Mainland Gives Capitulation Sign as Decliners Outpace Advancers 10 to 1

3 Min. Read Time

Key News

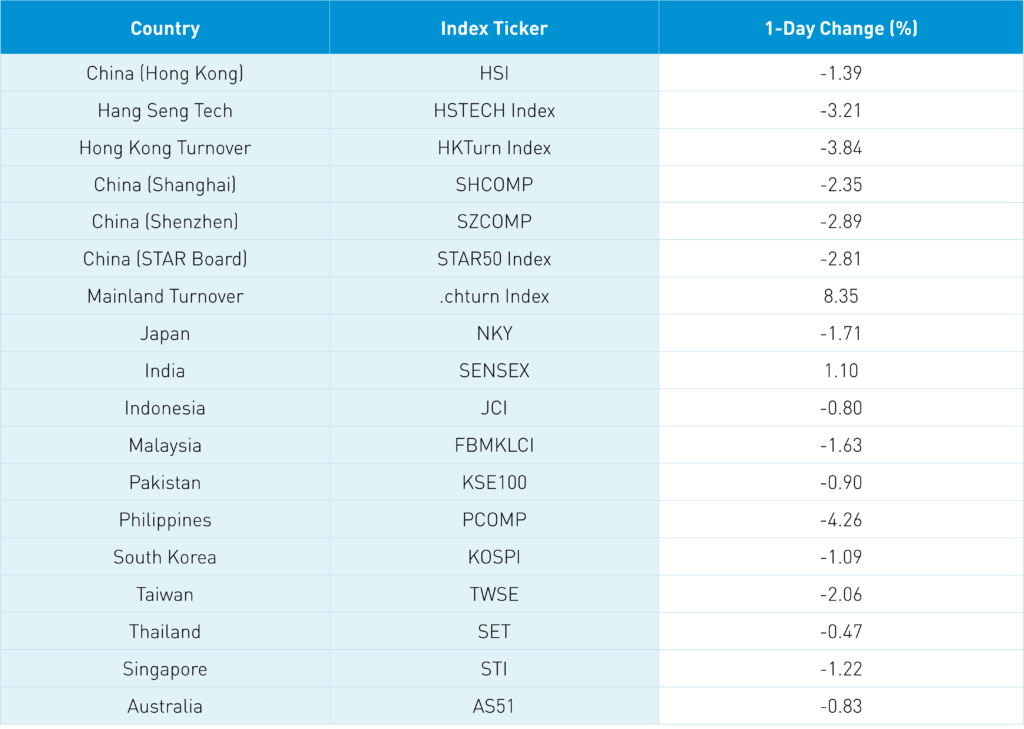

The wind was howling so loud last night it woke me up as an ill wind was blowing in Asia as equity markets were down overnight apart from India which didn’t get the message that the world is ending (I’m kidding!). The move is strange as India is a commodity importer, like China, which explains why it abstained from the UN vote condemning Russia’s invasion. India is the most western country in Asia so it's likely they were a beneficiary to markets rebounding from oversold levels. Obviously, the Ukraine/Russia war drove market action but the spillover effect on the global economy and rising natural resources, raw materials and food prices.

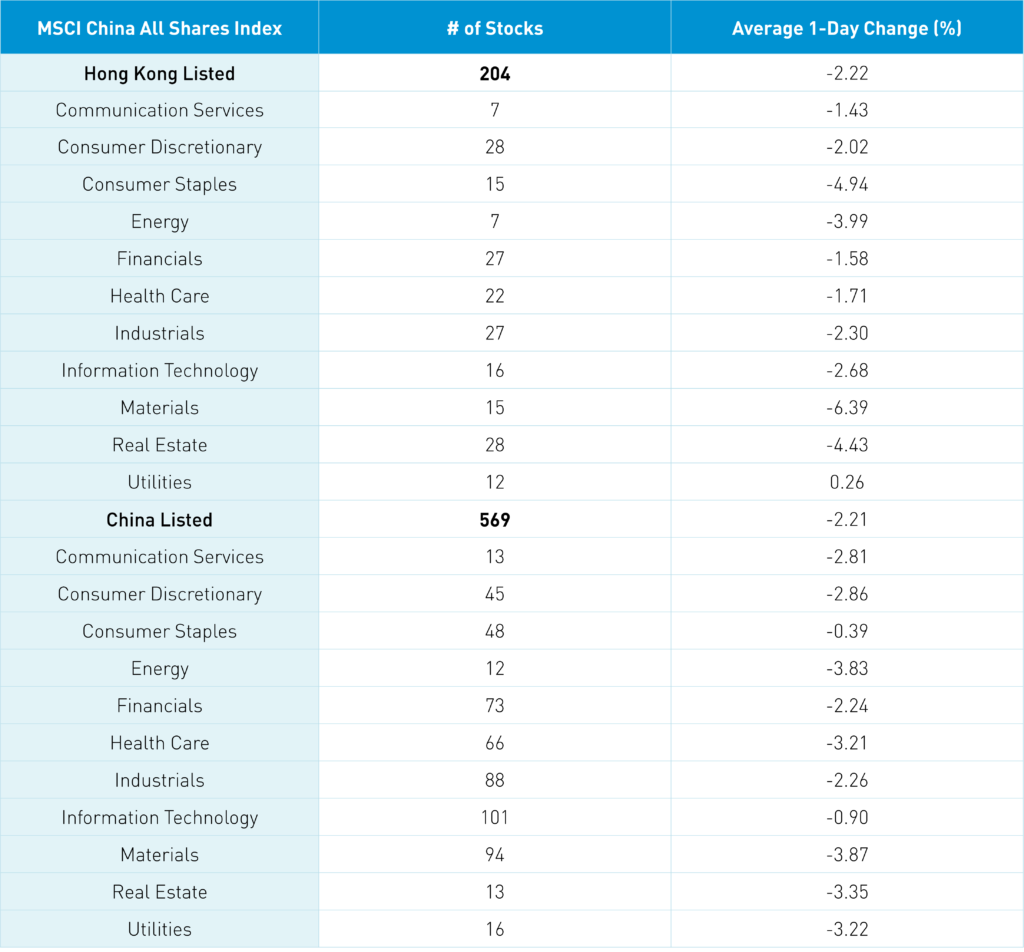

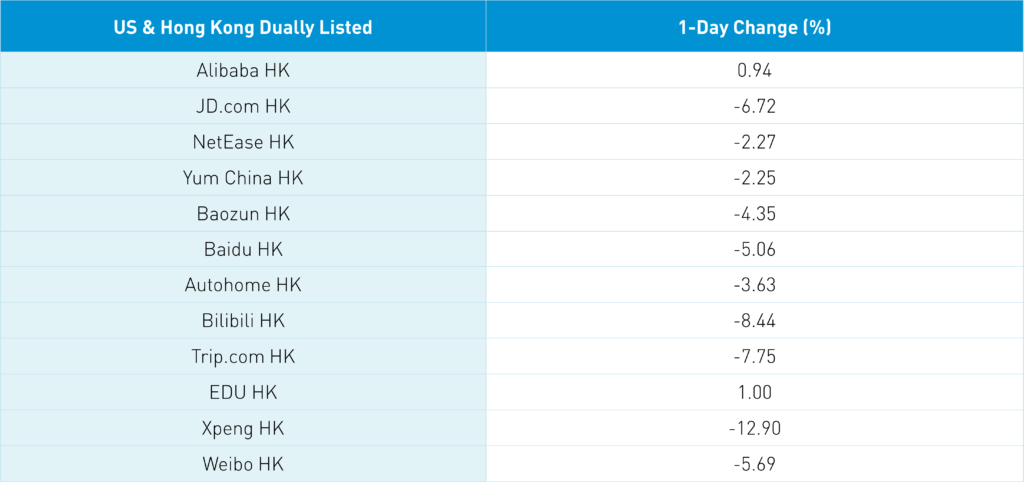

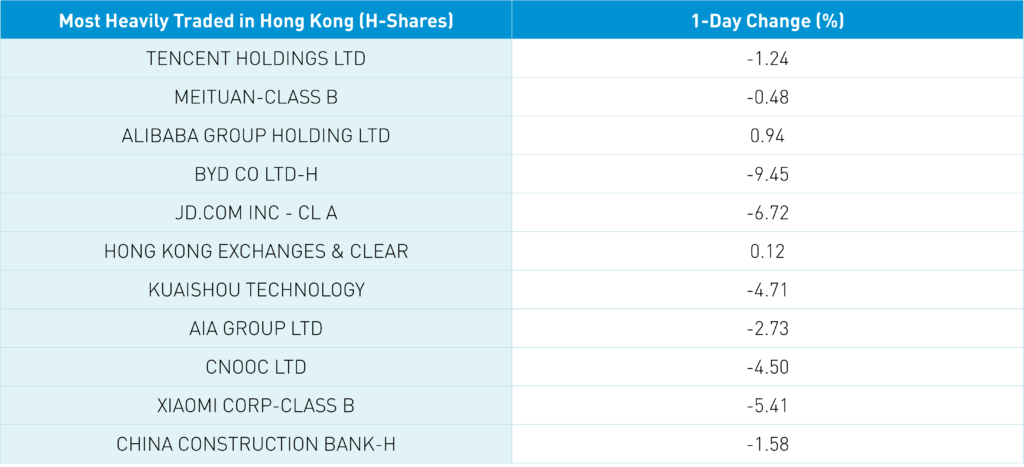

The Hang Seng Index was off -1.39% closing below the 21k level on volume -3.87% from yesterday which is 114% of the 1-year average. The minute the Hang Seng hit 21k, brokers would be required to redeem structured products due to a key knock out price being reached. Hong Kong investors demand for principal/downside protection structure products is exacerbating the market’s downside move. Decliners outpaced advancers by nearly 7 to 1. JD.com HK, which reports financial results Thursday, was off -6.97% overnight on no news other than it had been outperforming it's peers. Tencent’s coming spinoff of it's shares could have been a factor. Alibaba HK managed to gain +0.94% in a good sign while Mainland investors were buyers of both Tencent and Meituan.

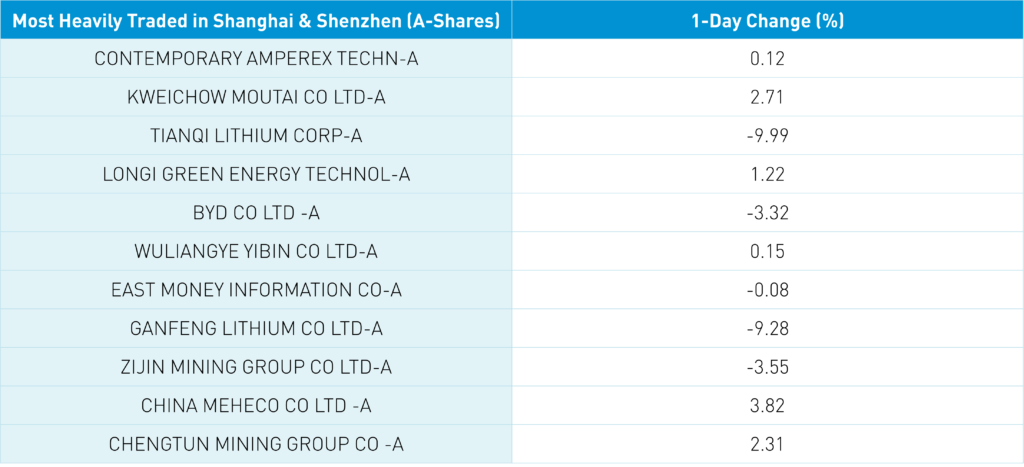

Shanghai, Shenzhen and STAR Board were off -2.35%, -2.89% and -2.81% on volume +8.35% from yesterday which is just above the 1-year average. Declining stocks outpaced advancing stocks nearly 10 to 1 (3,987 decliners and only 408 advancing stocks). Energy and material stocks were hit hard in both China and Hong Kong. Higher energy prices increase the viability of clean energy producers such as solar and wind which had a decent day in Hong Kong and China. Lithium stocks did very poorly on Russian supply curtailments along with EV stocks as raw material prices skyrocket. Chinese EVs were hit for the same reason despite February sales data being released overnight. Mainland listed EV battery maker CATL, which was hit hard last night, managed to rebound today. Mainland semiconductors managed to close in the green today as well. Foreign investors sold $1.377B of Mainland stocks via Northbound Stock Connect. Chinese Treasury bonds rallied, CNY appreciated slightly versus the US $ and copper was off.

Could China broker a peace settlement? China imports grain from the Ukraine and natural resources from Russia which puts it in an interesting position. Resolving the issue is very much in China’s economic interest.

Internet regulation has come up in the dual sessions but nothing specific. I don’t see anything explicitly negative to the fundamentals of the space thus far.

Markets have been very much in risk off mode due to the Ukraine crisis, surging oil prices and the specter of higher US interest rates. It is hard to quantify though I suspect an element of China’s recent weakness is driven by investors witnessing Russia’s removal from financial markets. Could the same happen to China? First, western politicians and western media have hammered us with an anti-China narrative. The Crimean Peninsula was taken by force from the Ukraine. Western political and western media response? Nothing. Malaysian Airlines Flight 18 from Amsterdam to Kuala Lumpur was shot down over the Ukraine. Western political and western media response? Nothing. We are witnessing the repercussions of an appeasement policy. Apologies for the rant but significant political and media attention has been misdirected in my opinion. China’s GDP is nearly 8X bigger than Russia’s. Let’s take a look at the trade importance of each country.

In 2020 according to the Bureau of Economic Analysis:

US Exports of Goods and Services to Each Country:

- China $165B (7.8% of all exports)

- Russia $8.907B (0.4% of all exports).

US Imports of Goods and Services in 2020:

- From China $450B (16% of all imports)

- From Russia $18.223B (0.6% of all imports).

The US Direct Investment Position in Each Country in 2020:

- China was $123.9B

- Russia’s $12.5B

As we’ve mentioned in the past, trade data doesn’t include goods manufactured and sold in China by US companies though the BEA does calculate the figure at $378B in 2019 (the latest data available). Remember these profits flow back to Cupertino, Detroit, Seattle etc. US companies generated $47B in Russia. Cutting Russia off from the global economy could contribute to a global recession. Cutting China off would undoubtedly lead to a global depression.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.32 versus 6.32 yesterday

- CNY/EUR 6.89 versus 6.88 yesterday

- Yield on 10-Year China Government Bond 2.83% versus 2.81% yesterday

- Yield on 10-Year China Development Bank Bond 3.10% versus 3.08% yesterday

- Copper Price -1.12% overnight