Liquor Stocks Weigh on Shanghai While Internet Stocks Lift Hong Kong

3 Min. Read Time

Key News

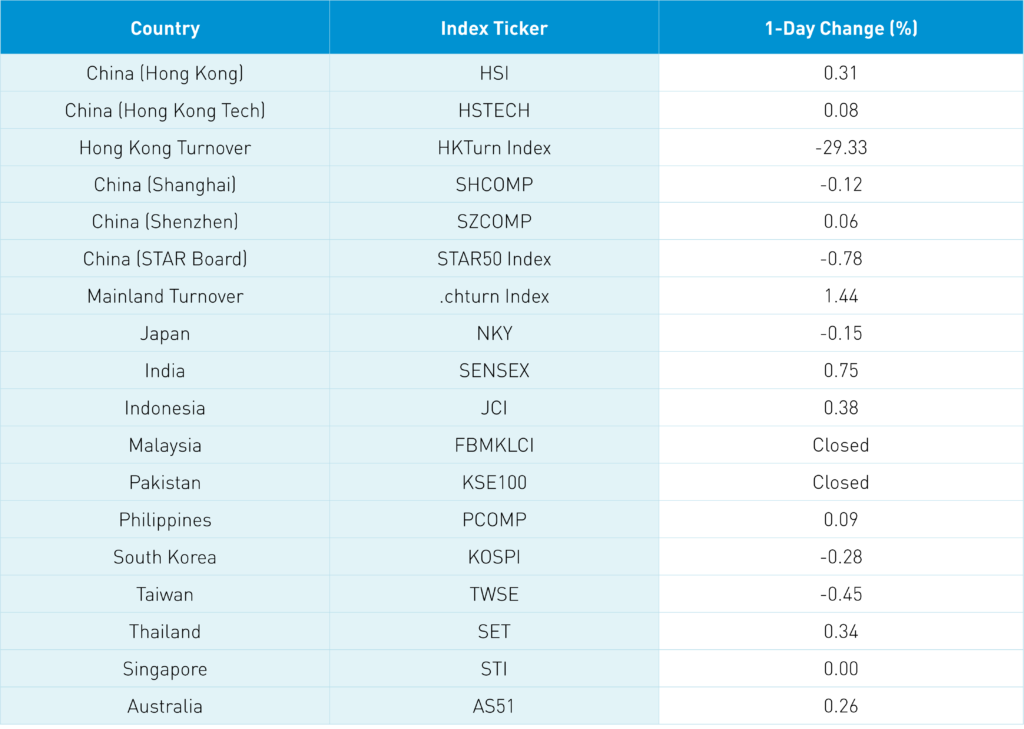

Asian equities were largely higher though Japan, South Korea, and Taiwan were off. China was mixed overnight and Hong Kong and India closed higher.

Over the weekend PBOC head Yi Gang stated that Evergrande’s problems are “containable”. Meanwhile, had a negative Wall Street Journal article on Alibaba documenting increased competition, which has caused the company’s market share in E-Commerce to fall from 78% in 2015 to 51% today. Alibaba’s Hong Kong share class did not seem to care as it rose +0.68% overnight as internet names had a good day overnight. However, Tencent saw another small net sale by Mainland investors via Southbound Stock Connect.

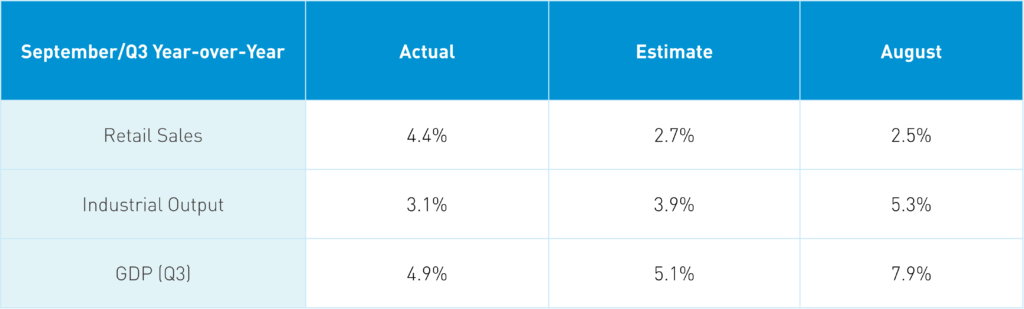

As China gets further away from its Q1 2020 quarantine, the year-over-year comparisons get harder as the low bar comparison rises. However, retail sales were a bright spot in September, coming in well above estimates. The release opens debate on whether the PBOC will ease monetarily by cutting the bank reserve requirement ratio (RRR) or the loan prime rate (LPR). It is possible that regulation and carbon commitments, which have been ramped up lately, might be eased temporarily to help the economy.

News over the weekend of a consumption tax hit liquor stocks hard as Kweichow Moutai and Wuliangye Yibin fell -6.1% and -8.11%, respectively. Both stocks were sold nearly 2 to 1 in Northbound Stock Connect, which led to a healthy exodus of $1.25 billion worth of Mainland stocks by foreign investors who decided to shoot first and ask questions later. Clean technology plays had a strong day in both Hong Kong and the Mainland market as the electric vehicle (EV) ecosystem, solar, wind, and metal stocks outperformed.

Hong Kong Exchanges launched MSCI China A50 Index futures today. This is the first futures contract approved by the China Securities Regulatory Authority (CSRC), China’s version of the SEC, as Singapore listed FTSE A 50 was never given permission to trade. 1,395 contracts were traded, which is a value of nearly $100 million. The launch eliminates one of three MSCI concerns on expanding the inclusion of Shanghai and Shenzhen stocks in their indexes. The other issues are that Chinese stocks settle on trade date versus the rest of the world’s T+2 (trade date plus two days) and the misalignment of Hong Kong and Mainland Chinese market holidays. We also heard an announcement that foreign investors that use QFII, a quota program that provides access to Mainland stocks and bonds, will be allowed to trade financial derivatives, including commodities.

Today, it was announced that Goldman Sachs will be allowed to take full ownership of its Mainland securities business. The move follows JP Morgan’s approval two months ago to do the same.

H-Share Update

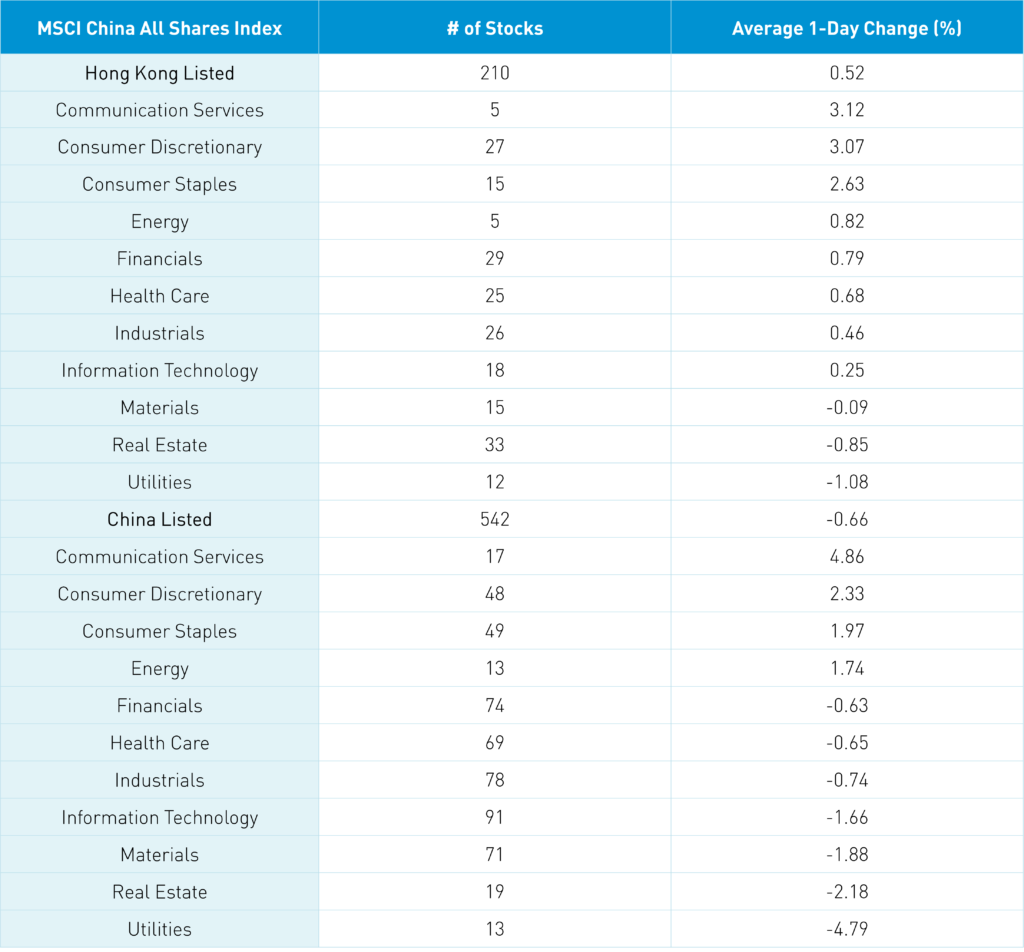

The Hang Seng opened higher and slipped into the red for most of the trading day before staging a late-day rally, lifting the index higher to close at +0.31% as volume plunged -29%, which is only 74% of the 1-year average. The 210 Chinese companies listed in Hong Kong and within the MSCI China All Shares Index gained +0.52% led by energy +3.12%, materials +3.07%, healthcare +2.64%, and industrials +0.82%. Meanwhile, utilities -1.08% and financials -0.85%. Hong Kong’s most heavily traded stocks by value were Tencent, which gained +0.28%, Meituan, which fell -0.14%, Alibaba HK, which gained +0.68%, BYD, which gained +1.39%, Anta Sports, which gained +4.45%, AIA, which fell -0.4%, Wuxi Biologics, which gained +5.03%, Geely Auto, which gained +1.64%, Kuaishou Technology, which fell -3.01%, and Li Ning, which gained +2.82%. Southbound Stock Connect volumes were light as Mainland investors sold $13 million worth of Hong Kong stocks today as Southbound Connect trading accounted for 11.4% of Hong Kong turnover.

A-Share Update

Shanghai, Shenzhen, and the STAR Board diverged to close -0.12%, +0.06%, and -0.78%, respectively, on volumes that were up +1.44% from Friday, which is 102% of the 1-year average. The 542 Mainland stocks within the MSCI China All Shares Index were off -0.65% with energy +4.86%, utilities +2.33%, materials +1.98%, and industrials +1.75%. Meanwhile, staples -4.79%, real estate -2.18%, healthcare -1.87%, and communication -1.66%. The Mainland’s most heavily traded stocks by value were Kweichow Moutai, which fell -6.1%, Wuliangye Yibin, which fell -8.11%, CATL, which gained +4.57%, Tianqi Lithium, which gained +4.63%, BYD, which gained +0.91%, Zijin Mining, which gained +0.87%, Longi Green Energy, which gained +1.21%, Ganfeng Lithium, which gained +5.63%, Luzhou Laojiao, which fell -4.16%, and broker East Money, which fell -0.77%. Northbound Stock Connect volumes were moderate/light as foreign investors sold -$1.25 billion worth of Mainland stocks as Northbound trading accounted for 5.9% of Mainland turnover.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.43 versus 6.44 Friday

- CNY/EUR 7.47 versus 7.47 Friday

- Yield on 1-Day Government Bond 1.71% versus 1.71% Friday

- Yield on 10-Year Government Bond 3.04% versus 2.97% Friday

- Yield on 10-Year China Development Bank Bond 3.36% versus 3.30% Friday

- Copper Price