

The Hang Seng opened lower but snapped back, rising across the trading day to close +1.03% on volume that was +51% higher than yesterday. The 210 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index gained +1.87% led by healthcare +5.28%, discretionary +2.86%, staples +2.74%, communication +2.39%, tech +2.17%, real estate +1.89%, and utilities +1.7%. Meanwhile, energy -1.72, financials -1.2% and materials -1.2%. Hong Kong’s most heavily traded stocks by value were Tencent, which gained +2.39%, Kuaishou Technology, which gained +6.22%, BeiGene, which ripped +20.29%, Ping An Insurance, which fell -5.05%, Meituan, which gained +3.53%, Alibaba HK, which gained +2.24%, Baidu, which gained +2.38%, AIA, which was flat, JD Health, which gained +9.52%, and BYD, which gained +3.37%.

A-Share Update

Shanghai, Shenzhen, and the STAR Board bounced around the room opening higher then falling into the red before rebounding to close +0.19%, +0.35%, and -0.13%, respectively, on volumes that were -9.85% lower than yesterday, which is 140% of the 1-year average. The 541 Mainland stocks within the MSCI China All Shares Index gained +0.66% led by healthcare +4.37%, utilities +3.93%, staples +2.3%, and real estate +1.18%. Meanwhile, energy -4.69% and materials -1.88%. The Mainland’s most heavily traded stocks by value were Tianqi Lithium, which fell -5.12%, China Northern Rare Earth, which fell -6.32%, China Three Gorges Renewables, which gained +9.97%, Kweichow Moutai, which gained +2.93%, Gangfeng Lithium, which fell -2.8%, Inner Mongolia BaoTou Steel, which fell -6.63%, Yunnan Yuntianhua, which fell -4.02%, Jiangxi Special Electric Motor, which gained +2.51%, and Longi Green Energy, which fell -1.00%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.46 versus 6.46 yesterday

- CNY/EUR 7.60 versus 7.60 yesterday

- Yield on 1-Day Government Bond 1.83% versus 1.83% yesterday

- Yield on 10-Year Government Bond 2.88% versus 2.88% yesterday

- Yield on 10-Year China Development Bank Bond 3.20% versus 3.21% yesterday

- Copper Price -1.15% overnight