Top Economic Policy Meeting Concludes, Foreign Investors Buy China in Size, Week in Review

2 Min. Read Time

Week in Review

- Over the weekend, the China Securities Regulatory Commission (CSRC), the SEC of China, issued a statement affirming its support for the variable interest entity (VIE) structure and the ability of Chinese companies to list abroad following US media reports to the contrary. However, the regulatory body will need to approve overseas listings going forward.

- China internet stocks rebounded this week after last week’s steep declines. Alibaba’s Hong Kong-listed shares surged +12.24% on Tuesday.

- Electric vehicles (EVs) accounted for over 20% of all vehicle sales in China in November, according to data released by the China Passenger Car Association on Wednesday.

- The Renminbi (CNY), China’s currency, reached a three-year high versus the US dollar this week, prompting the People’s Bank of China (PBOC), China’s central bank, to raise banks’ foreign exchange deposit ratio to 9% from 7%.

Friday’s Key News

The Central Economic Work Conference, which was attended by all top government officials, concluded today in Beijing. Attendees published a statement after the market’s close last night, which was sooner than anticipated. The statement starts by acknowledging that China’s economy faces three pressures: demand contraction, supply shocks, and expected weakness. According to attendees, to counteract these pressures, macro policies should be stable and effective while implementing a new tax reduction and fee reduction policy and strengthening support for small to medium-sized enterprises (non-SOEs). Furthermore, the policymakers in attendance highlighted that financial institutions will be “guided” to support the economy. Areas of focus for policy will include supporting the clean technology industry and creating a three-year action plan for science and technology innovation. Policymakers also stressed that financial opening will continue. Another area of focus will be “implementing the new birth policy and actively responding to the aging population.” That will be interesting to see! Peak carbon was highlighted, and policymakers noted that there will be a “gradual exit of traditional energy” to “the safe and reliable replacement of new energy.” It was a long statement, but my take was positive as China will pursue proactive policies while focusing on quality economic growth versus the high, but often debt-fueled growth of the past.

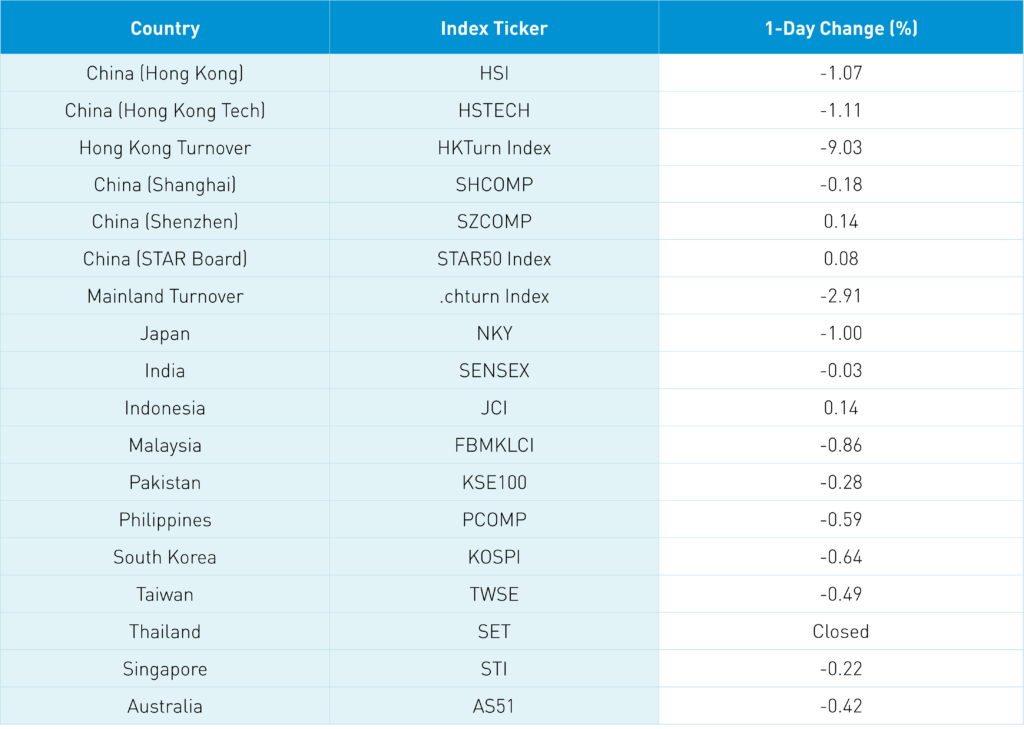

Asian equities followed the US’ equity drop yesterday ending a positive week with a thud. Omicron fears were mentioned but good old-fashioned profit-taking was likely the culprit. Having visited four European cities recently, I do not believe there is any appetite for further lockdowns.

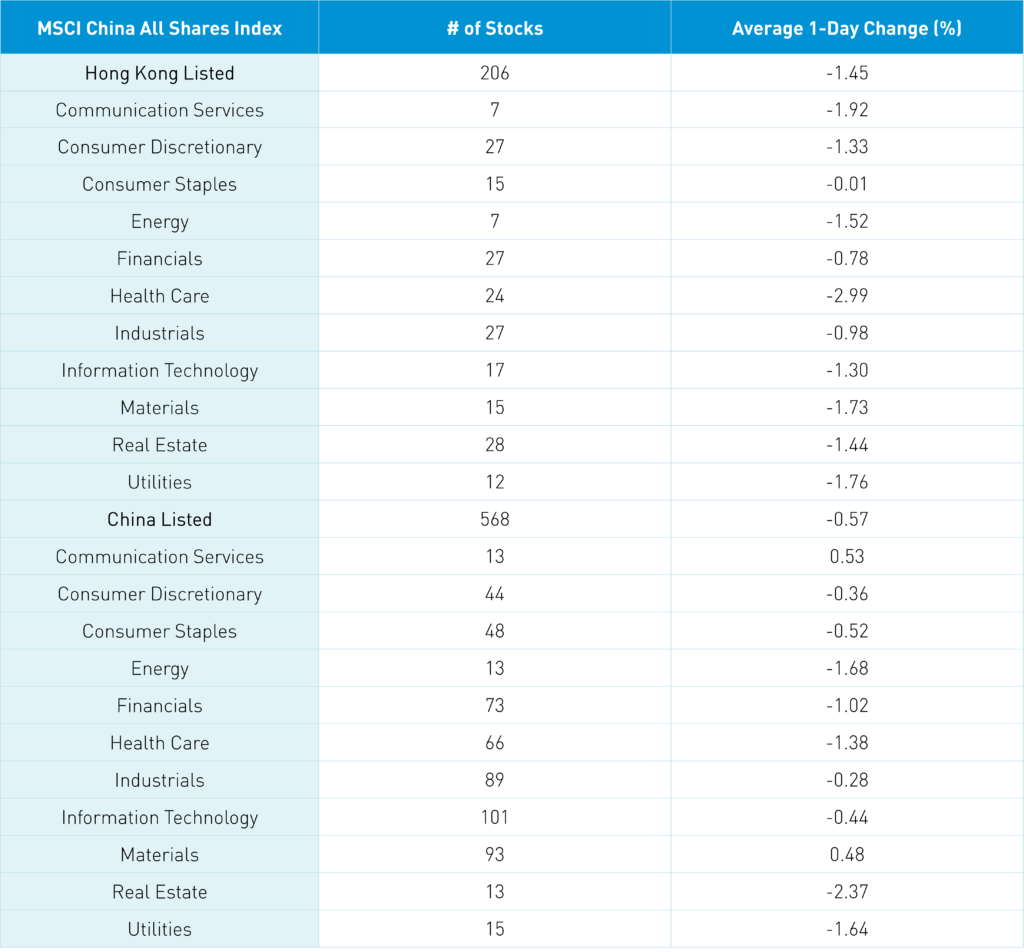

Hong Kong was off with as decliners outpaced advancers by nearly 4 to 1 on light volume that was only 60% of the 1-year average as all sectors were in the red, including internet stocks. However, JD.com’s Hong Kong listing bucked the trend, gaining +0.39% as the long JD and short Alibaba trade took a beating early in the weak. Alibaba shorts should be careful as the company hosts its investor day next Thursday and Friday. I anticipate a strong message from management.

Tencent and Meituan saw net buying (again) from mainland investors via Southbound Stock Connect with the latter seeing the strongest buy day in two months.

Mainland China was not nearly as pessimistic as broader Asia. Shanghai, Shenzhen, and the STAR Board were mostly flat, closing -0.18%, +0.14%, and +0.14%, respectively. Advancers and decliners were even on the Mainland though communication and materials were the only positive sectors, gaining +0.52% and +0.46%, respectively.

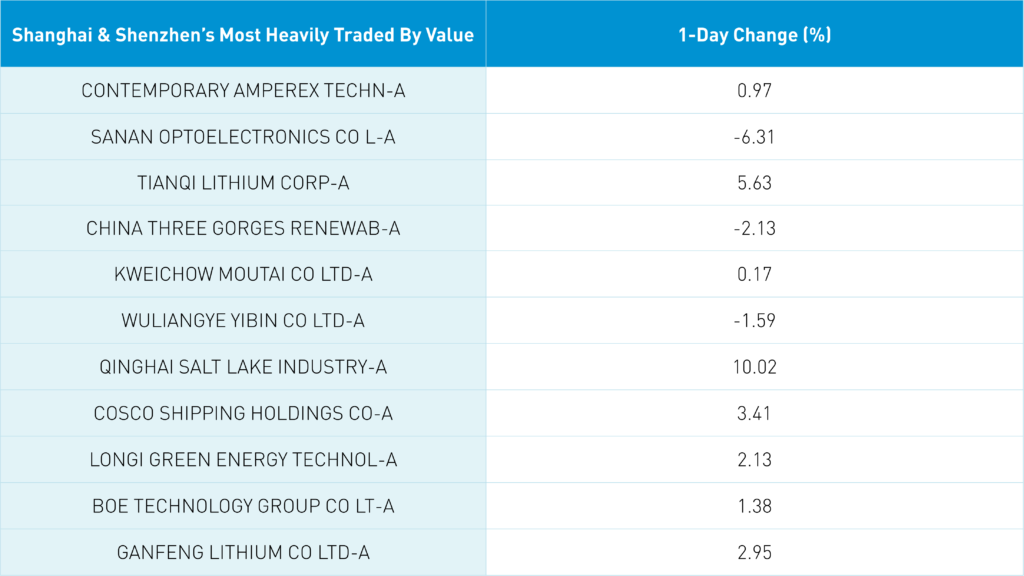

Clean technology was a bright spot on the Mainland overnight as the EV ecosystem, solar, and wind stocks had a strong day.

Foreign investors bought $1.4 billion worth of Mainland stocks today, bringing the weekly total to $7.7 billion. CNY was off a touch along with copper while bonds gained.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.37 versus 6.38 yesterday

- CNY/EUR 7.20 versus 7.20 yesterday

- Yield on 1-Day Government Bond 1.63% versus 1.65% yesterday

- Yield on 10-Year Government Bond 2.84% versus 2.85% yesterday

- Yield on 10-Year China Development Bank Bond 3.09% versus 3.09% yesterday

- Copper Price -0.42% overnight