Monetary Easing Gains Momentum, Hong Kong Internet Holds Up

2 Min. Read Time

Key News

Asian equities were a sea of red, except for the small gains by Hong Kong and Singapore. Japan was off -2% as Sony was smoked -12.79% post-Microsoft/Activision announcement.

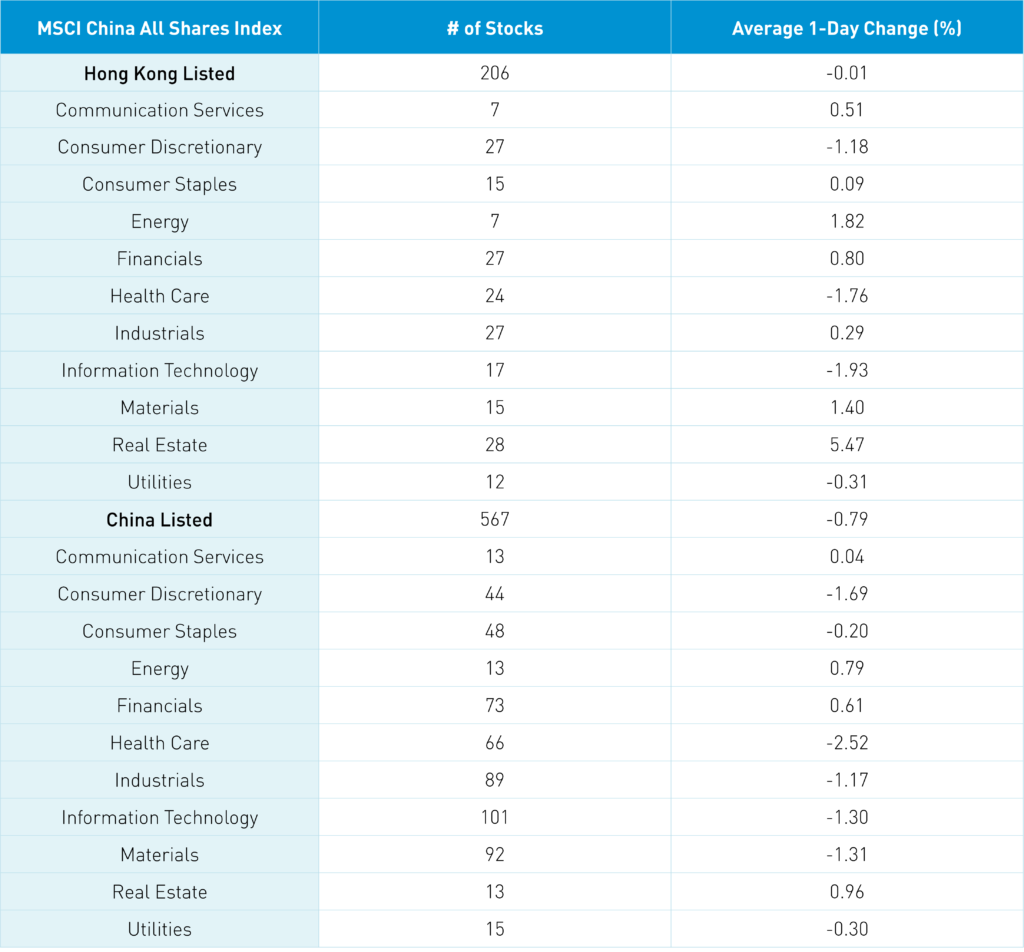

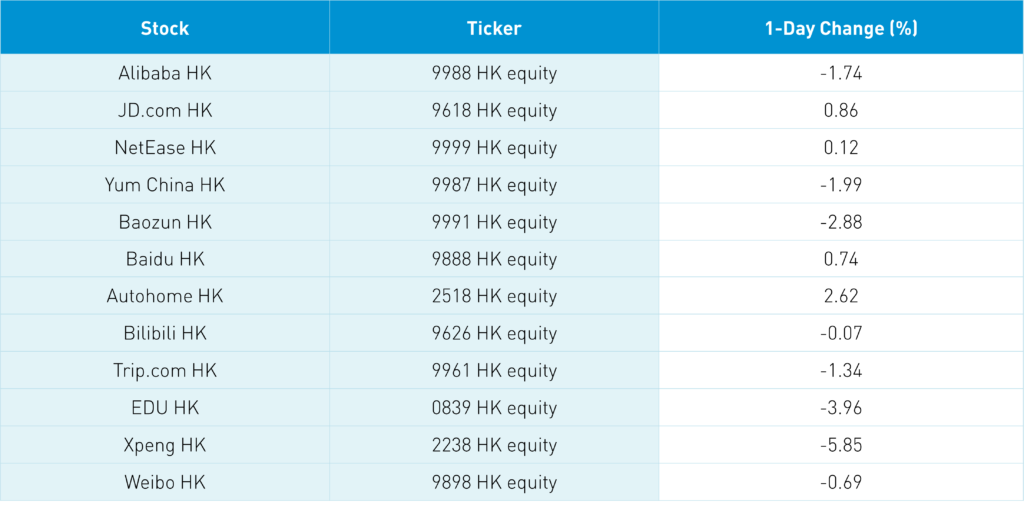

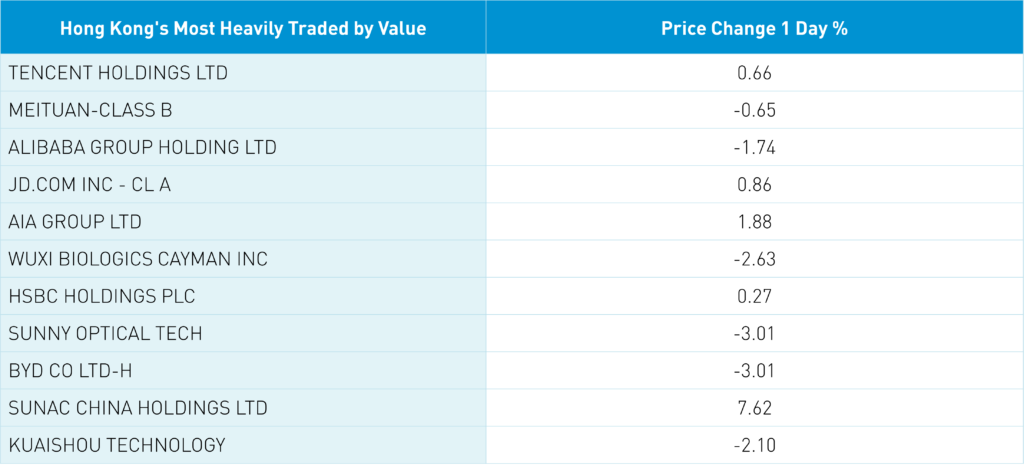

The Hang Seng Index managed to gain +0.06% while the Hang Seng Tech Index was off -0.98% on volumes that were up +2.36% from yesterday, which is only 70% of the 1-year average. Foreign investors are starting to pick up on China’s monetary easing narrative, which makes their underweight potentially dangerous if we get a rally. Hong Kong internet stocks didn’t fall nearly as much as the US names yesterday as Tencent +0.66% (Tencent US listing -5.14% yesterday), Meituan -0.65% (US -0.71% yesterday), Alibaba HK -1.74% (US -2.26%) and JD.com HK +0.86% (US -0.43%).

JD merchants will gain access to Shopify’s e-commerce platform while Shopify merchants can gain access to suppliers on JD’s platform. Alibaba HK felt yesterday’s ridiculous article on how Biden may ban US firms from accessing Alibaba’s cloud offering in the US. Hong Kong internet names eased at the end of day on a Reuters report, that according to “sources familiar with the matter,” internet platform companies would be banned from large investments. The article was widely re-reported by multiple media sources. This morning the Cyberspace Administration posted on their website that the article was not true.

Regardless, the Hong Kong names held up better than the US names. Real estate was a top performer in Hong Kong +5.47% and China +0.97% as the sector is viewed as a beneficiary of easing monetary conditions. Healthcare was off in both Hong Kong -1.76% and China -2.51% on reports several hormone drugs were added to the national procurement drug list as investors appeared to shoot first/ask questions later. Tencent was a small sell while Meituan was a small buy from Mainland investors via Southbound Stock Connect, though the former bought back stock again overnight.

Shanghai fell -0.33%, Shenzhen fell -0.92%, and the STAR Board fell -1.36% as the Mainland took a breather from recent outperformance, especially in light of Chinese New Year, which kicks off next Friday. Volumes were off -10.71% from yesterday, which is 101% of the 1-year average. Tomorrow, we will find out whether the loan prime rate will be cut, which would be further support for the real estate sector as mortgages are based on it.

Lithium, battery, and rare earth names have had a rough start to the year. CATL was off -2.86% while Tianqi Lithium -5.9% overnight though foreign investors were net buyers of the former via Northbound Stock Connect. Foreign investors bought $602mm of Mainland stocks today via Northbound Stock Connect. China 10 Year Treasury bond yield was 2.73% in a price rally, while CNY was basically flat versus the US $ and copper off -0.01%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.35 versus 6.35 yesterday

- CNY/EUR 7.20 versus 7.22 yesterday

- Yield on 10-Year Government Bond 2.73% versus 2.74% yesterday

- Yield on 10-Year China Development Bank Bond 3.03% versus 3.05% yesterday

- Copper Price -0.01% overnight