US-China Rhetoric Weighs on Stocks

3 Min. Read Time

US-listed China ADR Recap From Yesterday

We had a triple whammy starting at 10 am when the FCC announced China Telecom would be banned from operating in the US. I doubt the move has any financial impact on the company, but the timing post-Janet Yellen’s conversation with Vice Premier Liu He the night before was interesting.

Also starting at 10 am, the US House Finance Subcommittee on Investor Protection, Entrepreneurship, and Capital Markets held a session titled “Taking Stock of China, Inc: Examining Risks to Investors and the U.S. Posed by Foreign Issuers in U.S. Markets”. The four “expert” witnesses were mega-China bears so it is hardly surprising that the tone was negative. The emphasis was all on risks with no examination of the rewards. There were multiple inaccurate statements that left me somewhat dismayed. Ultimately, institutional investors such as ourselves will simply convert out of the US ADRs into the Hong Kong share classes.

Last but not least, we had Secretary of State Anthony Blinken implicitly recommend Taiwan’s inclusion in the UN. It is worth noting that CNH, China’s currency that trades during US trading hours, did not move on the news. As we have stated in the past, CNH is usually a good barometer for the actual economic implications of a given news story. Several trading desks felt that the sharp sell-off was exacerbated by the recent strength of the sector, which led to some short-term profit-taking. We are still above the 50-day moving average, which should act as a support level.

Coincidentally, we mentioned yesterday’s 14th Five Year Plan for E-Commerce Development. My colleague Derek did a great job translating the plan for me. According to the report, by 2025, E-Commerce transactions are expected to reach RMB 46 trillion ($7.2 trillion) versus RMB 37.2 trillion in 2020. E-Commerce-related employment is expected to rise to 70 million by 2025 from 60.15 million in 2020.

Key News

Asian equities were lower overnight. China’s September industrial profits rose by +16.3% to RMB 738 billion versus August’s 10.1% rise driven by higher input prices. Higher commodity prices are being baked into the prices of manufactured goods, another sign of increasing inflation. Year-to-date, industrial profits are up 44.7% year-over-year.

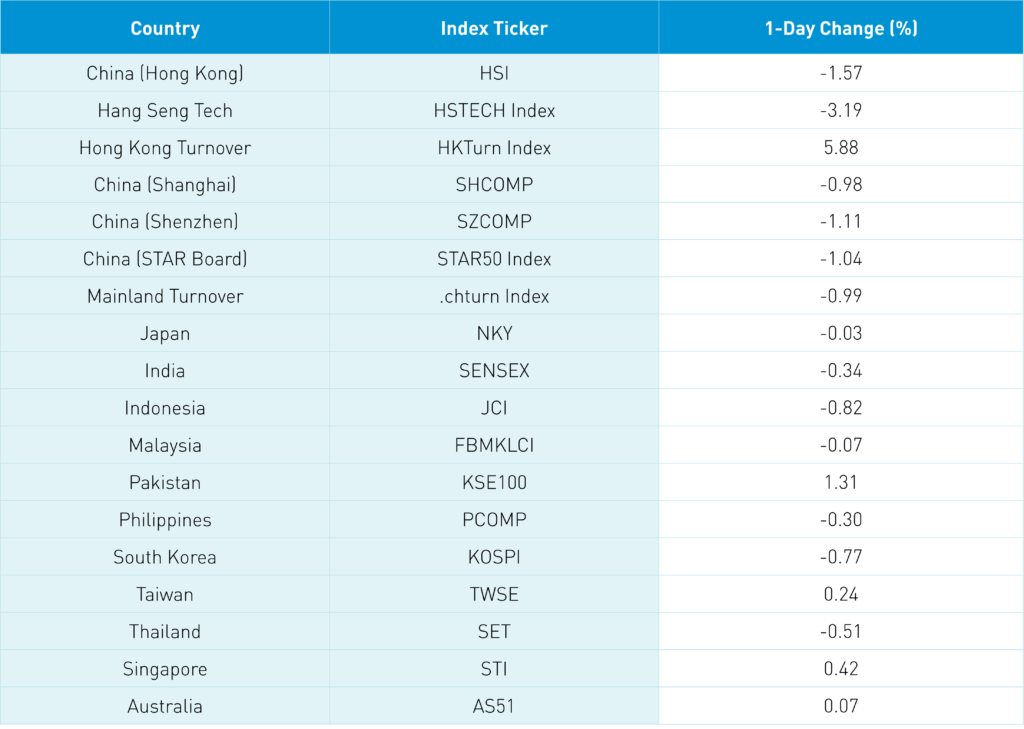

The positive economic release was a non-event as the Hang Seng was off -1.57%, led lower by internet stocks following yesterday's sell-off in the US. Volumes were off though breadth was nearly 4 to 1 decliners to advancers as utilities was the only positive sector. Southbound Stock Connect volumes were light as Mainland investors were small net sellers of Hong Kong stocks including Tencent, which fell -2.99%, and Meituan, which fell -5.09%. Kuaishou Technology was off -2.77% though saw net buying via Southbound Stock Connect.

Shanghai, Shenzhen, and the STAR Board were off -0.98%, -1.11%, and -1.04%, respectively, on volumes that were just above the 1-year average. It was a risk-off day as decliners outpaced advancers by nearly 4 to 1. The only bright spot was the clean energy technology space as the electric vehicle (EV) ecosystem, solar, wind, and hydrogen stocks were strong performers following Monday's release of clean energy targets. The State Council reiterated carbon targets overnight. A separate piece stated that EVs should account for 25% of all auto sales by 2025, which would be up from 5% in 2020, with a target of 40% by 2030. Ambitious!

Northbound Stock Connect volumes were light as foreign investors sold $475 million worth of Mainland stocks today. The PBOC was active again in injecting liquidity into the financial system. CNY was off a touch versus the US dollar overnight along with bonds and copper.

S&P and MSCI have proposed another update to the Global Industry Classification System (GICS), a long-winded way of saying sectors. The most notable changes include the elimination of the internet retailing subsector, which is a pure-play E-Commerce sub-sector, and breaking out renewable versus non-renewable energy providers. The former change could have an effect on thematic ETFs as they may lose out on companies solely focused on E-Commerce, as the index providers believe many brick and mortar companies now sell online. That is true, though pure plays still exist. Our approach has always been bottom-up, so it is a non-event for us, though I suspect others might not be so lucky.

If Helen of Troy launched a thousand ships, Luckin Coffee launched a thousand pessimists. The company announced having paid a $175 million class-action settlement following its fraud debacle last year. It is worth noting that the fraud was discovered by its auditor at the time, Ernst & Young. Ironically, the company’s stock is trading at $15 versus $25 in March 2020, which was just prior to the fraud news.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.39 versus 6.38 Yesterday

- CNY/EUR 7.42 versus 7.41 Yesterday

- Yield on 10-Year Government Bond 2.98% versus 2.98% Yesterday

- Yield on 10-Year China Development Bank Bond 3.32% versus 3.32% Yesterday

- Copper Price -0.78% overnight