PBOC Gets the Green Light to Ease As Inflation Moderates

2 Min. Read Time

Key News

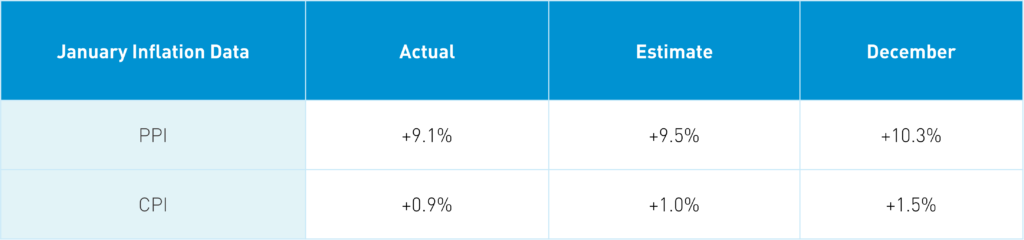

Asian equities had a strong day except for India’s small decline on Russia/Ukraine de-escalation hopes. China and Hong Kong had a good day, driven by declining Chinese inflation data. January’s PPI was 9.1% versus expectations of 9.5% and December’s 10.3% while CPI was 0.9% versus expectations of 1% and December’s 1.5% (% are year over year changes). While commodity prices are still high, food prices declined to ease consumer inflation. Investors cheered the data as it will likely allow the PBOC to continue their monetary easing without igniting inflation.

Meanwhile, in the US, the Fed has to tighten to curtail inflation as the US’ January CPI was 7.5% and PPI 9.7%. The US isn’t alone in tightening as many developed and EM countries are headed down the same path. US stocks are off on the anticipation of higher rates. Does anyone notice how well Chinese Treasury bonds are doing versus EM local currency and US dollar-denominated bonds? Using Bloomberg indexes over the last year, Chinese Treasury bonds and policy banks are +7.84% while EM local currency government bonds are down -1.36%. China has a tailwind while many markets face a headwind.

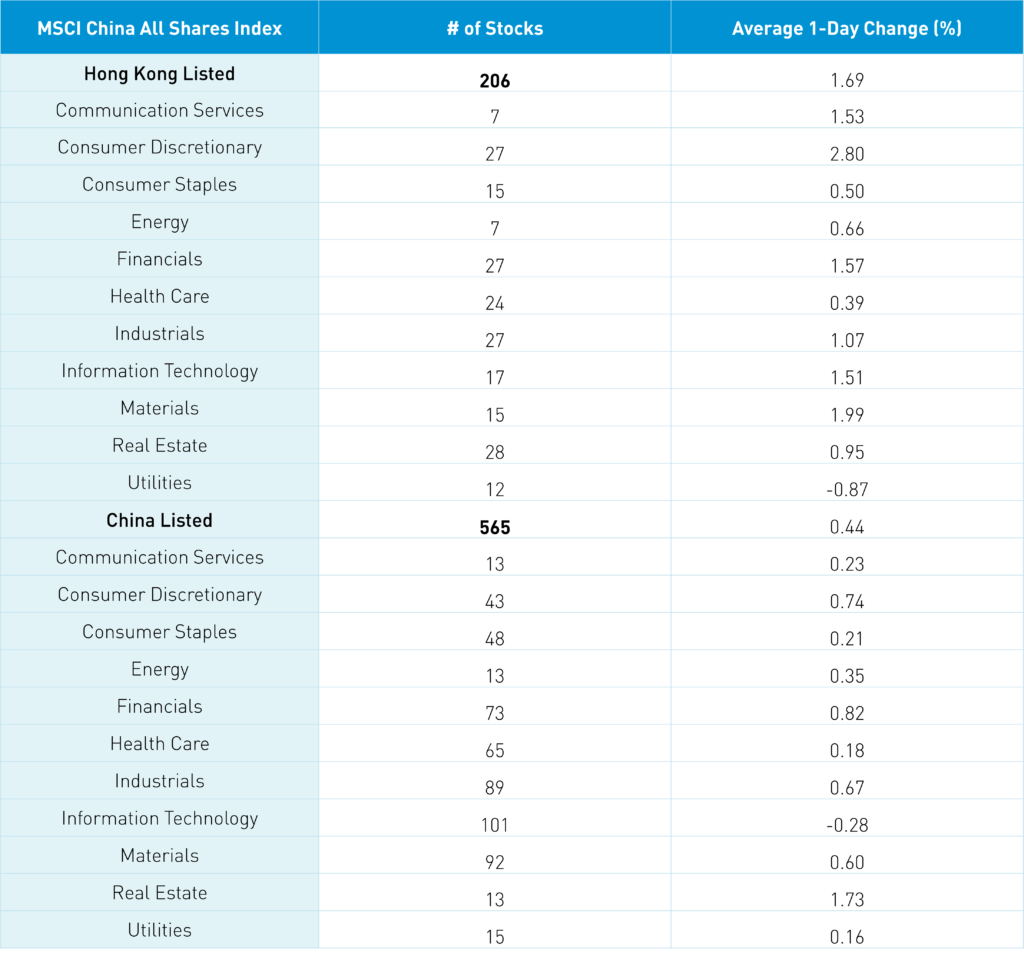

The Hang Seng Index gained +1.49% while the Hang Seng Tech Index jumped +2.3% as Hong Kong internet stocks had a strong day. Volumes were off -10.82% from yesterday, which is only 65% of the 1-year average though advancers outpaced decliners by more than 3 to 1. We would like to see volumes on an up day higher as it indicates conviction. Hong Kong is having a coronavirus outbreak that could see the quarantine and lockdown restrictions coming.

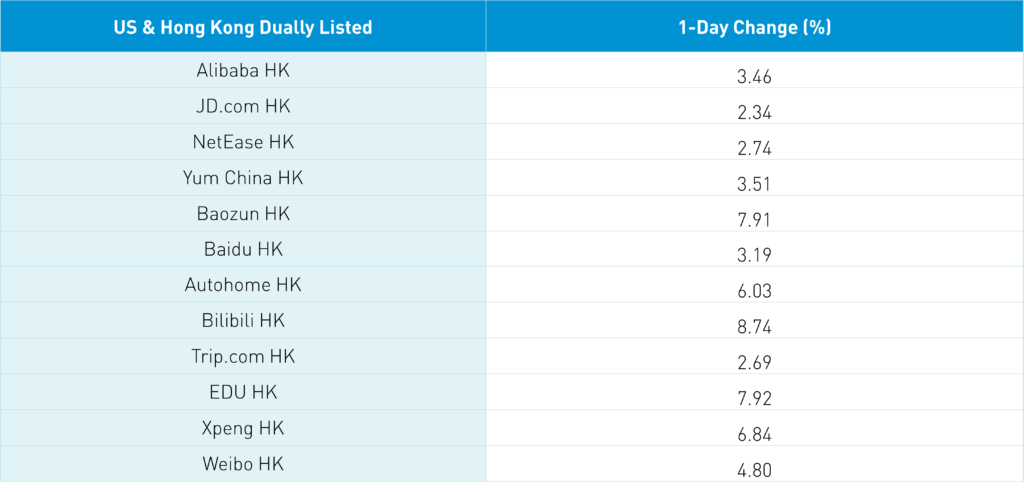

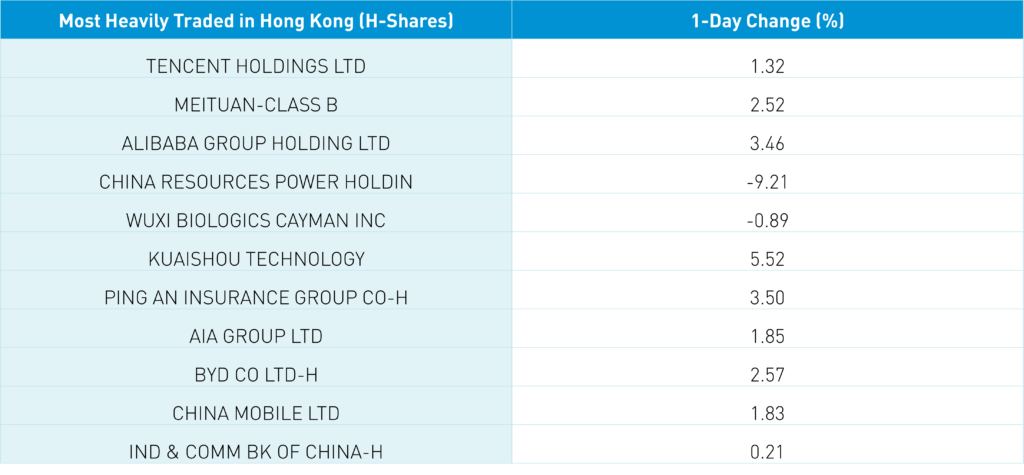

Hong Kong’s three most heavily traded stocks by value were Tencent, which gained +1.32%, Meituan, which gained +2.52%, and Alibaba HK, which gained +3.46% though both value and growth stocks and sectors had good days. Southbound Connect volumes have been light as Mainland investors have been small net sellers of Tencent and Meituan of late. China Resource Power (836 HK) was off -9.21% as the company pushes its renewable unit IPO to later this year.

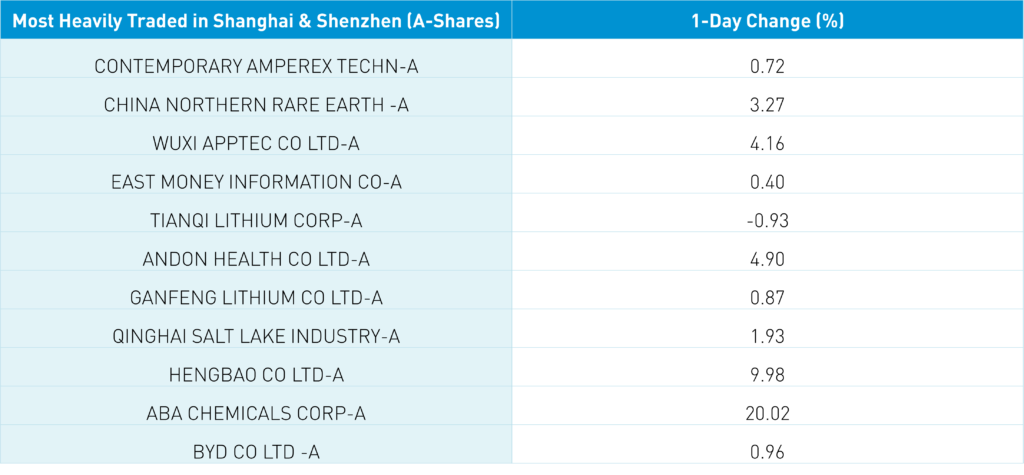

Shanghai gained +0.57%, Shenzhen gained +0.59%, and the STAR Board was off -0.46% on volumes -2.81% from yesterday which is 77% of the 1-year average. Advancers outpaced decliners by more than 3 to 1 in the Mainland as well as all sectors were in the green today less tech -0.28. Growth sectors/stocks were largely higher with a few exceptions such as Tianqi Lithium -0.93%. Interest rate-sensitive sectors were the best performers with real estate +1.73% and financials +0.81%. Foreign investors were net sellers of Mainland stocks today -$256mm via Northbound Stock Connect. Chinese Treasury bonds rallied along with copper +0.69% while the currency was flat versus the US $.

Hang Seng will provide the Hang Seng Index Pro-forma for the March rebalance this Friday. Predicting which names the committee will add is hard though we are apt to see Baidu’s Hong Kong share class added to the index as it gradually expands from 50 stocks to 80.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.34 versus 6.34 yesterday

- CNY/EUR 7.21 versus 7.20 yesterday

- Yield on 10-Year Government Bond 2.79% versus 2.80% yesterday

- Yield on 10-Year China Development Bank Bond 3.01% versus 3.02% yesterday

- Copper Price +0.69% overnight