Tencent Sets Sail to Some Sea Shares

2 Min. Read Time

Key News

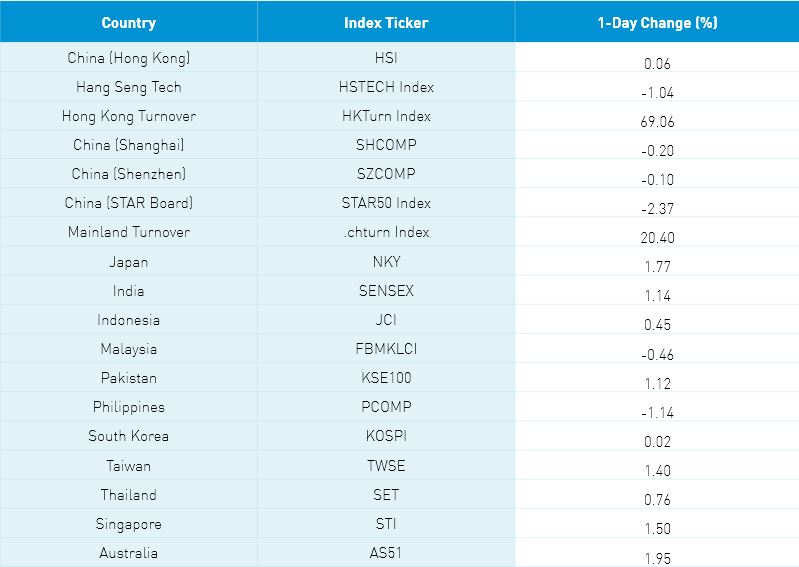

Asia equities were largely higher as Japan, Australia, Taiwan, and India outperformed. The Hang Seng bounced around the room, managing a +0.06% gain as volume increased +69.1% from yesterday, but was only at 71% of the 1-year average. It is interesting to note that regional volumes were light as investors trickle back from the holidays, which added to the volatility.

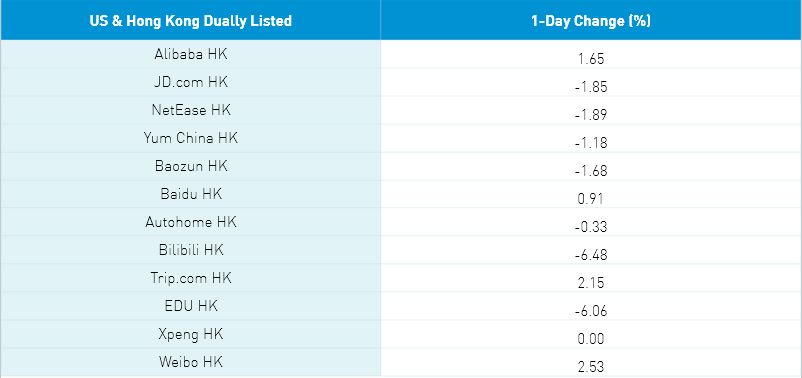

Tencent was off -0.84% though after the close it is being reported the company will sell 14.5 million shares, worth ~$3.1 billion, of Asian gaming and e-commerce company Sea. Tencent will still own 18.7% of Sea post-sale and agreed not to sell more shares for another six months. Another shareholder-friendly move from Tencent? Potentially, as the proceeds could fund buybacks or be distributed as cash. Clearly, the company wants to get its stock going after announcing that it would be spinning off its JD.com position to shareholders later this year.

Alibaba is rumored to be selling its Weibo stake. Hong Kong internet stocks were essentially off except for Alibaba HK, which gained +1.65%, on “news” that overseas listing of companies with more than 1 million users will require a cybersecurity review. I use air quotes because this was first announced back in July and reiterated several weeks ago.

Western media headlines are screaming about Evergrande having to tear down some buildings though its Hong Kong stock reopened for trading and gained +1.26%. However, US dollar bondholders were not so lucky as Evergrande’s April 2022 and June 2025 bonds hit 52-week lows.

The Caixin Manufacturing PMI reading for December was 50.9 versus expectations of 50 and November’s 49.9. Efforts to rein in high commodity prices effect on inflation appear to be working as Dr. Wang Zhe of Caixin Insight Group noted “Inflationary pressure eased as costs rose at a slower clip….Prices of some raw materials such as steel dropped considerably as government measures to ensure supply and stabilize prices took effect. Output prices dropped for the first time since April 2020…”. Maybe inflation is transitory!

Employment was off, which will certainly garner the attention of policymakers as job #1 is stability while job #2 is employment. There was some media and broker coverage that the PBOC drained liquidity from the financial system though this is only after ramping up liquidity into year-end. Coronavirus outbreaks across a few Chinese cities weighed on sentiment as China’s Lunar New Year travel will likely be highly curtailed this year.

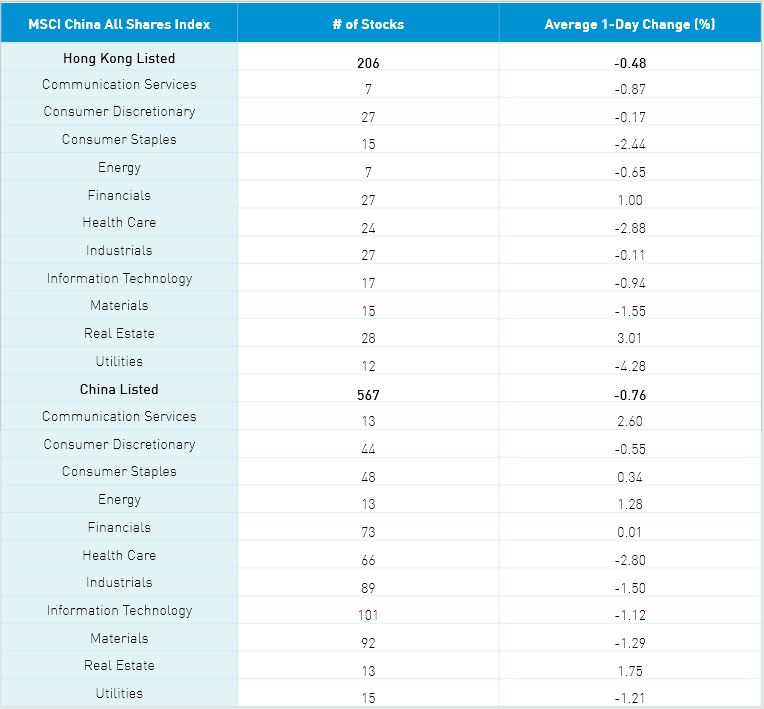

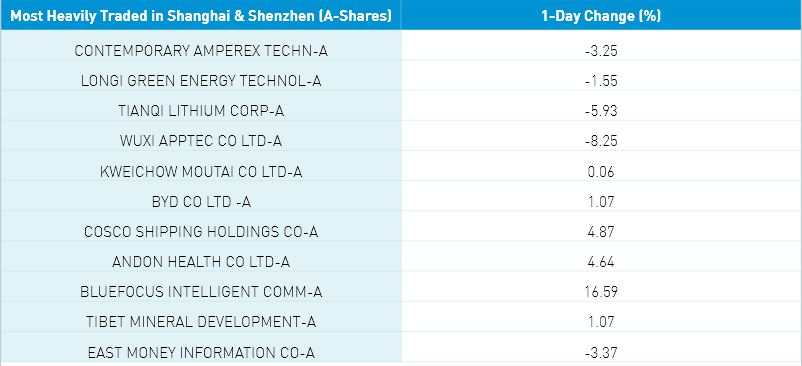

Several brokers highlighted higher US interest rates as a catalyst for the US dollar to rise but also a potential headwind for global equities. Hong Kong and China’s value sector/stock outperformed as healthcare was off as Chinese traditional medicine outperformed at the expense of biotech and equipment makers. The clean technology sector was off with electric vehicles, lithium, solar, and wind stocks underperforming as subsidies are being curtailed by 30% and will be completely pulled by year-end.

Shanghai eased -0.2%, Shenzhen fell -0.1%, and the STAR Board fell -2.37% as large caps outperformed small caps and value outperformed growth. Volumes were up +20% from the last trading day of 2021, which was just above the 1-year average. Foreign investors bought $72 million worth of Mainland stocks on moderate volumes via Northbound Stock Connect. CNY depreciated -0.32% versus the US dollar as the currency eased to 6.38 CNY/USD. Bonds were flat while copper was off a touch.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.38 versus 6.35 yesterday

- CNY/EUR 7.19 versus 7.19 yesterday

- Yield on 10-Year Government Bond 2.79% versus 2.78% yesterday

- Yield on 10-Year China Development Bank Bond 3.08% versus 3.08% yesterday

- Copper Price -0.46%