Tencent Reports Q3, PPI (Oh My!), Loan Data Improves

3 Min. Read Time

Tencent Q3 Earnings

Tencent reported Q3 financial results after the Hong Kong close this morning. Tencent’s release was decent as macro headwinds crimped the quarter’s results. Minor gaming regulation reduced minors’ percentage of revenue from 6.4% in Q3 2020 to 0.7% though overall gaming revenue increased by 8%. Advertising revenue slowed due to the after-school tutoring regulation and the macro headwind, which the company stated could persist for several quarters.

The company said internet regulation is driven by the government’s desire to see healthy economic growth and protect user data. While internet regulation is apt to be a global phenomenon, they believe there will be further regulation in China, but less and less impactful as companies adapt and adhere to the new rules. My read is that the worst is behind us on the regulatory front. President Martin Lau threw cold water on the metaverse, saying that the hype does not match the economic reality though the company is well-positioned for adoption. Comparisons are year over year, i.e. compared to Q3 2020.

- Revenue grew 13% to RMB 142.358B versus estimates of RMB 145.413B

- Revenue breakdown: Value Added Services increased +8% from RMB 69.802B to RMB 75.204B

- Online Advertising increased +5% from RMB 21.351B to RMB 22.495B, FinTech increased +30% from RMB 33.255B to RMB 43.317B

- Cost of revenues +16% to RMB 79.6B from RMB 68.8B

- Operating Margin 37%

- Net Margin 28%

- Adjusted Net Income declined -2% to RMB 31.751B versus estimate of RMB 32.354B

- Adjusted EPS declined-2% to RMB 3.32 versus estimate of RMB 3.35

- Cash increased to RMB 170.873B from RMB 141.721B

- Q3 Stock Buyback was 5.581mm shares

- # of employees increased to 107k from 77k

Key News

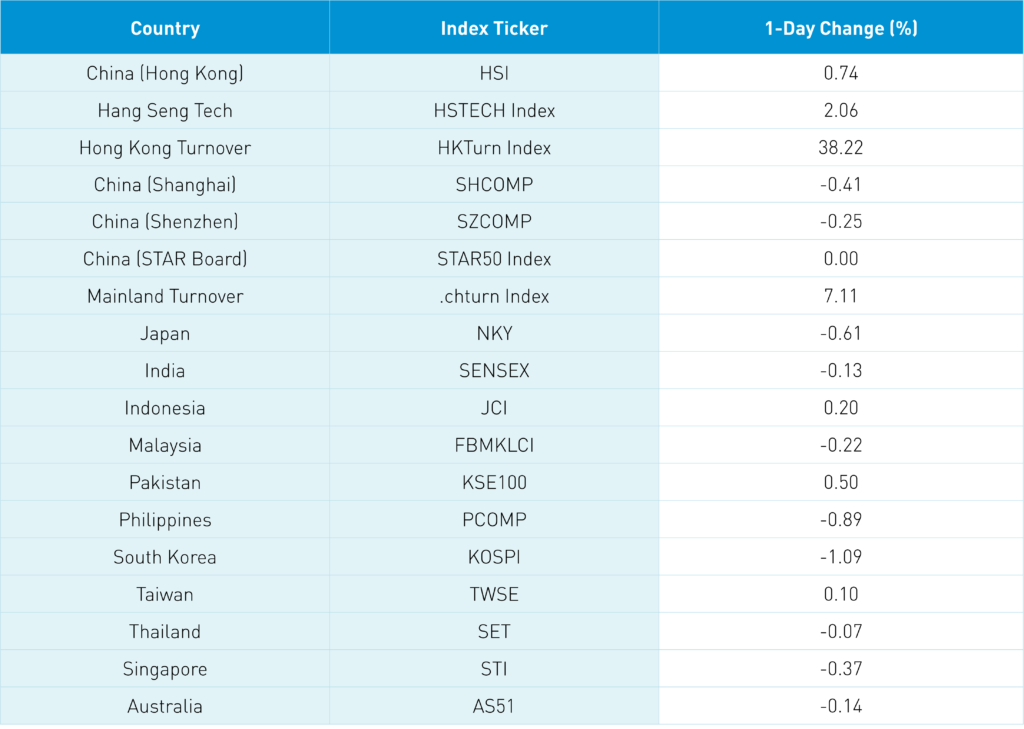

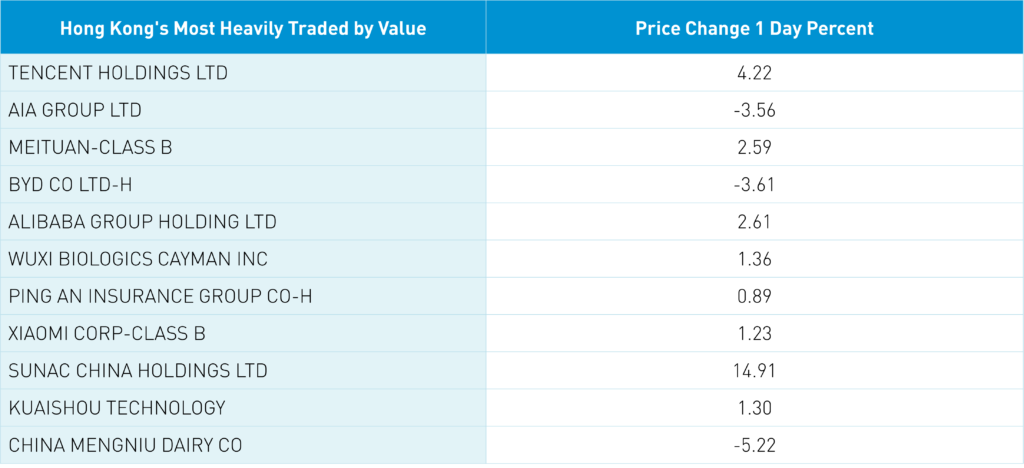

Asian equities were off overnight on light volumes as Hong Kong and Taiwan bucked the trend. The Hang Seng gained +0.7% as volume jumped +38% from yesterday though remains only 79% of the 1-year average. Internet stocks outperformed as the Hang Seng Tech Index gained +2.06% in advance of Tencent’s Q3 release after the market close in Hong Kong.

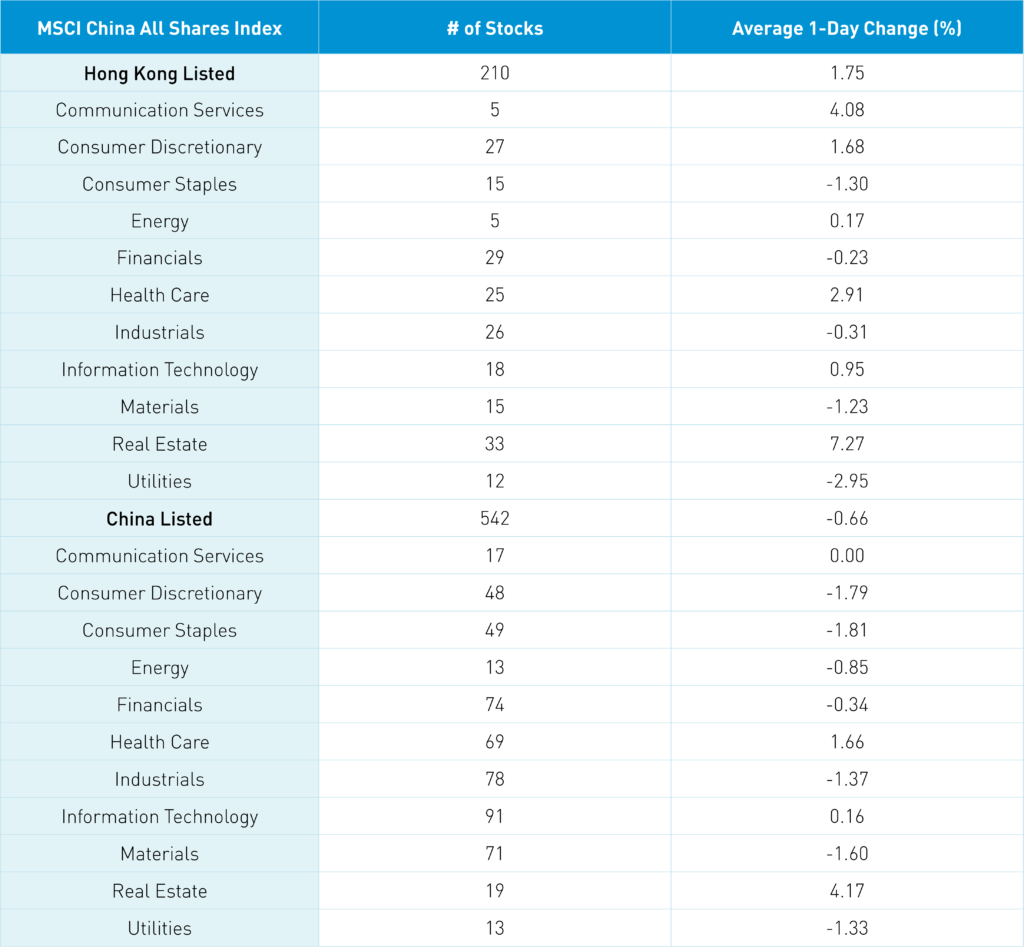

Real estate was the top-performing sector gaining +7.27% in Hong Kong and +4.17% in Mainland China on chatter that bond issuance policies could be loosened to support the industry. Evergrande’s 2022 and 2025 bonds were flat overnight. Healthcare also had a strong day in both markets.

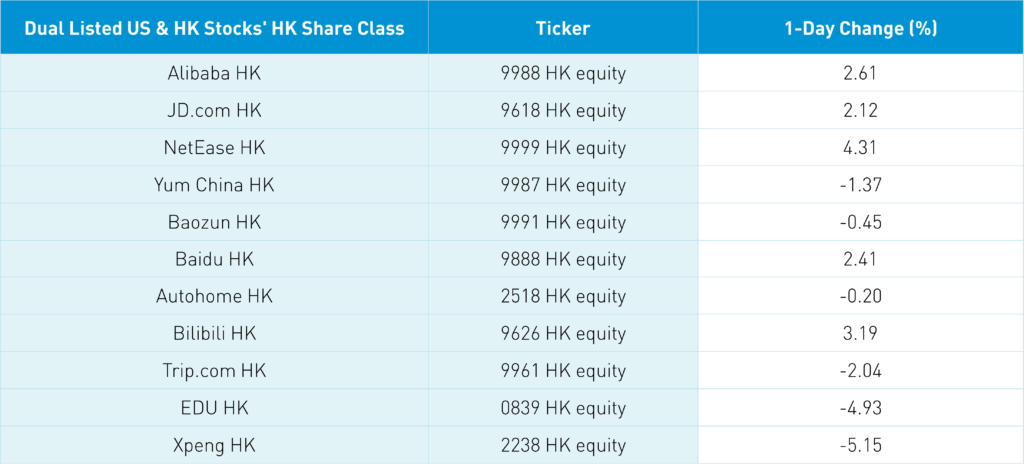

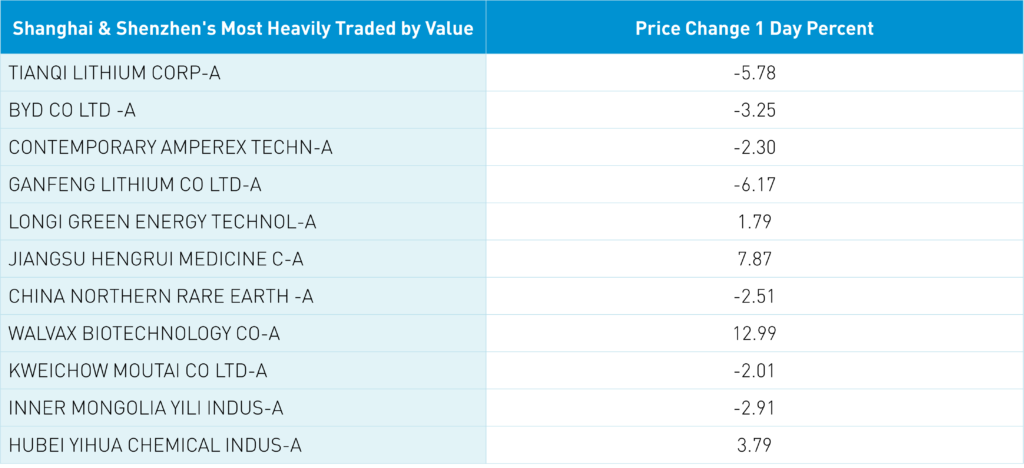

The clean technology ecosystem in Hong Kong and China was hit with profit-taking following Elon Musk’s proposed Tesla sale and Nio’s mixed Q3 financial results. The electric vehicle manufacturer's production outlook was a touch light due to the ongoing semiconductor shortage.

The Mainland market dipped following the release of China’s PPI and CPI data, though came off the lows as Shanghai fell -0.41%, Shenzhen fell-0.25%, and the STAR Board was flat.

October CPI was a non-event at 1.5% versus an estimated 1.4% and September’s 0.7% while PPI came in higher than anticipated at 13.5% versus an estimated 12.3% and September’s 10.7%. Higher commodity input prices are leading to higher output prices. High coal prices drove the mining segment up 66.5% year over year, though coal prices have been plunging and are down -42% from the October 19th high, as production ramps up in advance of the winter. I would guess that PPI has peaked.

After the Mainland market close at 3 pm, aggregate financing and new loans beat estimates, which helped Hong Kong rally into the close. The Mainland market closes at 3 pm versus Hong Kong at 4 pm. Chinese investors were net buyers of Hong Kong stocks as Tencent saw a slight net buy while Meituan saw a small net sale. Foreign investors were net sellers of Mainland stocks to the tune of $1.8 billion.

We have seen data showing that active managers, weighted by the size of the funds’ AUM, have a 10% underweight to China at 25% versus the MSCI Emerging Markets benchmark weight of 35%. That is a massive underweight! The culprit is how internet regulation was implemented as multiple regulatory bodies were implementing regulation on separate timetables, leading to the perception that it was being implemented in an ad hoc manner. Strong internet moves like today are a significant risk to these managers as their underweight can create underperformance, i.e. tracking error, which is what gets you fired. Ramping up exposure ahead of tomorrow’s Singles Day event makes sense to me. Today’s Mainland net sale could have been driven by managers that had been hiding in Mainland stocks dipping their toes in Hong Kong internet stocks. Hard to say for sure!

Last Night's Exchange Rates, Prices, & Yields

- CNY/USD 6.39 versus 6.39 yesterday

- CNY/EUR 7.37 versus 7.40 yesterday

- Yield on 1-Day Government Bond 1.70% versus 1.60% yesterday

- Yield on 10-Year Government Bond 2.91% versus 2.90% yesterday

- Yield on 10-Year China Development Bank Bond 3.18% versus 3.17% yesterday

- Copper Price -0.48% overnight