Stocks Lower In Advance of Earnings Season, Week in Review

3 Min. Read Time

Week in Review

- China released the October manufacturing and non-manufacturing PMIs on Monday, showing that the non-manufacturing sector expanded while the manufacturing sector contracted. The release highlighted the problems facing policymakers and companies globally: slower growth and higher input costs.

- Asian equities closed slightly lower overall on Tuesday as investors awaited clarity from the Fed on its tapering schedule.

- COP26, the UN-sponsored climate conference that kicked off this week, has been a performance catalyst for electric vehicles and renewable energy stocks in China this week.

- In regulatory news this week, the PBOC reminded fintech platforms to abide by the new consumer data protection laws and the State Administration for Market Administration (SAMR) released a classification system for internet platforms, which investors should cheer because it means that smaller players will be less impacted.

Key News

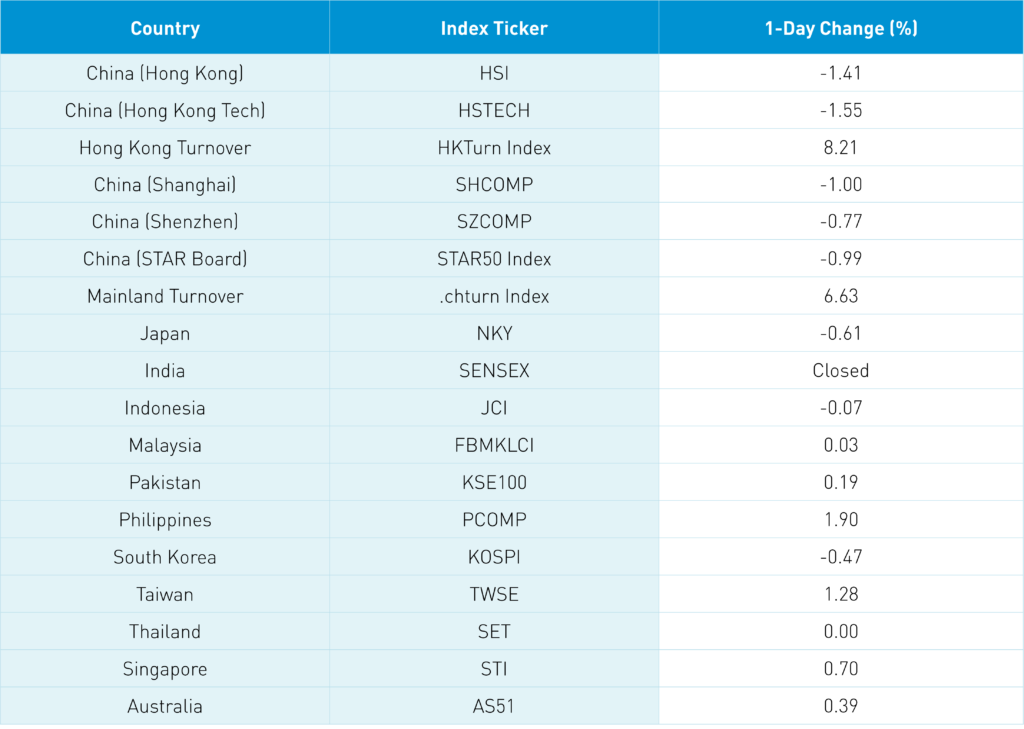

North Asia equity markets were off except for Taiwan, which managed a gain, while South Asia outperformed, and India took another day off.

Yesterday’s sell-off in US-listed Chinese ADRs was a head-scratcher as there was no catalyst for the selling especially after many of their Hong Kong listings had such a strong day. There are rumors that a $2 billion Hong Kong-based hedge fund focused on China might close following the exit of two senior partners after a rough September, but that would hardly explain the move. The ADRs all traded well below their average volumes, indicating that buyers are waiting for earnings season, which kicks off next week.

Tencent will report after the Hong Kong close next Wednesday. Alibaba and JD.com will report on November 18th. Online real estate company Beike and Tencent Music Entertainment kick things off on Monday. Overnight, an Asia-focused investment bank noted the divergent views of Chinese investors regarding the internet space versus foreign investors.

While Hong Kong internet stocks followed the US names down overnight, Mainland investors were net buyers of Tencent, which fell -2.79%, Alibaba HK, which fell -3.44%, and Meituan, which fell -3.22%. Hong Kong had a rough night as decliners outpaced advancers by 3 to 1 as the Hang Seng fell -1.41% on volume that was +8% from yesterday but still below the 1-year average.

Real estate was in the news (again) as real estate developer Kaisa reportedly missed a loan payment though it is selling 18 Shenzhen projects, which would raise approximately $13 billion. Kaisa’s bond due November 22nd, 2021 jumped $0.04 to $34.17 after hitting a 52 week low yesterday of $30.12. Evergrande ‘s April 2022 bond was off -$0.34 to $30.61. Evergrande’s June 2025 bonds +$0.41 to $25.86.

The Mainland market gave up early gains as a sell-off took place later in the day, leading to Shanghai falling -1%, Shenzhen falling -0.77%, and the STAR Board falling -0.99%. Investors pivoted to defensive/high-quality names as the clean technology ecosystem was hit with profit-taking. The PBOC took some liquidity out of the financial system after replacing maturing repos with a smaller amount of new repos. Energy stocks were hit hard as coal futures prices are now down -37% after their highs. Foreign investors were net sellers of Mainland stocks today to the tune of -$93 million as Longi Green Energy, which was also one of the Mainland’s most heavily traded, was down -2.7% after seeing significant selling following the confiscation of solar panels delivered to the US. For the week, foreign investors bought $689 million worth of Mainland stocks.

The opening of the China International Import Expo was a non-event. President Xi kicked off the event’s keynote speech, which focused on China’s 20th anniversary of joining the WTO while noting that China imports $2.5 trillion worth of goods and services annually. Monday’s start of the sixth plenary session of the 19th Communist Party of the China Central Committee also had a limited impact on market performance. There has been some anticipation that we could see supportive economic policies come out of the event, which concludes next Thursday. Another non-market moving event was the anticipation of the Biden-Xi virtual summit.

HKeX CEO Nicolas Aguzin’s speech at the Hong Kong Fintech Week included the statement that he believes stocks from China’s Mainland will increase from RMB 31 trillion ($5 billion) to RMB 100 trillion ($15.6B) by 2030. He appears to be using free-float market cap as an FYI. Is he talking his book since the HKeX is a critical link via the Connect trading programs? 100%. Could he be right? 100%.

There is a ton of buzz here in the US about metaverse stocks. Craig Mellow of Barron’s had an article out today noting that a similar phenomenon is taking place in China that includes a quote from yours truly. In China, they call metaverse “yuan cosmos,” which is seeing some speculative enthusiasm showing that investor behavior is not that different globally.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.40 versus 6.40 yesterday

- CNY/EUR 7.38 versus 7.38 yesterday

- Yield on 1-Day Government Bond 1.64% versus 1.69% yesterday

- Yield on 10-Year Government Bond 2.89% versus 2.93% yesterday

- Yield on 10-Year China Development Bank Bond 3.17% versus 3.21% yesterday

- Copper Price -1.10% overnight