Omicron Concerns Muted in China, Economic Data Better Than Expected

2 Min. Read Time

Key News

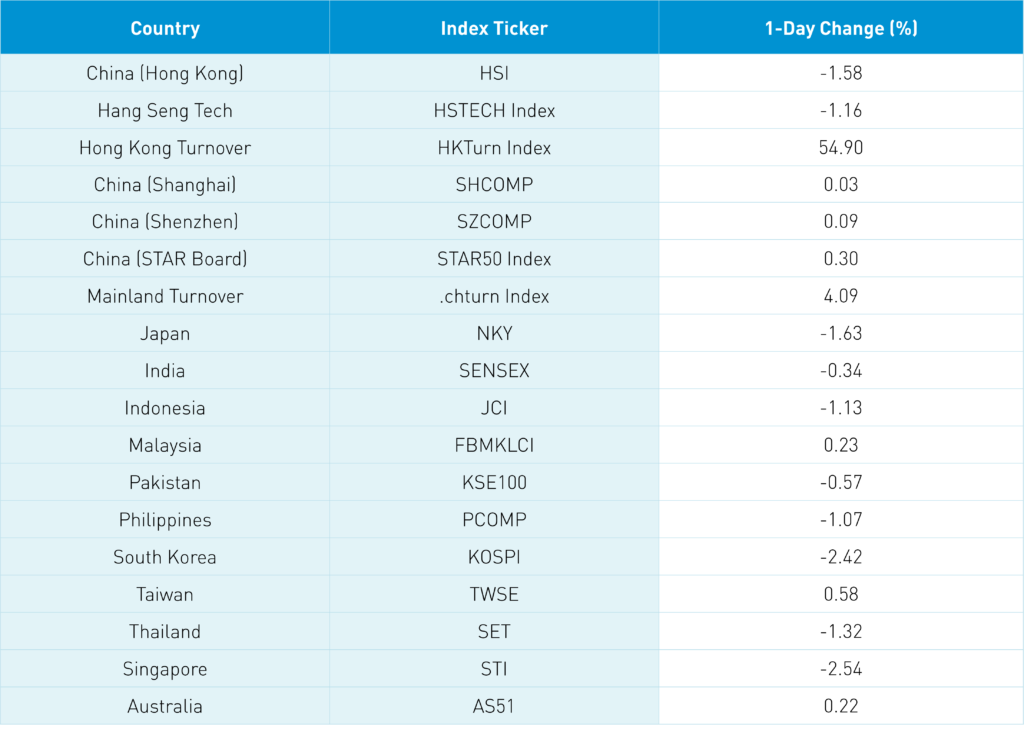

Asian markets were mixed overnight though Mainland China was flat as global markets reacted to news that existing vaccines and treatments may not work as well against the Omicron variant. Shanghai, Shenzhen, and the STAR Board closed +0.03%, +0.09%, and +0.30&, respectively. Meanwhile, the Hang Seng closed lower by -1.58% though the Hang Seng Tech Index held up better, falling by only -1.16%.

It appears another covid-fueled risk-off period could be upon us, though it is uncertain how long it will last. The CEO of Regeneron, the maker of one of the most popular covid treatments, stated that “there may be reduced neutralization activity of both vaccine-induced and monoclonal antibody conveyed immunity.”

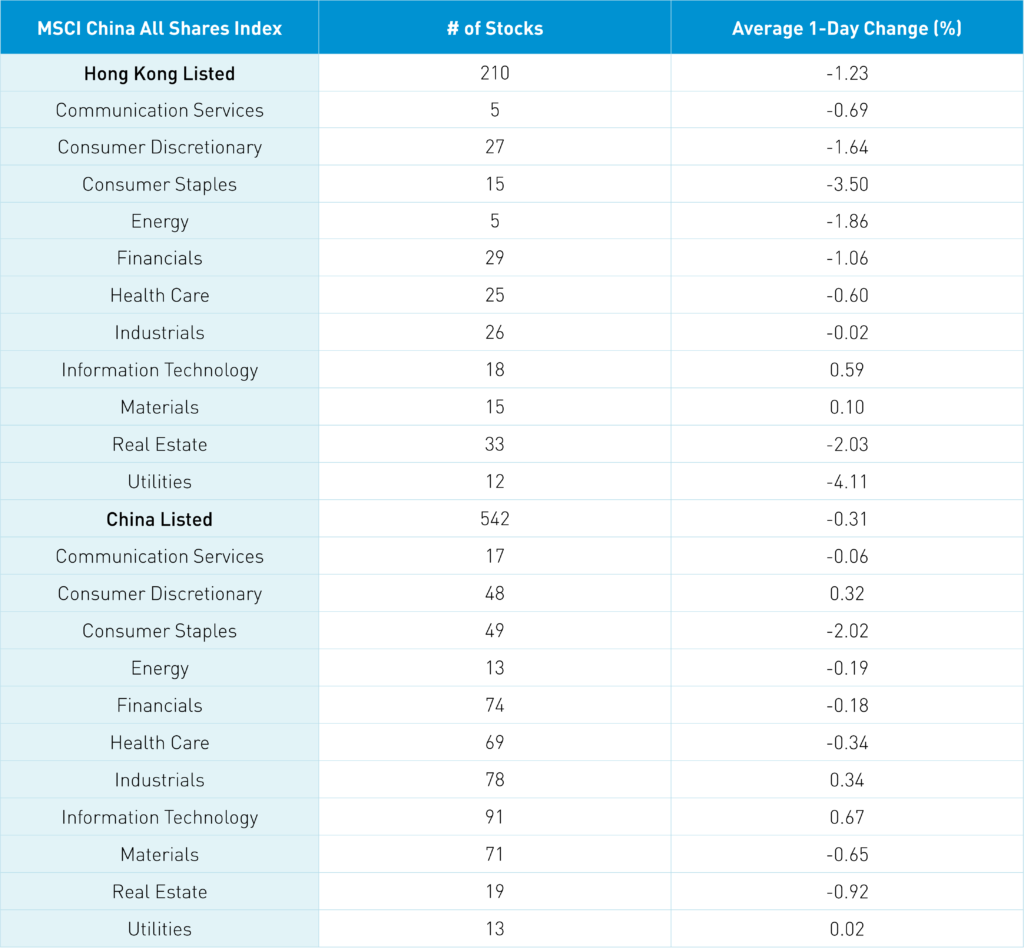

However, the risk-on environment may spare China to some extent because the country had not altogether stopped dealing with lockdowns, restrictions, and uncertainty. Thus, the sudden run-up in risk in China is less. Bloomberg reported on how China stocks have proven more resilient amid the growing Omicron concerns. Overnight, information technology was up on the Mainland as well as covid pill makers.

This December, China’s property developers will face nearly $1.3 billion in bond payments. Payments totaled $2 billion this past month with no defaults, which helped stabilize investors’ sentiment toward the sector. Investors’ focus will be on Evergrande and Kaisa Group, which have grace periods that will end in mid-December on $170.9 million worth in coupons. The reshuffling of Evergrande’s debts, among others, has been decidedly orderly, but these issuers and the sector are not out of the woods quite yet.

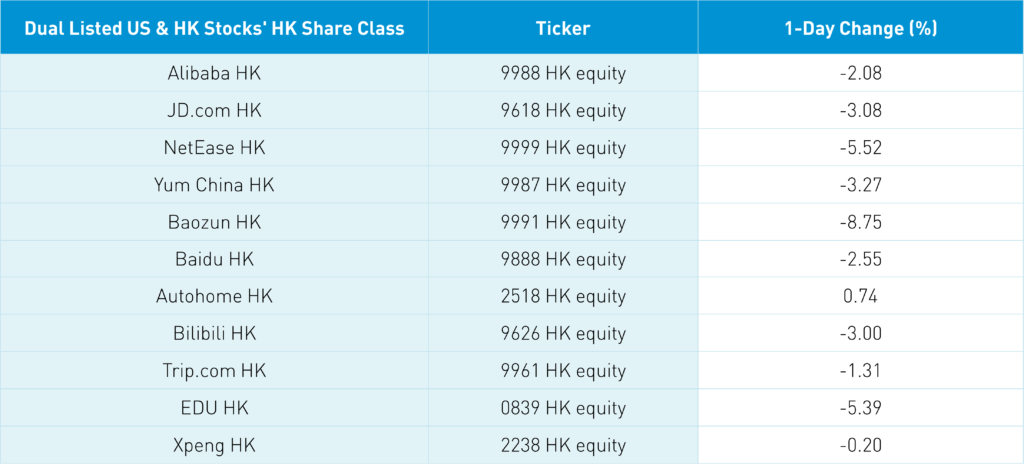

China internet stocks were under pressure, once again, in Hong Kong following lackluster earnings releases by Meituan and Pinduoduo. Yes, Meituan’s loss was significantly deeper than expected. However, Pinduoduo remains profitable as only the company’s top line was hurt. I think we are seeing more differentiation between China internet names, which should lead to a performance dispersion. Strangely, that has not happened yet as they have moved in lockstep with one another.

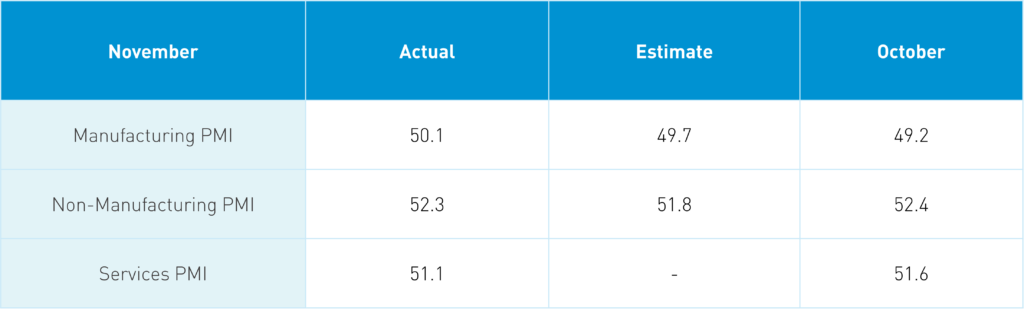

China released the November manufacturing, non-manufacturing, and services PMIs last night, all of which indicated an expansion in economic activity over the past month. However, non-manufacturing and manufacturing were lower than October’s reading. Manufacturing was particularly impressive as a contraction had been expected. PMIs are diffusion indexes, meaning that readings above 50 indicate expansion and readings below 50 indicate contraction.

Electric vehicle maker Li Auto reported that revenues surged +209.7% in the third quarter to RMB 7.78 billion. The company’s release follows what we heard from BYD, that China’s electric vehicle sales are due for another record year in 2021.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.39 versus 6.39 yesterday

- CNY/EUR 7.20 versus 7.23 yesterday

- Yield on 1-Day Government Bond 1.50% versus 1.50% yesterday

- Yield on 10-Year Government Bond 2.83% versus 2.82% yesterday

- Yield on 10-Year China Development Bank Bond 3.11% versus 3.10% yesterday

- Copper Price -0.20% today