Powell’s Dovish Comments Let Markets Fly

2 Min. Read Time

Key News

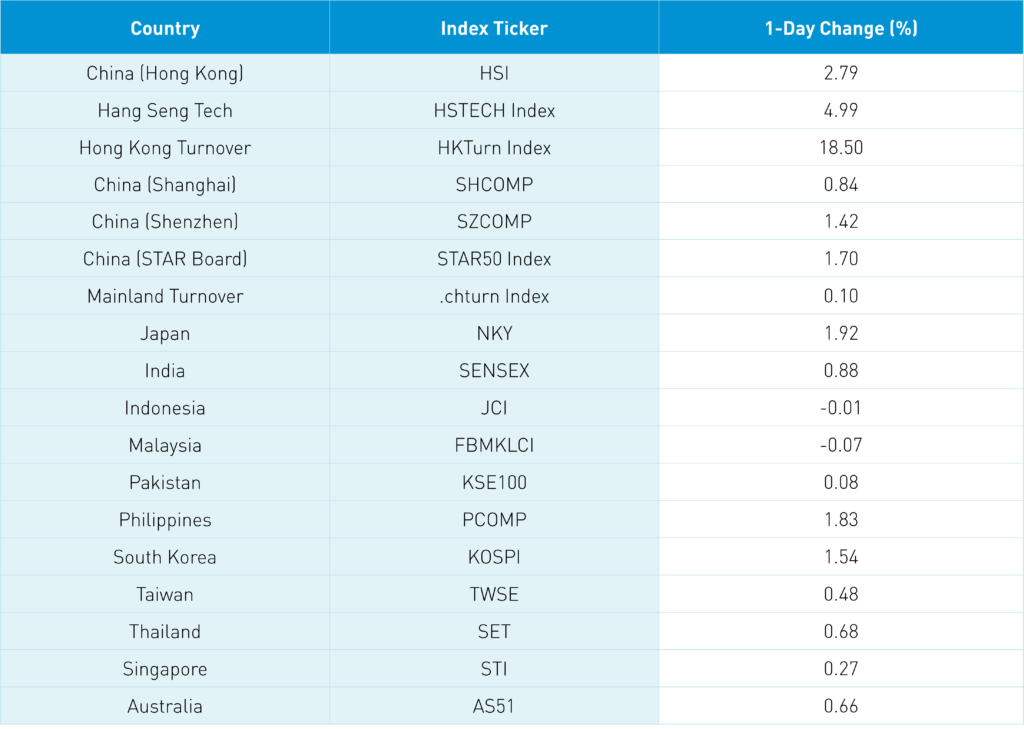

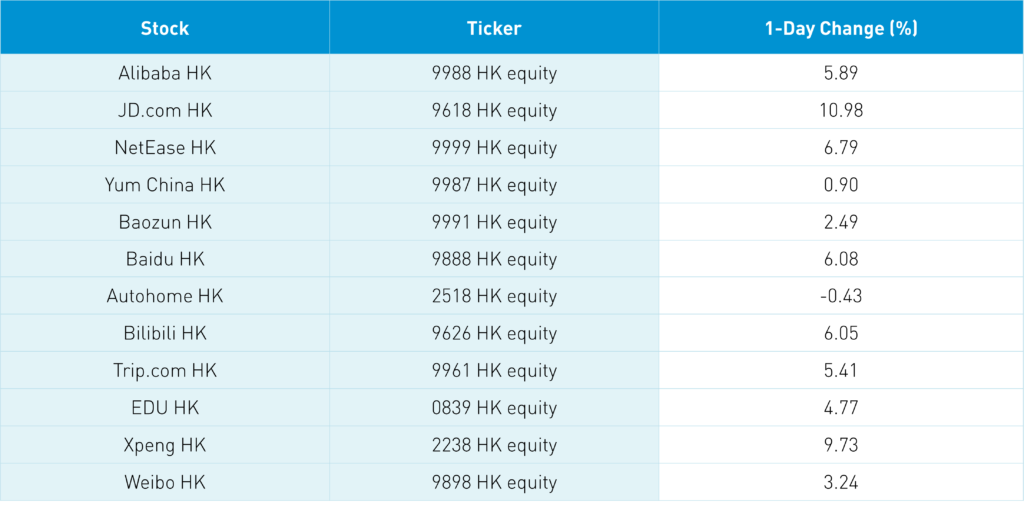

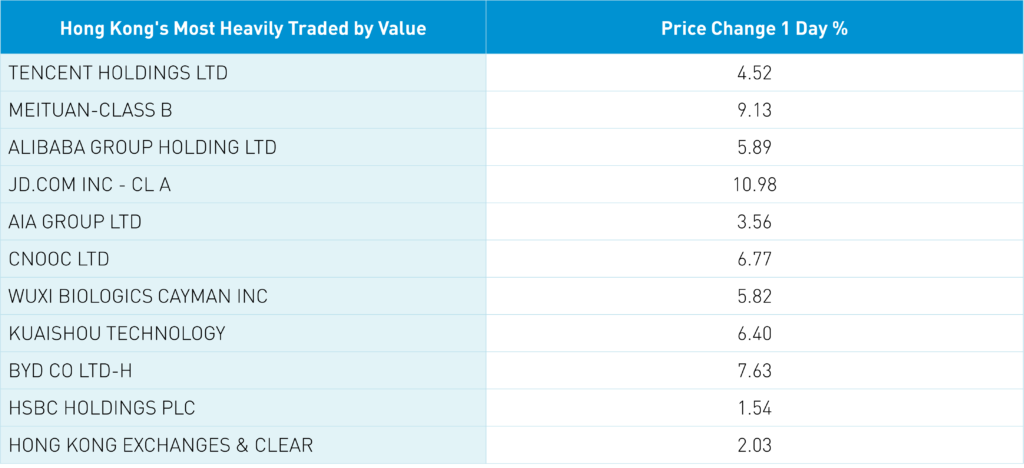

Asian equities had a strong day as Japan, China, Hong Kong, Taiwan, and South Korea posted impressive returns following US Fed Chairman Powell’s dovish comments, which raised investors’ risk appetite, especially toward growth stocks. The Hang Seng Index gained +2.79% led by internet stocks, which followed through on yesterday’s US rally. Hong Kong’s volume increased +18.51% from yesterday, which is 93% of the 1-year average while 2 stocks advanced for every 1 declining stock. The four most heavily traded stocks in Hong Kong by value were Tencent, which gained +4.52%, Meituan, which gained +9.13%, Alibaba HK, which gained +5.89%, and JD.com HK, which gained +10.98%. Muy Bueno!

Despite today’s Wall Street Journal headline that “For Chinese Tech Stocks, No News Is Good News” there were several catalysts for yesterday’s US move and today’s follow-through. As we mentioned yesterday, Fidelity held an investor symposium highlighting the attractiveness of China internet. Meanwhile, UBS’ internet analysts recommended the space following similar moves last week from Goldman Sachs and as JD.com announced entering the European market via an employeeless store in the Netherlands. We’ll have to get our colleague and main man in Amsterdam Sjef to check it out. We also had last week’s report that Charlie Munger doubled his Alibaba stake in Q4 after doubling in Q3. No catalysts – bah humbug! As we’ve mentioned numerous times, a rally in the space will “force” big fund families to correct their underweight to the names. Both Tencent and Meituan saw outsized purchases from Mainland investors via Southbound Stock Connect. Remember that Hong Kong has a significant structured product market, which tends to exacerbate moves to the upside and downside.

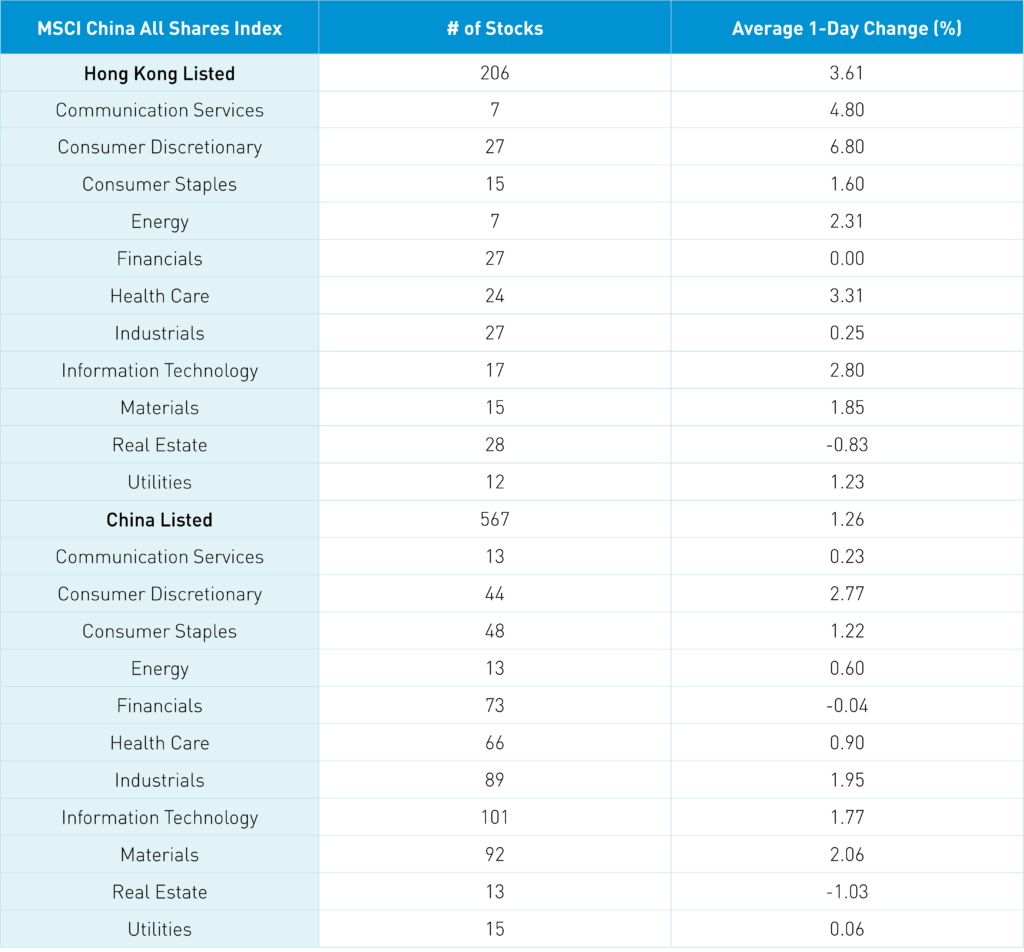

Growth stocks/sectors outpaced value stocks/sectors in both Hong Kong and China. The growth-oriented Shenzhen gained +1.42% and the hyper-growth STAR Board gained +1.7%, outpacing the growth/value balanced Shanghai’s +0.8% gain on volume that was flat from yesterday, which is barely over the 1-year average while advancing stocks outpaced declining stocks by 3 to 1.

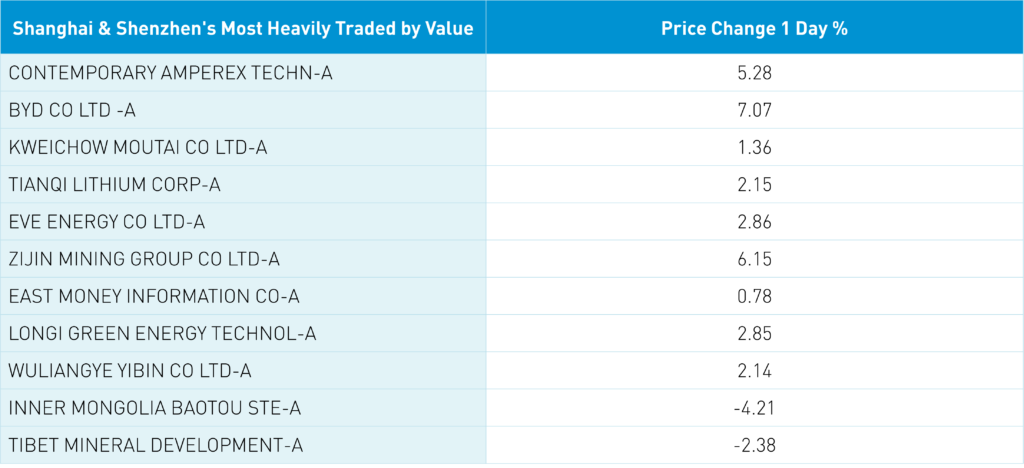

Catalysts for the Mainland rally included the announcement that China’s 2021 car sales increased +4.4% from 2020 to 20.1 million cars sold, according to Yicai Global and the China Association of Automobile Manufacturers (CAAM). Sales of internal combustion engine (ICE) cars (gas guzzlers) declined -6% from 2020 to 17.2 million while electric vehicle (EV) sales increased +250% to 3 million. 2021’s forecast for EV sales is 5 million though my colleague Anthony believes this figure is low based on his conversations with companies. The reports lit a fire under the clean technology sector as EV battery maker CATL was China’s most heavily traded stock by value, gaining +5.28%, followed by EV bus maker BYD, which gained +7.07%. Tianqi Lithium was the 4th highest volume traded and gained +2.15%.

December PPI year-over-year was 10.3% versus expectations of 11.3% and November’s 12.9% while the December CPI was 1.5% versus expectations of 1.7% and November’s 2.3%. Efforts to rein in inflation, especially in commodity prices, appear to slowly be taking effect. After the Mainland close, December aggregate financing was RMB 2.37 trillion versus expectations of 2.4 trillion and November’s 2.61 trillion, new loans came in at 1.13 trillion versus expectations of 1.25 trillion and November’s 1.27 trillion while M2 gained +9%. The loan data was a touch light though it is apt to spur policymakers to step on the support gas pedal especially with the Olympics around the corner. In the short run, we should see the PBOC provide ample liquidity going into Chinese New Year’s.

Foreign investors bought $1.103B of Mainland stocks via the Northbound Stock Connect with a focus on growth versus value. Chinese Treasury bonds were flat, CNY appreciated slightly versus the US $ and copper rallied.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.37 versus 6.37 Yesterday

- CNY/EUR 7.23 versus 7.22 Yesterday

- Yield on 10-Year Government Bond 2.80% versus 2.80% Yesterday

- Yield on 10-Year China Development Bank Bond 3.08% versus 3.08% Yesterday

- Copper Price +1.38% overnight