Weibo Loses $729mm of Market Cap on a $471k Fine

2 Min. Read Time

Key News

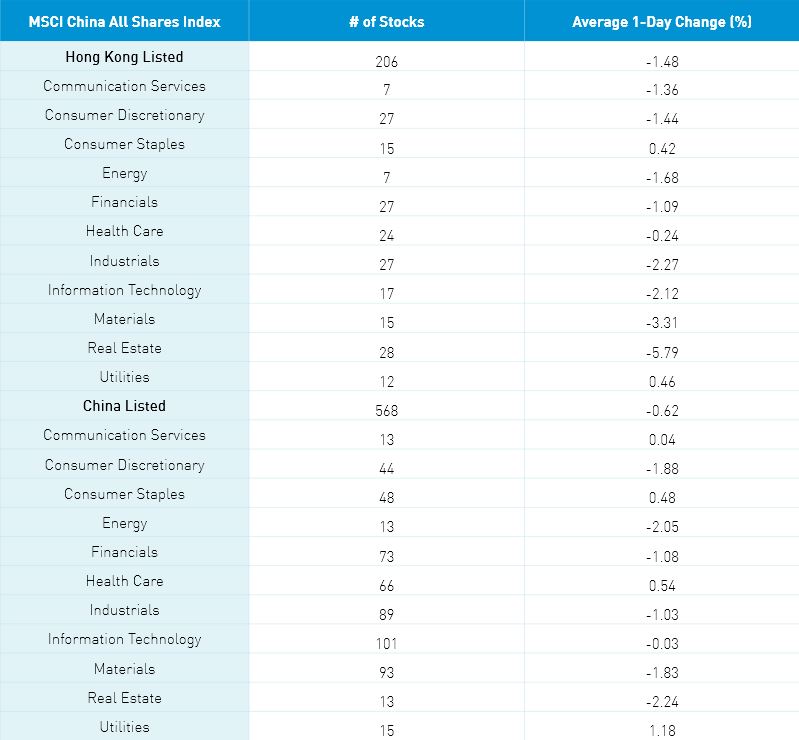

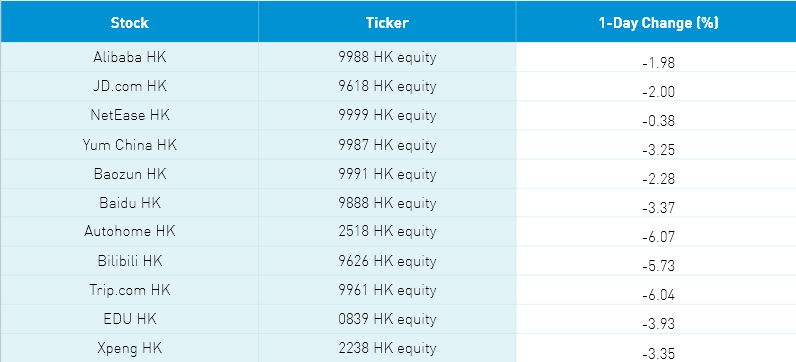

Asian equities were off overnight on light volumes as investors wait for tomorrow’s Fed tapering guidance while omicron fears weighed on sentiment. The Hang Seng was off -1.33% while the Hang Seng Tech -2.28% on volume -7.46% from yesterday which is just 71% of the 1-year average. US-listed Chinese internet stocks sold off yesterday following weakness in US equity markets as Hong Kong-listed internet stocks followed overnight. I believe tax loss harvesting is a factor in the weakness of US-listed Chinese ADRs though it is difficult to articulate the extent of the selling’s effect.

Weibo HK was off -9.62%, which is a loss of 729mm in market cap, after being fined a minuscule RMB 3mm ($471k) by the State Cyberspace Office. The market’s reaction considering the tiny size of the fine highlights the fragile state of the space.

Real estate in both Hong Kong and the Mainland was off nearly -6% after property developer Shimao (813 HK) fell -19.92% following a broker downgraded the stock. Interesting to note that the company’s bonds had been trading near par value though have fallen recently as the market’s shoot first ask questions mentality remains in the space. The sharp sell-off hit the offshore bond market as Evergrande’s May 2022 bond was off -$0.88 to $22.57 while the June 2025 bond were off -$0.61 to $20.04. After the close, Shimao reported that “Business as Usual, No concern on Debt Repayment Ability” according to Bloomberg.

After the Hong Kong close, Goldman Sachs upgraded Chinese equities due to their attractive valuations and the fact that they continue to be underinvested in. JP Morgan also upgraded offshore Chinese equities in anticipation of a strong 2022 performance.

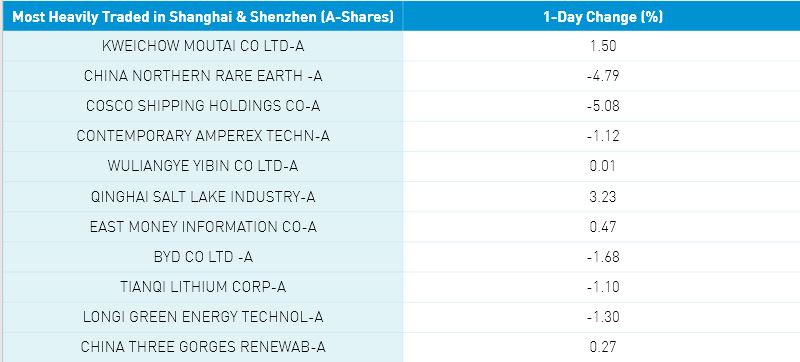

Shanghai, Shenzhen and STAR Board were off -0.53%, -0.14% and -0.43% on volume off nearly -10% from yesterday which is 110% of the 1-year average. Worth noting that the PBOC, Ministry of Finance, and CBIRC (insurance regulator) had statements speaking to the Central Economic Work Conference’s guideline on supporting the economy. The NDRC and MIIT had statements on supporting purchases of EVs and home appliances post CEWC. The market may have been off today but I don’t think for long!

Liquor stocks and the healthcare sector had a strong day while the clean technology ecosystem was mixed as China reported the first case of omicron in the Mainland. We had another strong day from foreign investors in the mainland as they purchased $946mm of Mainland stocks today. CNY appreciated versus the US $, Treasury bonds rallied, and copper was off a touch.

Suddenly there is a narrative that China isn’t investable. How quickly we forget 2020 when China was one of the best-performing markets globally! My weekend reading included a statistic I almost didn’t believe from institutional brokerage firm CLSA. Since 1989, MSCI Japan is down -26%. 1989!!!

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.36 versus 6.36 Yesterday

- CNY/EUR 7.20 versus 7.18 Yesterday

- Yield on 10-Year Government Bond 2.85% versus 2.86% Yesterday

- Yield on 10-Year China Development Bank Bond 3.09% versus 3.10% Yesterday

- Copper Price -0.73% overnight