Russia Leads To Risk-Off, Proactive Policies Announced From Dual Sessions

2 Min. Read Time

Key News

Asian equities were firmly in the risk-off camp due to the Ukraine/Russia situation, rising oil prices, and potential Fed rate hikes. China and Hong Kong were not immune to the downdraft despite an above-average 2022 GDP growth estimate and supportive economic policies from this weekend’s political and economic meetings.

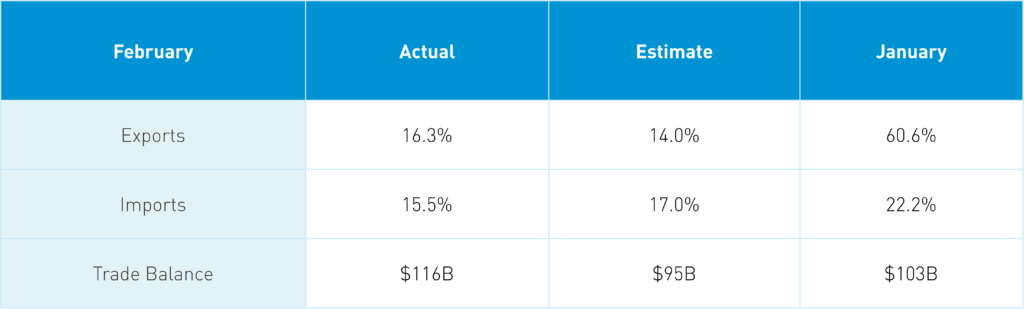

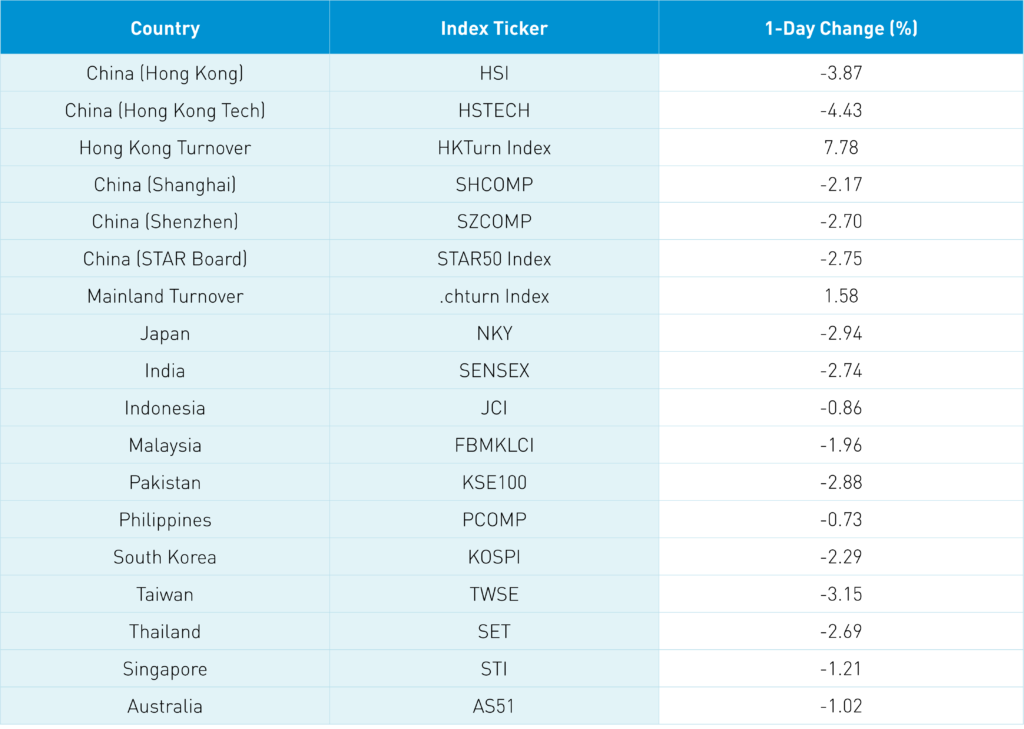

China’s export/import data looked good though it simply doesn’t matter on a day like today. One local broker called today “capitulation,” which I suppose is a good sign, as the Hang Seng Index fell -3.87% as volume increased +7.75% from Friday, which is 119% of the 1-year average. Declining stocks outpaced advancing stocks by 8 to 1 in Hong Kong.

Mainland investors were very active buyers via Southbound Stock Connect as Tencent and Meituan saw strong buying along with Kuaishou, though to a lesser degree. The reality that Hong Kong is on the precipice of a lockdown due to a significant coronavirus breakout did not help while the mainland also saw an uptick in daily cases.

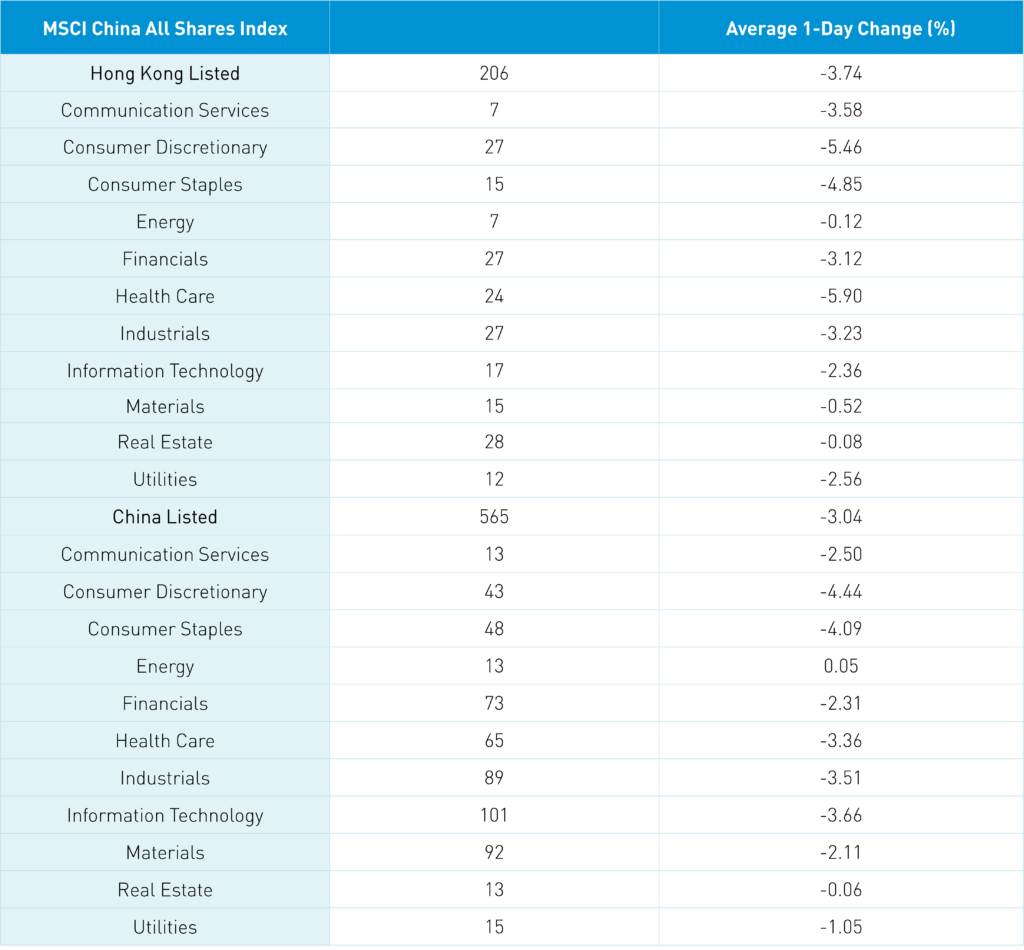

Consumer spending and travel names were particularly weak due to the outbreaks. We’ve mentioned in the past that warrants, which we call structured products here in the US, are very popular in Hong Kong. As the market falls, warrants hit price levels that require the structured products to be unwound, exacerbating market moves such as today.

Shanghai, Shenzhen, and the STAR Board were down -2.17%, -2.70%, and -2.75%, respectively, on volume that increased +1.58% from Friday, which is just below the 1-year average. Breadth was awful as 3,575 stocks declined versus 773 advancing stocks. Foreign investors sold $1.3 billion worth of Mainland stocks in a de-risking move. Gold and fertility names were one of the only positive sub-sectors today.

This weekend was the start of China’s dual sessions, which are comprised of the NPC and CPPCC. The meetings are political and economic in nature but also provide a check-in on how the government is progressing on its goals from the 14th Five Year Plan (2021 to 2025). On Saturday, Premier Li provided an overview of the 16,000-word Government Work Report. Key points for investors include:

- 2022 GDP Growth target 5.5%; 2021’s 8.1% growth was RMB 114.4 trillion ($18.11 trillion)

- Maintain CPI 3%

- Create 11mm urban jobs

- Budget deficit 2.8% lower than 2021’s 3.2%

- CNY should be stable

- We’ve always said stability is job #1 in China. Stability was mentioned 76 times in the Work Report.

- Clean energy consumption accounted for 25.5% of total consumption

On Sunday, President Xi’s speech emphasized energy and food security while the press conference afterward stressed the importance of US and China ties. Targeted tax cuts and promoting parents having more kids are other areas of focus.

February Trade Data (Year-to-Date, in USD)

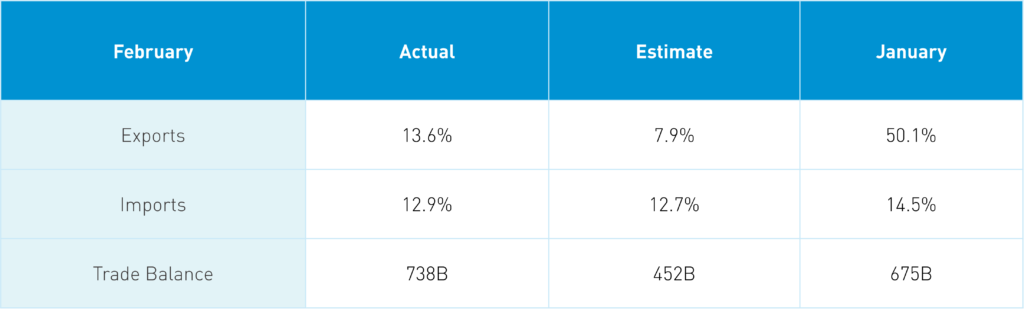

February Trade Data (Year-to-Date, in CNY)

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.32 versus 6.32 Friday

- CNY/EUR 6.87 versus 6.89 Friday

- Yield on 1-Day Government Bond 1.65% versus 1.67% Friday

- Yield on 10-Year Government Bond 2.81% versus 2.81% Friday

- Yield on 10-Year China Development Bank Bond 3.08% versus 3.09% Friday

- Copper Price +2.21% overnight