China’s Trade Balance Improves in December, Week In Review

3 Min. Read Time

Week In Review

- Health care gained Monday as China continues to battle covid-19 outbreaks with the city of Xian locked down, leading to increased demand for testing and vaccines.

- The growth to value rotation landed in Asia on Tuesday as the Shanghai Composite fell -1.06% and value stocks outperformed throughout the region.

- US Fed Chairman Powell’s dovish comments on Tuesday led to a rally in Asian equities n Wednesday as investors’ risk appetite was heightened globally following a risk off start to the week.

- Thursday’s market downturn left investors pondering what the PBOC’s calendar for stimulus could be. We know there will be easing this year, just not when or in what form.

Friday’s Key News

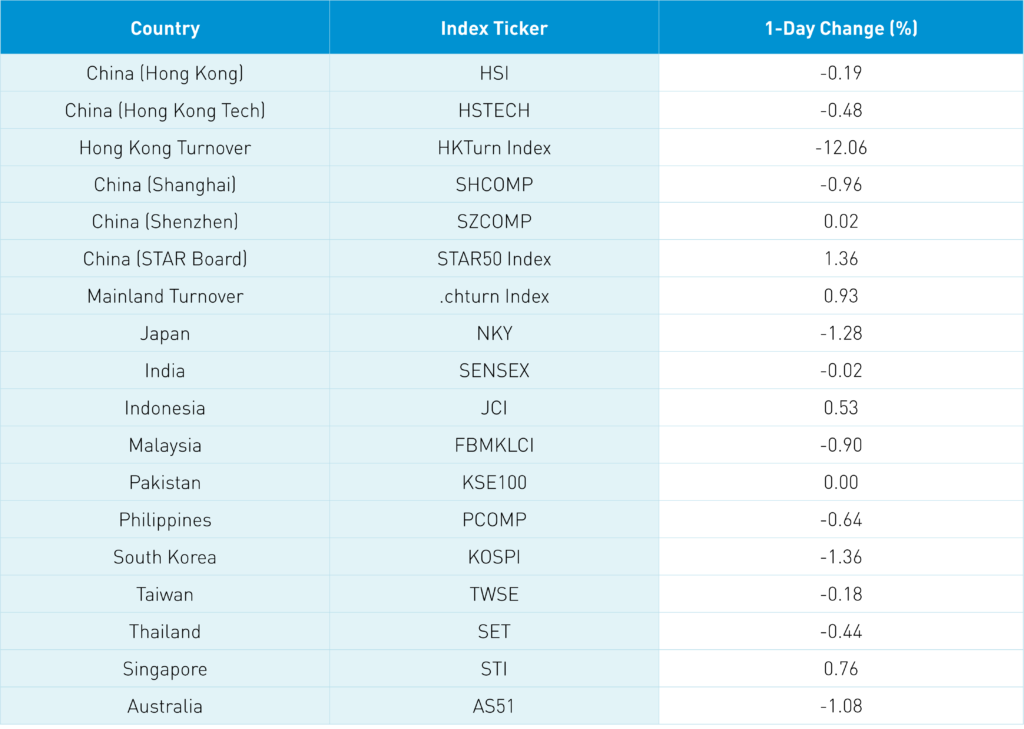

Asian equities were lower overnight as Japan, South Korea, and Australia were all off more than -1%.

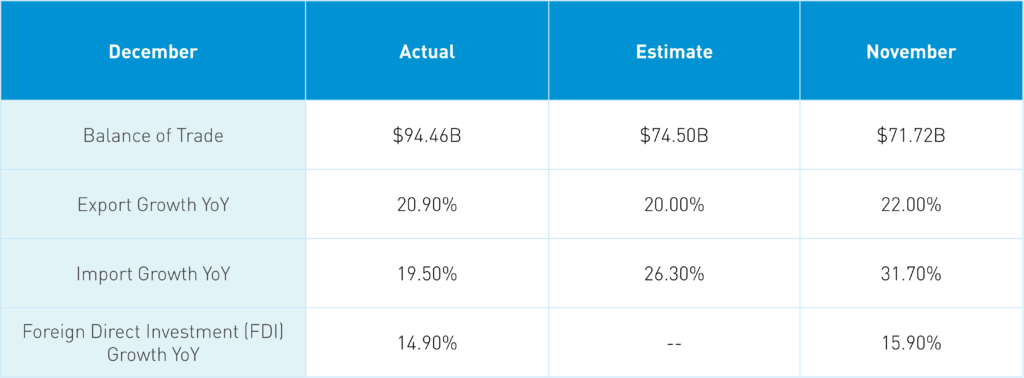

China’s December trade data was strong, beating expectations handily. The data proves how well businesspeople are getting along globally compared to politicians. However, the General Administration of Customs was cautious in its 2022 outlook, stating that domestic consumption needs to take the baton from export-driven manufacturing in 2022 as global government stimulus is eased. The release was not a market-moving event as market sentiment felt the weight of continued coronavirus outbreaks in China.

Numerically, China’s case numbers are low but seeing the virus cropping up in multiple cities, including Shanghai, is weighing on sentiment as investors recognize the response can be significant lockdowns, as are currently being seen in Xian.

Q4 and 2021 GDP data will be released on Sunday along with Industrial Production, Retail Sales, and Fixed Asset Investment (FAI).

The Hang Seng Index was off -0.19% after rallying into the close to mitigate losses on volume that was -12% lower than yesterday, which is 73% of the 1-year average. Hong Kong-listed internet stocks were off but not nearly as much as yesterday’s sell-off in the US, which has led to a rebound in US trading today. Alibaba HK was off -2.19%, which was well above the intra-day low of -4.24% on reports that asset manager China Cinda will not increase its stake in Ant Financial. Tencent fell -0.38% and Meituan fell -2.48% though both had small net buys coming from Mainland investors via Southbound Stock Connect.

There was some chatter and a Bloomberg article on how the US ADRs seem to do worse than their Hong Kong-listed peers intra-day. However, the names tend to play catch up with one another, so this is not exactly true, but we have spoken about how meaningless media stories tend to weigh heavily on the US shares. Despite how embarrassing a delisting might be, perhaps these companies belong in Asia for this reason.

Hong Kong-domiciled companies such as AIA, which gained +2.18%, HSBC, which gained +1.68%, and Macau gaming stocks had a good day though these names are not considered Chinese stocks as they are part of MSCI Hong Kong, which is within MSCI’s developed market index suite, and not MSCI China, which is in MSCI’s emerging market index suite. This makes very little sense to me.

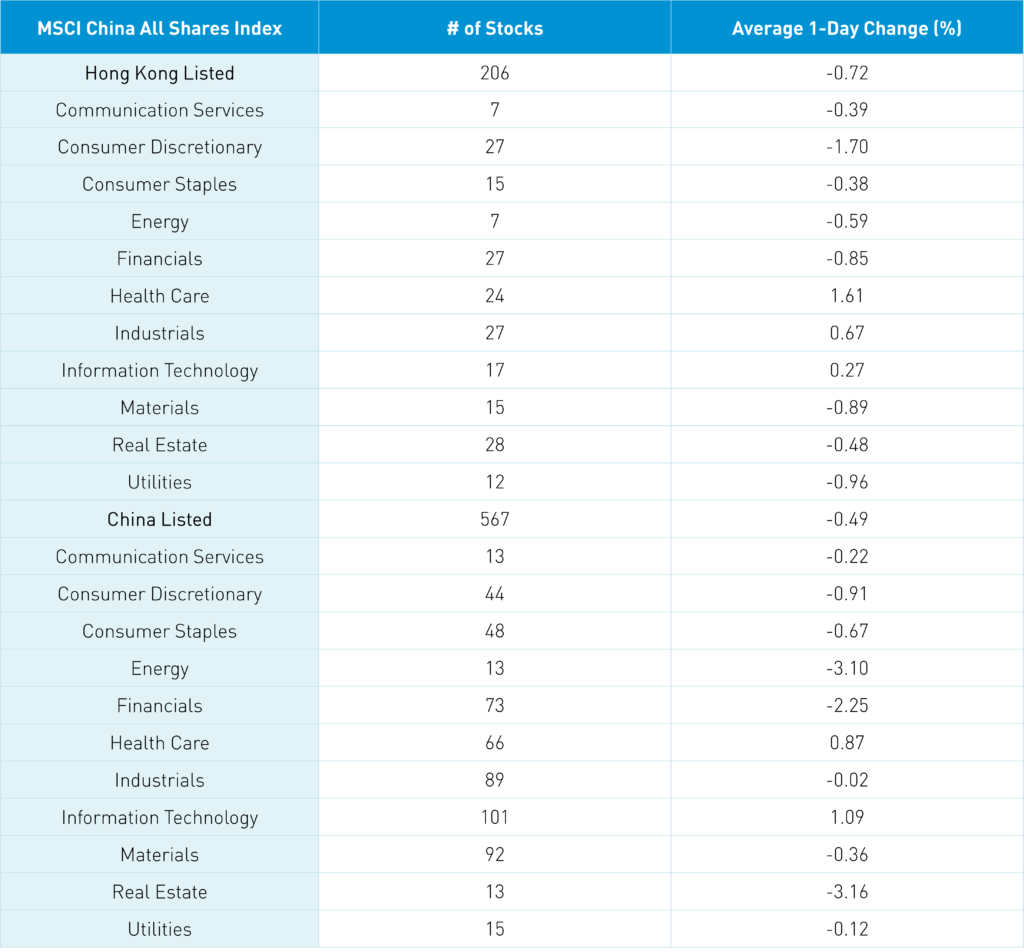

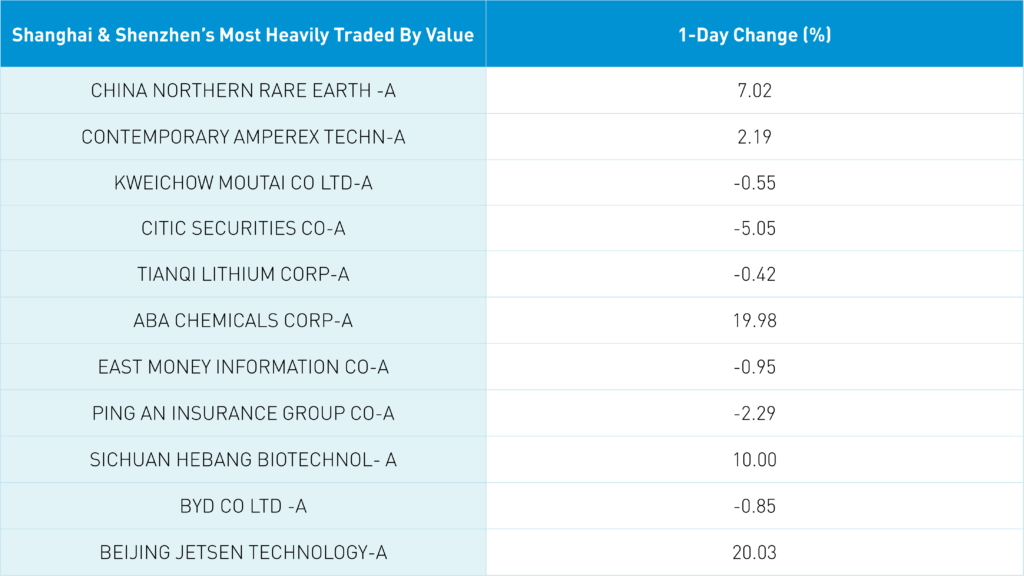

Mainland China saw an interesting divergence as Shanghai fell -0.96%, Shenzhen gained +0.02%, and the STAR Board gained +1.36% on volume that was up +0.93% from yesterday, which is 104% of the 1-year average while decliners outpaced advancing stocks by 2 to 1. The only positive sectors were technology, which gained +1.09%, and healthcare, which gained +0.86%. CATL rebounded +2.19% along with semiconductors, broader tech sub-sectors, and elements of the cleantech ecosystem such as lithium and rare earths.

Financials, energy, and real estate were off -2.26%, -3.11%, and -3.16%, respectively, on the Mainland. Foreign investors bought $44 million worth of Mainland stocks today via Northbound Stock Connect which brings the weekly total to $1.17 billion of net inflow. Chinese Treasury bonds were mostly flat, China’s currency appreciated to 6.35, and copper eased -0.63%.

Michael Shuman’s Superpower Interrupted provides a comprehensive account of China’s history starting more than 2,000 years ago. It is a good read for those curious about China’s history as it speaks to how Asia’s civilization, like what occurred in the Middle East, Africa, and the Americas, grew for thousands of years without contact with Europe other than some trading via the Silk Road. By the time Marco Polo got to China in the 1200s, China had been unified for over one thousand years. The point is that Europe and subsequently America were brought up on Greek, Roman, and European history, religion, and values, which were simply different than those in India, China, Japan, and Asia’s upbringing. European countries, and to a lesser degree the US, forced themselves and their culture on China during the Opium Wars, similar to the colonialism that took place in India, Africa, and Latin America. I do not want to give too much away. The book spends a great deal of time on the various dynasties while the critical element to understanding how Macau, Hong Kong, and Taiwan were taken by foreign powers (Portugal, Britain, and Japan) are the Opium Wars. There is very little examination of the US’ participation in this period though it continues to play role in politics today.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.35 versus 6.36 yesterday

- CNY/EUR 7.27 versus 7.29 yesterday

- Yield on 1-Day Government Bond 1.87% versus 1.90% yesterday

- Yield on 10-Year Government Bond 2.79% versus 2.79% yesterday

- Yield on 10-Year China Development Bank Bond 3.08% versus 3.08% yesterday

- Copper Price -0.63% overnight