Trip.com Beats Expectations Following Tencent’s Tumble

2 Min. Read Time

Key News

Asian equities were mixed overnight after a choppy US equity session yesterday in advance of NATO talks on Ukraine. The US reinstated tariff exemptions on 352 Chinese goods that had their exemptions expire in 2020. The exempted goods did decrease from the 549 goods previously exempted. Tariffs are playing a small role in inflation according to Janet Yellen. The move is a positive step in what could lead to trade negotiations.

The South China Morning Post reported overnight that the finance ministry would check US listed Chinese companies’ audit for “state secrets or sensitive data such as personal identity numbers”. They would then deliver the audit to the PCAOB. Weibo (WB US) was the sixth Chinese company added to the SEC’s list of companies not adhering to the HFCAA after filing their 2021 annual report on March 10th. The SEC will continue to add all US Chinese companies to this list thus providing a good incentive for both sides to find a resolution. Weibo has already listed in Hong Kong so investors have an escape route if necessary.

Bloomberg News reported on a PCAOB statement today indicating that reports of a resolution to HFCAA are premature. The statement is the first time the PCAOB has directly acknowledged the talks to resolve the HFCAA between the CSRC, China’s SEC, and the US side of SEC and PCAOB. The PCAOB stated according to Bloomberg they are unwilling to provide exemptions for US listed Chinese companies even if those companies operate in “sensitive industries”. A sticking point in negotiations will be addressing state secrets and personal data. The real issue is the small number of State Owned Enterprises (SOEs) amongst the +270 US listed Chinese companies as there might be state secrets or sensitive information in their audits. This is simply not the case for the private companies. Earlier this week Reuters reported that the CSRC told Alibaba, JD.com and other private companies they should prepare for more audit disclosures. This would indicate a segmentation between private and SOE listed companies is the path for a resolution. Allowing the private companies to comply, would also provide time to address the more complicated situation of SOEs.

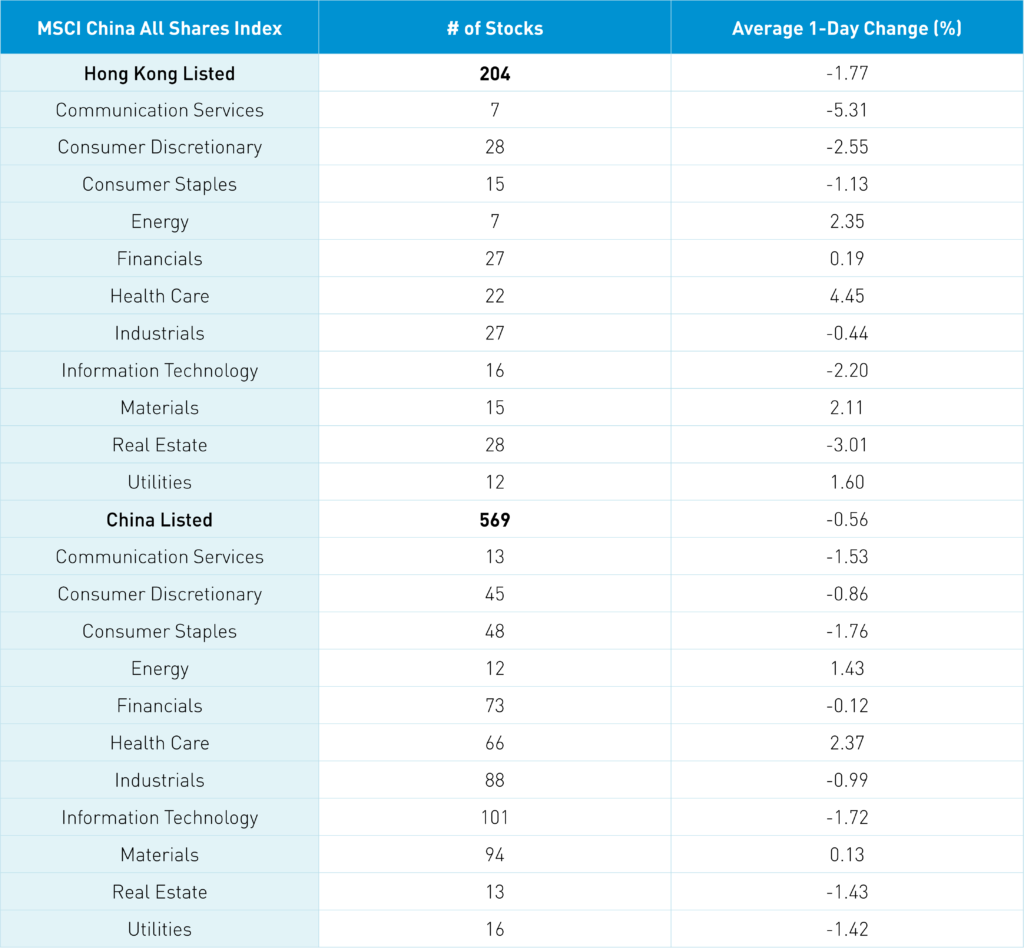

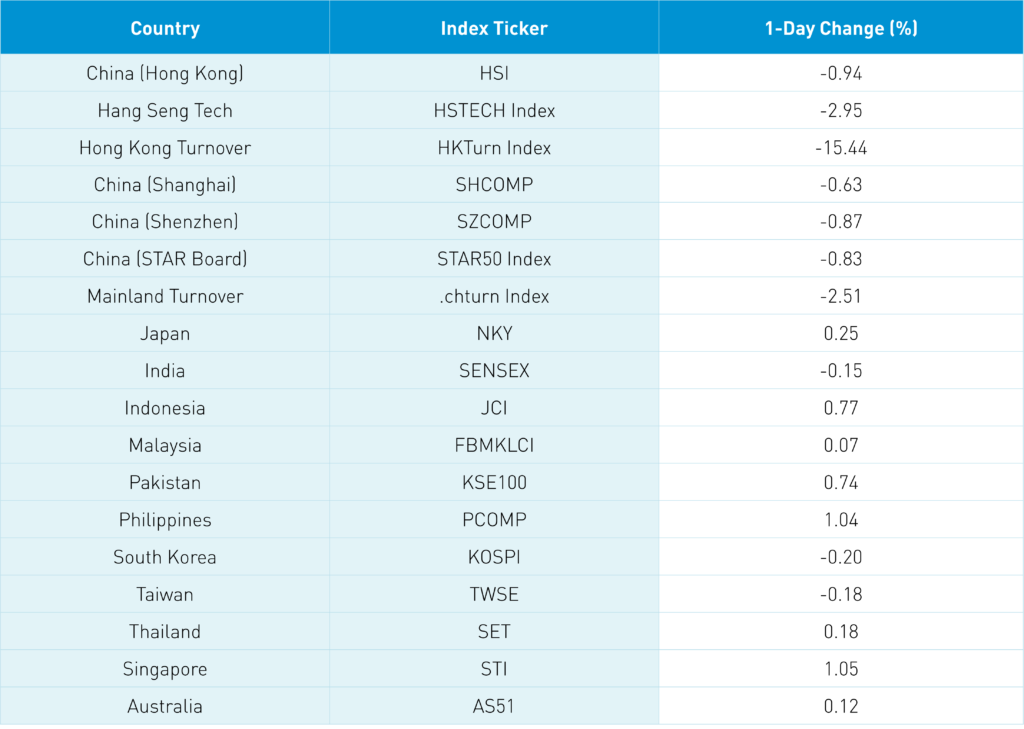

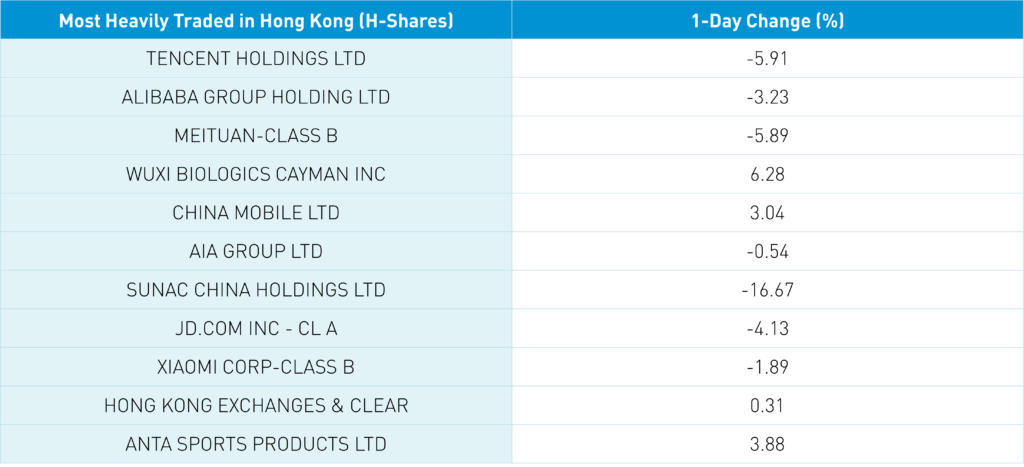

The list of Tencent’s lackluster Q4 results weighed on internet names as the Hang Seng -0.94% with the Hang Seng Tech -2.95%. Volumes were light -15.44% from yesterday which is just above the 1-year average while 249 stocks advanced, and 240 stocks declined. Hong Kong short selling turnover was off -22% from yesterday which is 112% of the 1-year average though down from recent levels. Shorts might be a touch nervous. Tencent’s results likely weighed on investor sentiment for Meituan off -5.89% in advance of earnings tomorrow as Mainland investors were sellers via Southbound Stock Connect. Trip.com HK (TCOM US, 9961 HK) gained +7.59% overnight in Hong Kong after beating low analyst expectations.

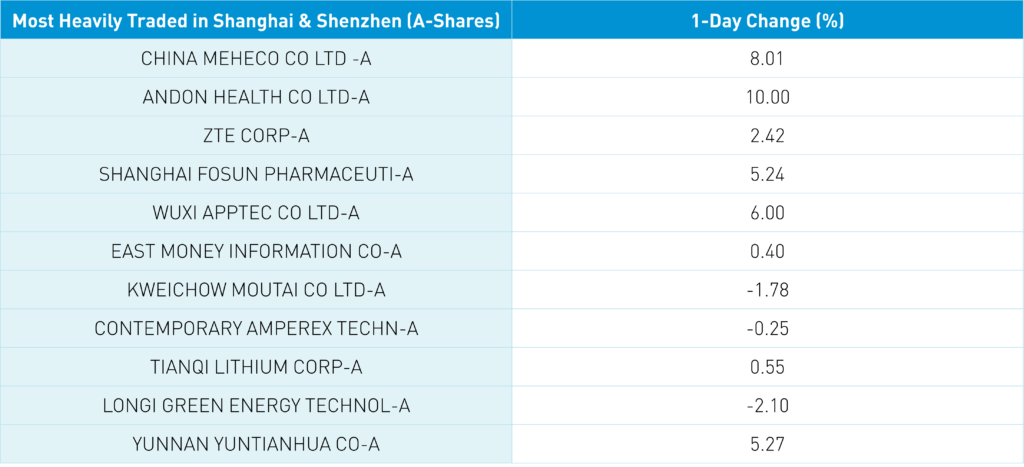

Healthcare was the best performer in Hong Kong +4.45% and China +2.39% due to covid outbreaks in China. Real estate was weak in both markets -3.01% Hong Kong and -1.41% China on news developer Suanc -16.67% is asking bond holders for an extension. Worth noting Evergrande’s bond due yesterday jumped to $14.04 from $12.56 as the company negotiates with bond holders.

Shanghai -0.63%, Shenzhen -0.87% and STAR Board -0.83% on volume -2.51% from yesterday which is 86% of the 1-year average. Foreign investors sold -$20mm of Mainland stocks via Northbound Stock Connect. Chinese Treasury bonds rallied, CNY appreciated very slightly versus the US $ and copper +0.67%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.37 versus 6.37 yesterday

- CNY/EUR 7.01 versus 7.00 yesterday

- Yield on 10-Year Government Bond 2.81% versus 2.83% yesterday

- Yield on 10-Year China Development Bank Bond 3.06% versus 3.07% yesterday

- Copper Price +0.67% overnight