China Talks to France, Reports FDI Increase of +11%

2 Min. Read Time

Key News

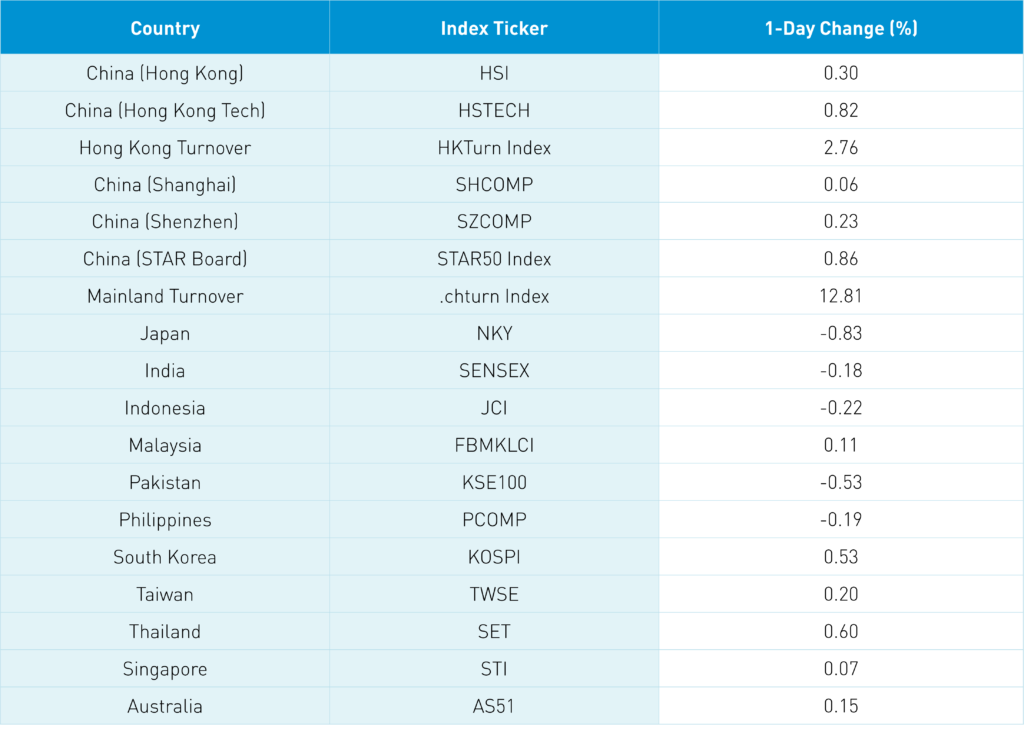

Asian equities were mostly higher overnight following mixed performance in the US on Wednesday, though Japan, India, and the Philippines were off. It was a relatively slow news day in Asia. Investors appear to be waiting for more clarity on Russia/Ukraine and internet earnings, which will be in full swing next week.

Xi Jinping and French President Emmanuel Macron had a phone call yesterday. China’s president spoke of improving ties between the two nations. The two leaders apparently reached six bilateral agreements in areas including agriculture, green manufacturing, finance, and aviation. It was expected that China would step up its diplomatic engagements in 2022 after the government’s internal focus throughout 2021.

China reported that foreign direct investment (FDI) increased +11.6% year-over-year in January versus +14.9% in December. While the FDI number was lower than expected, remember that FDI has increased every month since March, 2020.

The People’s Bank of China (PBOC) cut banks’ reserve requirement ratio (RRR) in December and has cut the one-year loan prime rate (LPR) twice, in December and January. The South China Morning Post had an interesting editorial overnight stating that easing has yet to lead to an equity market rally. It appears that the credit impulse among households and private businesses remains low given the policy uncertainty coming out of 2021. We believe the central bank will continue to ease through a variety of policy tools over the course of this year. However, lending to private businesses and households may not increase significantly until the second half of the year. But, with the Fed becoming more hawkish by the day, this bodes well for China equities, though it may not be an immediate rally.

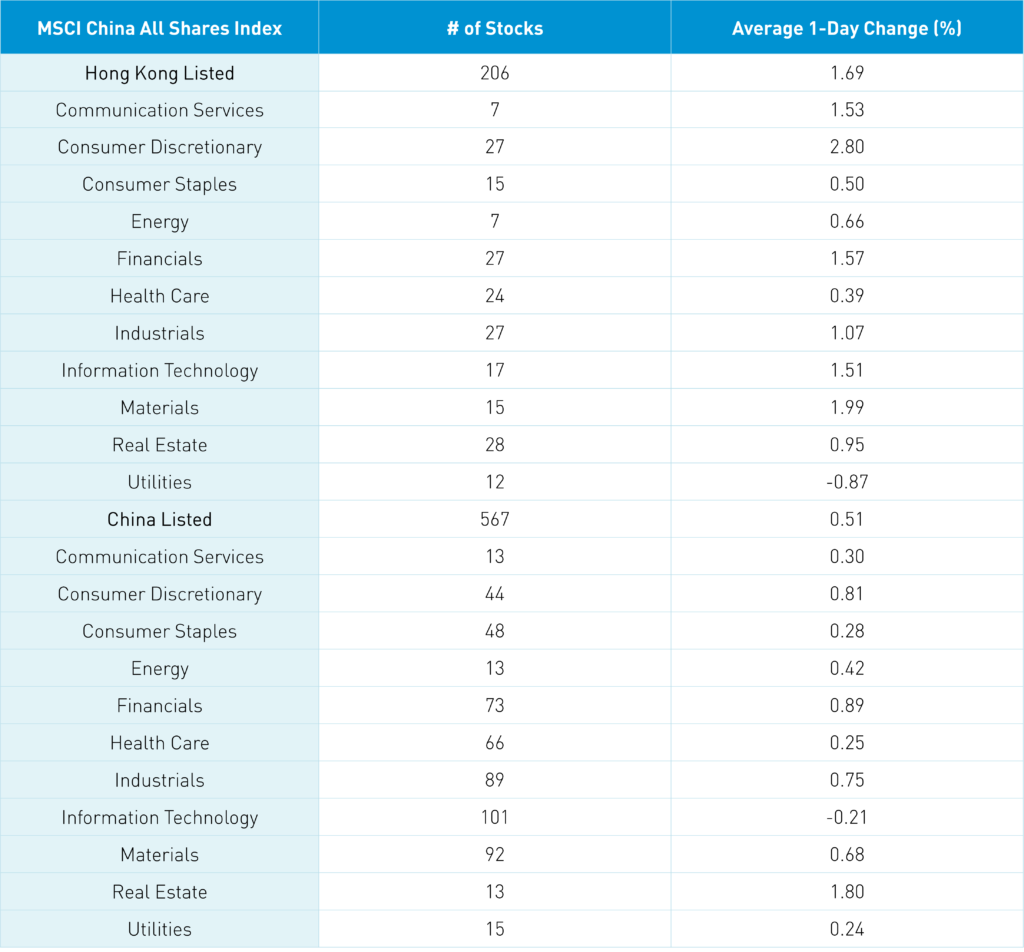

Real estate equities were broadly higher in both Hong Kong and Mainland China overnight as investors appear to be getting more comfortable with new policies and the financial straits of developers. Consumer staples names were also higher in both markets overnight as investors could be betting on a consumer comeback later this year.

Global pharmaceutical company Wuxi Biologics rebounded by +6.06% in Hong Kong overnight after the company’s stock cratered last week on news that it would be added to the US’ unverified/red flag list.

The electric vehicles (EV) ecosystem was up overnight as BYD gained +2.7% and other battery names were up on news that Zhejiang province will step up its speed the construction of charging infrastructure.

The Hang Seng Index gained +0.30% overnight while the Hang Seng TECH Index gained +0.30% as Hong Kong-listed internet stocks had a mixed, but net positive session. Volumes were up +2.76% from yesterday but remain well off the 1-year average. Hong Kong’s coronavirus situation does not appear to be getting any better as Beijing pledged support, but all but guaranteed a tough stance on increasing virus precautions.

Shanghai, Shenzhen, and the STAR Board were up +0.06%, +0.23%, and +0.86%, respectively, overnight on volumes that were up +12.81% from yesterday, though still slightly lower than the 1-year average. The growth to value rotation was not so evident in last night’s trading, which is good, as most sectors were up, though tech was slightly lower on the Mainland.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.34 versus 6.34 yesterday

- CNY/EUR 7.21 versus 7.20 yesterday

- Yield on 1-Day Government Bond 1.50% versus 1.50% yesterday

- Yield on 10-Year Government Bond 2.78% versus 2.79% yesterday

- Yield on 10-Year China Development Bank Bond 3.01% versus 3.01% yesterday

- Copper Price -0.06% overnight