CSRC Responds to Media’s Narrative, PBOC Cuts Bank RRR After Close

5 Min. Read Time

CSRC on Delisting, VIEs, and Regulation

Following Friday’s report that Didi might delist and the SEC outlining how they will enforce the Holding Foreign Companies Accountable Act (HFCAA), the China Securities Regulatory Commission (CSRC), China’s SEC, responded on Sunday. It is shocking how little attention this address has received. Didi proposed relisting in Hong Kong because the company is unable to comply with both Chinese law, which prevents audit papers from being given to the Public Company Accounting Oversight Board (PCAOB), and US law, which requires audit papers to be given to the PCAOB. It is important to remember that, under the current version of the HFCAA, a forced delisting of US-listed Chines companies would not occur until 2025, providing investors ample time to convert shares out of the US share class and into the Hong Kong share class. The Hong Kong Stock Exchange has waived its listing standards for companies with existing US listings, which should lead to many relistings in Hong Kong over the next year. Weibo is scheduled to relist in Hong Kong on Wednesday.

The CSRC release addressed several issues:

Variable Interest Entities (VIEs)

VIE, a legal structure that has been used for over twenty years, was specifically mentioned, nullifying the argument that VIEs are illegal in China. The VIE structure is used not only in the US but also in Hong Kong and Mainland China. News of VIE delisting is “misunderstanding and misinterpretation”.

Will Chinese regulators ban companies from listing outside of China?

The CSRC denied this news item, stating that “some domestic companies are currently communicating with domestic and foreign regulators to seek listing in the U.S. markets.”

Solving the long-running PCAOB audit review issue

CSRC “recently conducted candid and constructive communications with the US SEC and PCAOB…and has made positive progress on several important issues”. “…both sides have been cooperating on audit oversight of US-listed Chinese companies and worked together on pilot inspection programs…”. It had been reported that the US rejected China’s proposal that audit reviews redact user data and personal information. The workaround would be to tell the auditor not to include such data in their audit review.

Why is China implementing internet regulations?

Is China trying to kill its technology leaders? Since nearly 1/3 of all retail sales take place online, I have long been skeptical of this argument. The CSRC stated that recent regulations “…are aimed at limiting monopolistic practices, protecting SMEs, safeguarding the security of data and personal information, and preventing the disorderly expansion of capital.” Elements of China’s internet regulation resemble the General Data Protection Regulation (GDPR), which has been implemented in the European Union. While in Europe for work last week, I was surprised at how many US websites are not allowed in Europe for not complying with GDPR. I suppose this is Europe’s Great Firewall!

Where does this leave us?

There is time to solve the issue of US-listed Chinese companies’ inability to provide their audit papers to the PCAOB. The companies and their US and global shareholders are stuck between Chinese law and US law. Holding US and global investors’ savings hostage is disconcerting. It is worth noting that the US law came after the Chinese companies were allowed to list in the US. I firmly believe that Chinese companies should adhere to the PCAOB’s audit review standard. At the same time, threatening to vaporize the stocks makes little sense to me. If a solution cannot be found in the next two and half years, investors will convert out of the US names and into the Hong Kong shares.

Key News

The People’s Bank of China (PBOC), China’s central bank, cut banks’ reserve requirement ratio, the amount of deposits that banks need to hold on their balance sheet, after the market’s close by 50bps to 11.5%, effective December 15th. The move frees up RMB 1.2 trillion ($188 billion) for the banks to lend in support of small and medium-sized enterprises (SMEs), i.e. non-SOEs and the real estate sector. Investors will take the move as a signal the PBOC and policymakers are aware and ready to stimulate the economy.

Speaking of the real estate sector, Evergrande made headlines over the weekend after stating that it could not guarantee it could meet bond payments, which include $260 million owed to creditors. This led to a quick response from the PBOC, China’s insurance regulator, and the government of Guangdong province, where the company is located. The PBOC stated on Friday that “Evergrande Group’s risk primarily originates from its own unsound operations and blind expansion”. Ouch! With that said, both stated the real estate sector should be able to navigate Evergrande’s issues, though we are apt to see smaller players fail.

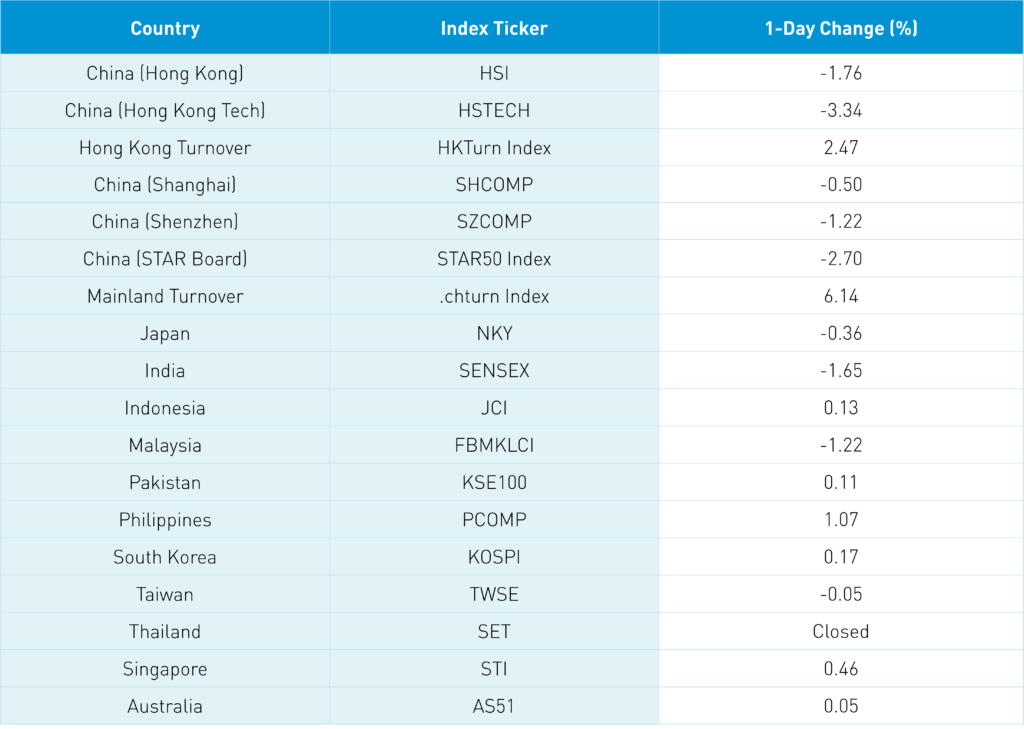

Asian equities had a rough night as growth stocks were hit especially hard as Hong Kong and India underperformed following the US’ market swoon on Friday. Hong Kong-listed internet stocks were off but were not down as much as they were on Friday in the US. For instance, Alibaba US was down -8.2% on Friday though Alibaba HK was down only -5.6% today.

Alibaba announced their CFO Maggie Wu will be replaced with Toby Xu as she will serve on the firm’s board. I always appreciated Ms. Wu’s candor and transparency on the company’s quarterly earnings calls, which I am sure Mr. Xu will continue. The company will also be separating its domestic Chinese E-Commerce and international E-Commerce units, which makes sense to me. The company is looking to become nimbler by providing unit heads more with more flexibility and control to respond to competition and unit-specific issues.

Japan’s Softbank had a rough night, falling -8.2% as its investments in Didi and Alibaba have been under pressure while overnight news that the FTC will block their sale of semiconductor company Arm to Nvidia added to its issues.

Mainland investors were net buyers of Tencent, which fell -3.2%, and Meituan, which fell -3.65% via Southbound Stock Connect.

Financials and real estate were areas of strength in Hong Kong and China as the market anticipated the bank RRR cut announced after the market’s close.

Healthcare names were very weak in Hong Kong after the latest round of bulk drug buying though today’s risk-off mood likely exacerbated the move.

Hong Kong Exchanges & Clearing was a rare up stock, gaining +1.15% as it would benefit from US delisting.

Growth names struggled across the region including in China as Shanghai fell -0.5%, Shenzhen fell -1.22%, and the STAR Board fell -2.7%. The clean technology ecosystem was broadly weaker across electric vehicles, solar, and wind on profit-taking. Rare earths were a standout as increased investment will occur in China. Foreign investors were small net buyers of Mainland stocks to the tune of $61 million. Chinese Treasury bonds rallied, CNY was off a touch, and copper rallied a little.

60 Minutes had a piece on China’s internet regulation last night. Of the false narratives repeated, my favorite was that Ant Group’s IPO was stopped to put Jack Ma in place. Per the CSRC’s November 4th, 2020 statement, Ant Group’s IPO was stopped because it was about to be regulated under new fintech laws that would have impacted the financial statements in the IPO prospectus had they been considered. If Ant had gone public and then the regulation came out, the stock would have cratered. Per the CSRC’s website, “The recent regulatory interview with Ant Group by relevant regulators and changes in the regulatory environment of fintech businesses may have a material impact on Ant Group’s business structure and profit mode, which constitutes material issues at the pre-listing stage. Sticking to the principles of protecting the legitimate rights of investors, ensuring comprehensive, transparent, and accurate information disclosure, and safeguarding the integrity of the market, the SSE decided to suspend the listing pursuant to relevant regulations for the registration-based IPO regime.”

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.38 versus 6.38 Friday

- CNY/EUR 7.20 versus 7.19 Friday

- Yield on 1-Day Government Bond 1.58% versus 1.58% Friday

- Yield on 10-Year Government Bond 2.82% versus 2.87% Friday

- Yield on 10-Year China Development Bank Bond 3.08% versus 3.12% Friday

- Copper Price +0.14% overnight