Mainland China Outperforms Hong Kong as Investors Assess Geopolitical Risk, Internet Stocks Rebound, Week In Review

2 Min. Read Time

Week In Review

- Asian equities began the week lower on fears of a Russian invasion of Ukraine and came under further pressure Thursday when the invasion materialized.

- Mainland-listed semiconductor stocks had a positive week as many companies in the sector released overwhelmingly positive annual earnings reports on Tuesday.

- Alibaba reported Q4 earnings on Thursday, falling short of analyst expectations due to a high base of Q4 2020 and announcing that annual active consumers on its platforms had reached an all-time high of 1.3 billion.

Friday’s Key News

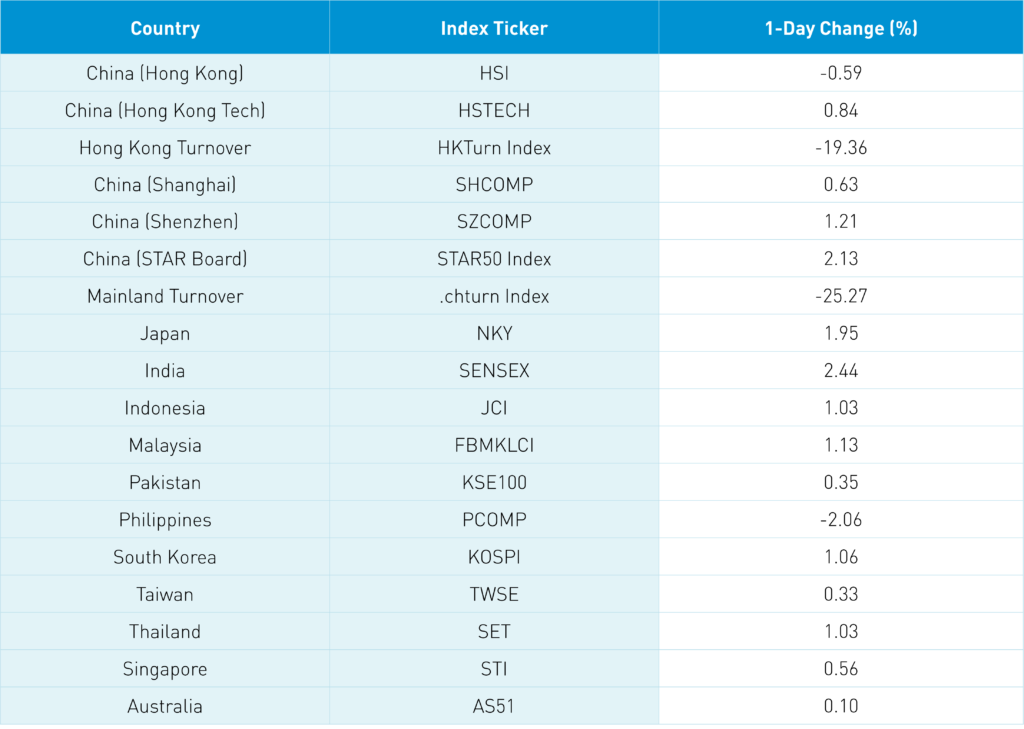

Asian equities were mostly higher overnight, rebounding from yesterday’s downdraft and ending the week on a positive note. Nonetheless, investors appeared cautious about the geopolitical risks going into the weekend.

We saw yet another instance overnight of Hong Kong underperforming the Mainland due to its high foreign ownership. Historical data suggests that China’s markets tend to be insulated to geopolitical shocks compared to developed markets. Hong Kong’s markets, though often representing China and emerging markets in Asia, tend to act like developed markets. This was clearly demonstrated in last night’s market action.

China has not directly condemned Russia’s invasion of Ukraine but has urged “restraint” from all parties. This could be a pivotal moment for US-China relations as the enemy of my enemy is always my friend. China does not benefit from sky-high energy prices especially after the energy shortage this winter. However, China may want to punt blame to the US. We will see.

CICC analysts released a research report on the potential impact that the Ukraine conflict could have on China’s economy. They concluded that it will have a relatively muted impact and maintained their 2022 GDP forecast for China, though higher energy prices could cause problems. China’s materials industry could be a beneficiary as demand looks domestically, Mainland-listed Inner Mongolia Baotou Steel has seen wild swings over the past week but is net positive for the week. Oil and gas may also see some margin improvements, but those improvements will be constrained by China’s pricing mechanism.

The electric vehicle ecosystem rallied overnight, with lithium and battery names leading the rebound as CATL gained +4.2%. A US Department of Energy plan to increase US energy dependence did not include restrictions on battery imports from China, which helped the sector overnight.

The Hang Seng Index fell by -0.59% overnight on volumes that were -19.36% lower than yesterday’s monster volumes. Hong Kong-listed internet and technology stocks rebounded as the Hang Seng TECH Index gained +0.84%.

Shanghai, Shenzhen, and the STAR Board gained +0.63%, +1.21%, and +2.13%, respectively, overnight on volumes that declined by -25.27% from yesterday.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD versus 6.32 versus 6.33 yesterday

- CNY/EUR 7.10 versus 7.06 yesterday

- Yield on 1-Day Government Bond 1.73% versus 1.70% yesterday

- Yield on 10-Year Government Bond 2.78% versus 2.79% yesterday

- Yield on 10-Year China Development Bank Bond 3.05% versus 3.06% yesterday

- Copper Price -0.53% overnight