Growth Concerns & Fed Tapering Uncertainty Weigh on Asian Equities

2 Min. Read Time

Upcoming Virtual Conference:

Join us on Tuesday, November 16th 2021 at 8:20 EDT for

China's Balancing Act: How Policy Reforms and Innovation are Reshaping the World's Second Largest Economy

Click here to register.

Key News

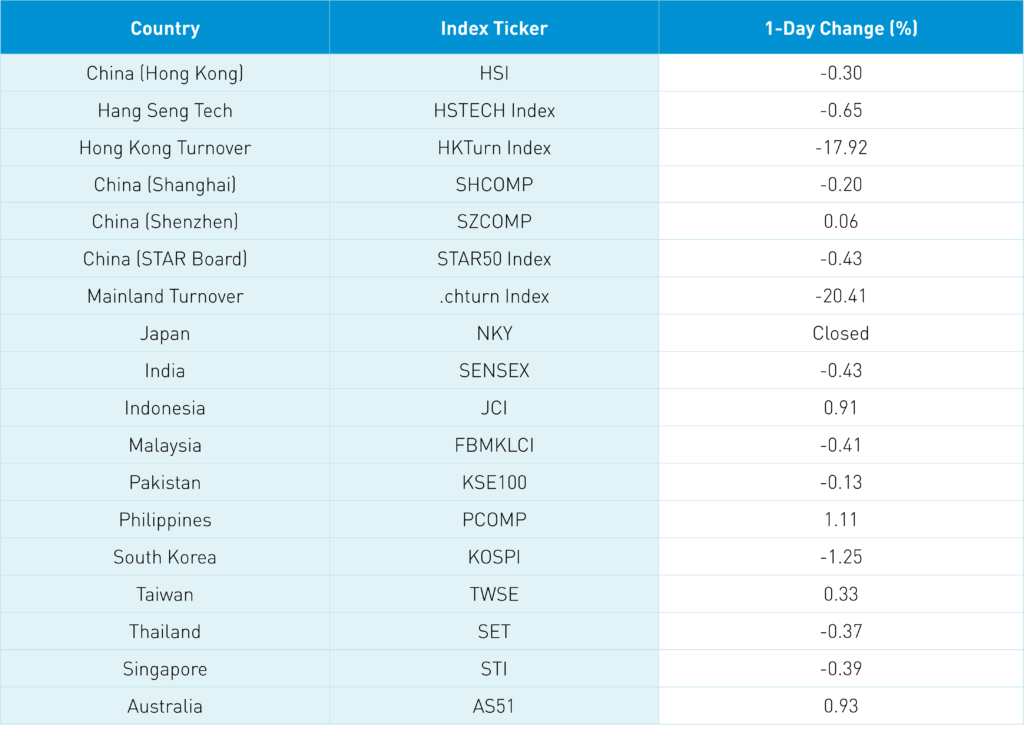

Asian equities were largely off today on light volumes as investors wait on the Fed’s tapering outlook with Japan on holiday and the Philippines outperforming.

Going into today’s session we had several negative headlines including Premier Li stating that China’s economy faces “downward pressure” though he offered a solution via tax and fee cuts for small and medium companies, which we saw at the end of October as companies in manufacturing were allowed to defer taxes until next year.

We also had PBOC head Yi Gang reminded fintech companies to abide by the new user data protection law. Meanwhile, concerns that the Biden administration could ban Chinese-made solar panels weighed heavily on solar names overnight. The irony is that there has been talk of rolling back China tariffs in order to curb inflation.

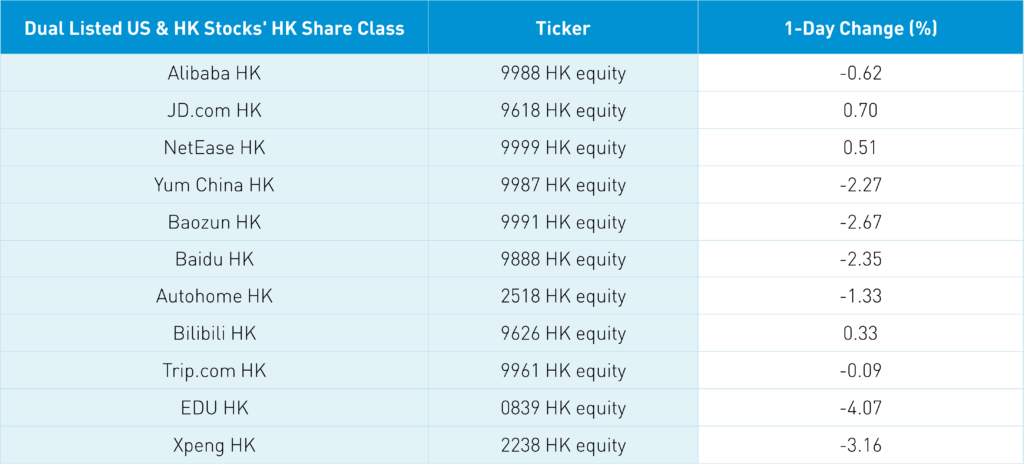

We also had a Bloomberg article widely circulated on Alibaba’s US listing seeing sales based on SEC 13F filings stating investors “dumped over 16 million shares”. The article failed to look at Alibaba’s Hong Kong listing, which showed that many of the “sales” in Alibaba’s US listing were conversions into the Hong Kong share class. There was some chatter about management changes at Bytedance, though it is a private company. We also had reports on China’s efforts to curtail the Delta virus.

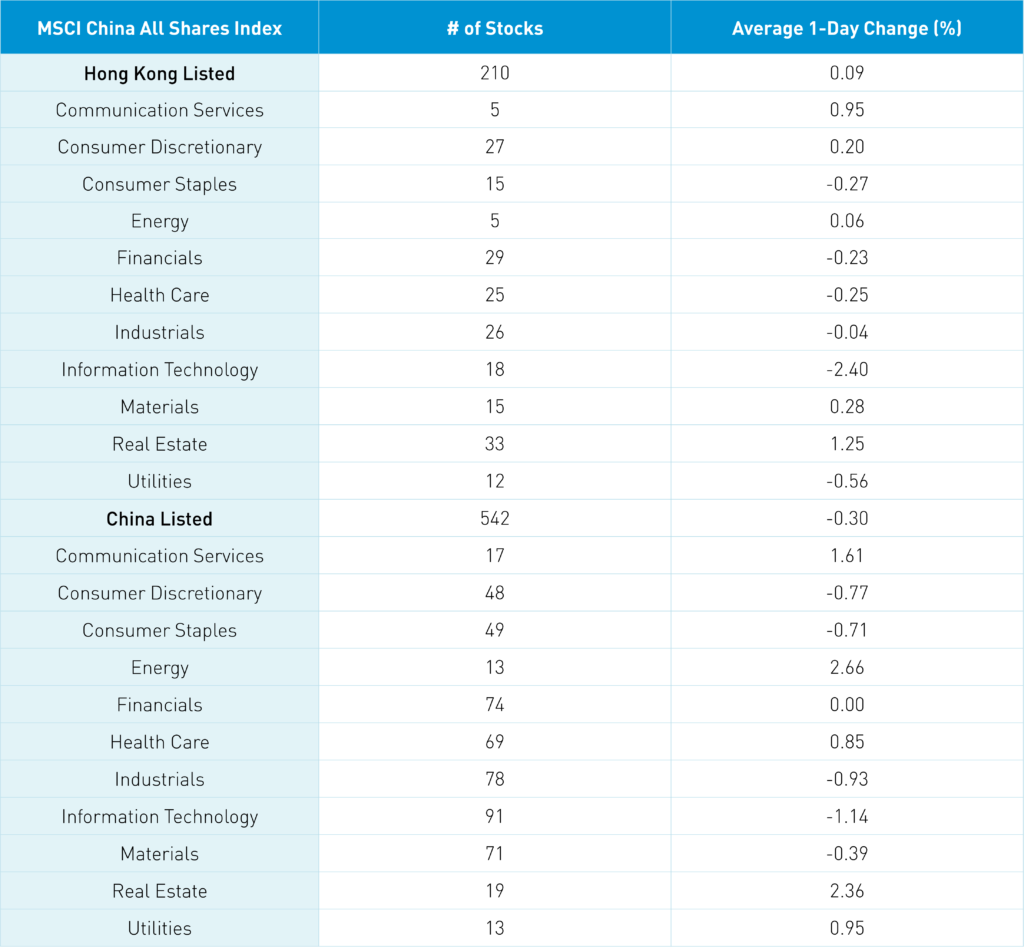

The Hang Seng was off -0.3% though Hong Kong’s volume was only 70% of the 1-year average. The index managed to close above 25k at 25,024. The October Caixin China PMI Services, which had its survey done by IHS Markit, beat estimates at 53.8 versus estimates of 53.1 and September’s 53.4. Hong Kong-listed internet stocks were mixed though companies with a US dual listing were not down nearly as much as yesterday’s US price action which should lead them to pop today.

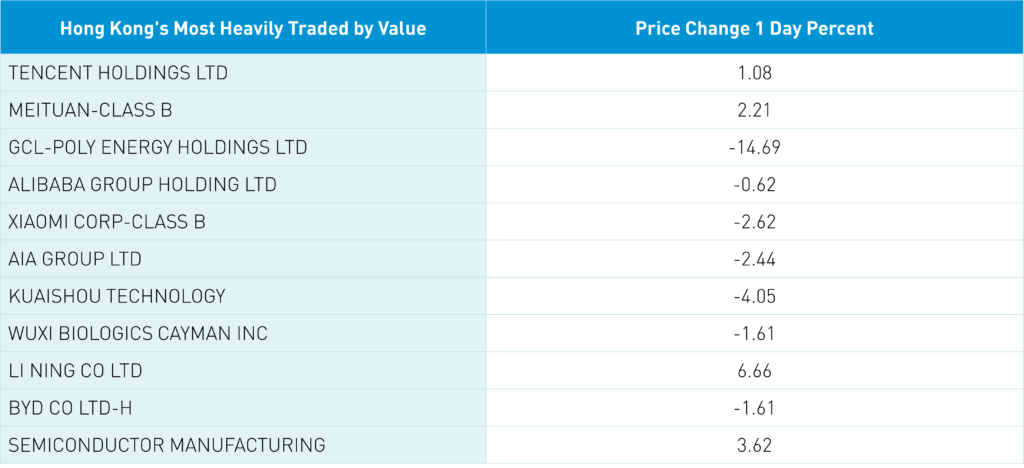

Tencent and Meituan gained +1.08% and +2.21%, respectively, as Mainland investors were net buyers via Southbound Stock Connect. Tencent announced the rollout of several new semiconductor chips, highlighting the company’s ingenuity.

Mainland markets diverged as Shanghai fell -0.2%, Shenzhen gained +0.06%, and the STAR Board fell -0.43% on volumes that were equal to the 1-year average. It is interesting to note that real estate was a top-performing sector in the Mainland and Hong Kong. Energy was led higher by coal stocks as China needs to stockpile ahead of the winter while clean energy names were off today. Foreign investors bought $114 million worth of Mainland stocks today via Northbound Stock Connect. Chinese Treasuries were off while CNY and copper rallied a touch.

I stumbled upon the below article written by a US truck driver on his take on the supply chain problems. Unfortunately, the problem has multiple causes which likely means it isn’t going away. A worthwhile read! https://medium.com/@ryan79z28/im-a-twenty-year-truck-driver-i-will-tell-you-why-america-s-shipping-crisis-will-not-end-bbe0ebac6a91

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.40 versus 6.40 Yesterday

- CNY/EUR 7.41 versus 7.42 Yesterday

- Yield on 10-Year Government Bond 2.94% versus 2.93% Yesterday

- Yield on 10-Year China Development Bank Bond 3.23% versus 3.23% Yesterday

- Copper Price +0.60% overnight