Buyback Bonanza as Regulators Talk About Talking

3 Min. Read Time

| Upcoming Webinar: |

| Join us Wednesday, April 6th for our webinar at 11:00 am EDT. Carbon Reset: Where Allowance Markets Go From Here Click here to register. |

Key News

Asian equities were largely off overnight.

The SEC added Weibo, Baidu, iQIYI, and three other China ADRs during US trading hours to their HFCAA non-compliant list. All 273 US-listed Chinese ADRs will be on the SEC list as the companies file their 2021 annual report with the SEC. After the US close, Bloomberg interviewed SEC Chair Gary Gensler, who gave measured comments on the discussions to resolve the issue. Chairman Gensler pointed out that sensitive information, i.e. state secrets, are unlikely to be included in an audit. That may be true for SOEs but is likely not the case for private companies with far less sensitive information. We hope the two sides will differentiate between these two types of companies. Ultimately, the SEC is the enforcement agency whose mandate is to enforce the Holding Foreign Companies Accountable Act (HFCAA), a US law.

The China Securities Regulatory Commission (CSRC) responded with equally measured comments. The CSRC stated, “Both sides are willing to resolve differences and problems, and the final result depends on both sides' wisdom and original aspirations.” Since last August, CSRC Chairman Yi and SEC Chairman Gensler have had three video calls to discuss the matter, according to the CSRC. Hopefully, the two sides can put this issue to bed.

My colleague Derek noted that the value of goods sold by Alibaba is 3X larger than Amazon though its market cap is 5X smaller. JD.com sells almost as much as Amazon but has a market cap of only $95 billion versus Amazon’s $1.682 trillion. Big fund families will dabble in the US ADRs because they are so cheap, but they will want to keep the names out of their top ten, which will be disclosed tonight (quarter-end). Until they get definitive clarity on HFCAA, they won’t take the career risk of buying the names in size. Hedge funds don’t have this problem as they can hedge their position. These names are like a coiled spring waiting for a definitive agreement as, ultimately, this is a very solvable issue. Yes, there is the potential for policy error, though would you want your tombstone/legacy being you couldn’t solve this? I don’t think so either.

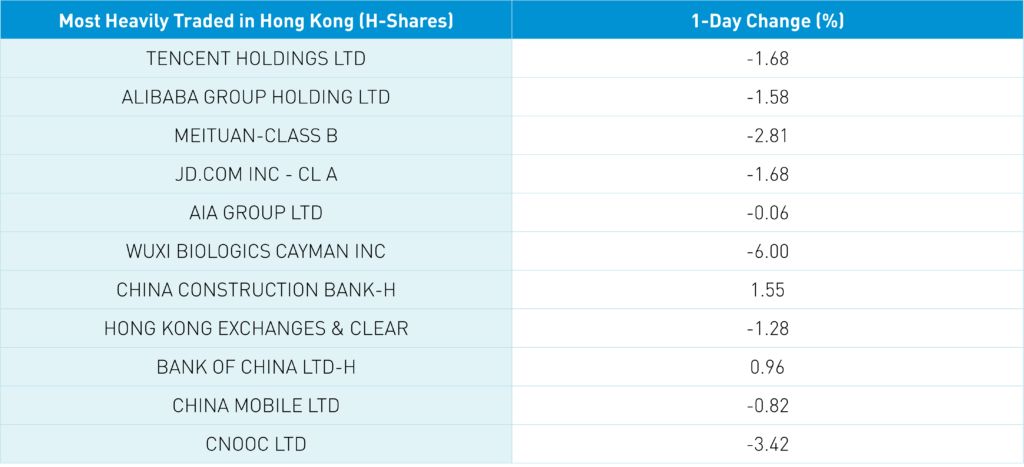

The companies with US ADRs believe their stocks are cheap, as we’ve seen numerous companies announce buybacks. Alibaba increased their buyback plan to $25B from $15B while Tencent bought other 799k shares overnight, extending their buying for the 5th day. Vipshop (VIPS US) announced they will buy $1B of their stock in the next 24 months after announcing a $500mm buyback last year. Weibo (WB US) announced overnight they would be $500mm of stock over the next 12 months. The key is the companies' message: the stock is cheap. They are also indicating that the China regulatory cycle is over.

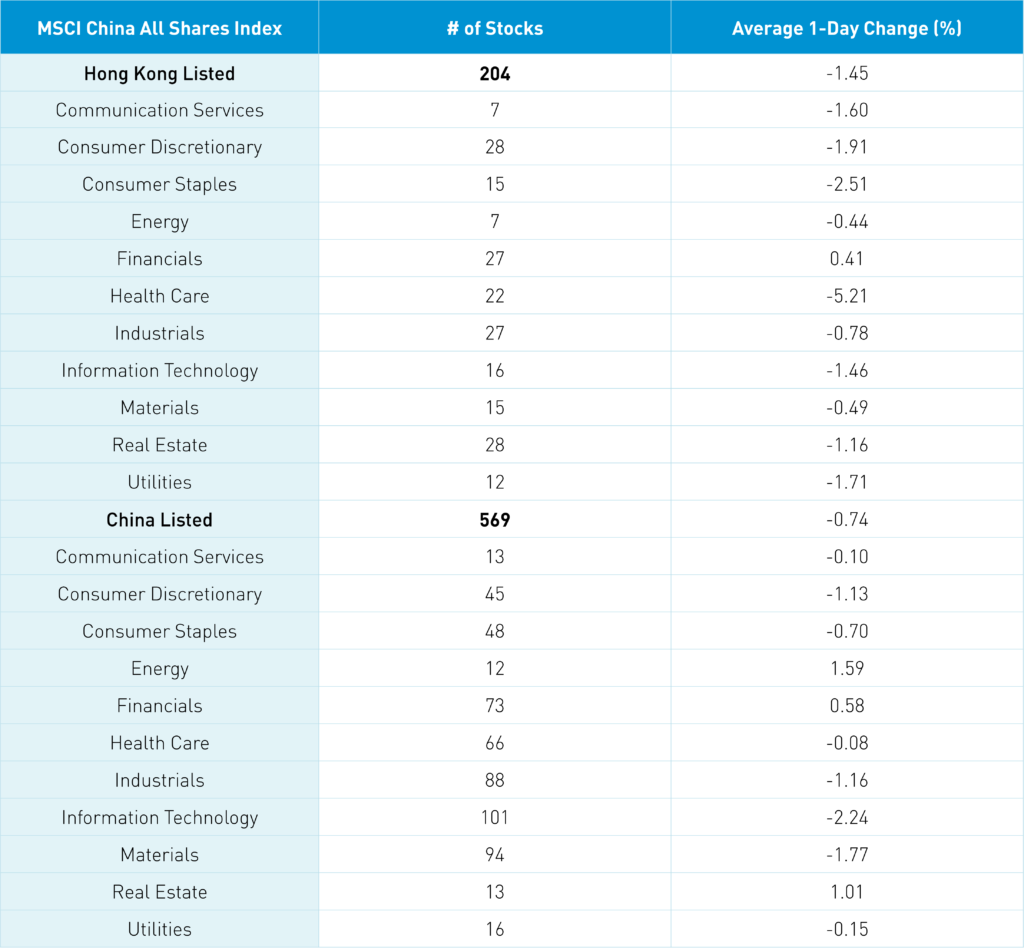

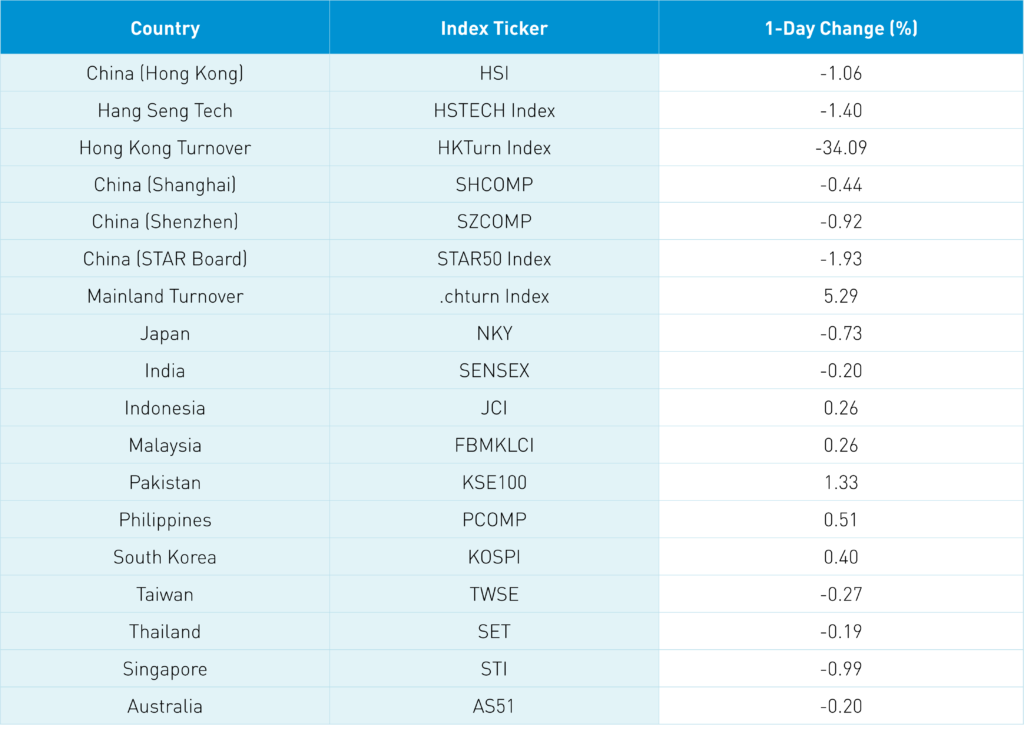

The Hang Seng Index was off -1.06%, while the Hang Seng Tech Index was off -1.4% as volume declined by -34% from yesterday, only 69% of the 1-year average. Investors might be packing their bags early in advance of their long weekend due to a market holiday next week. Short selling volume was below the 1-year average. The only sector in the green was financials today on strong financial results, while healthcare was clipped -5.21% after its recent strong move. Decliners outpaced advancers 3 to 1. Southbound Stock Connect was closed in advance of the Mainland’s close on Monday and Tuesday. Hong Kong is closed on Tuesday.

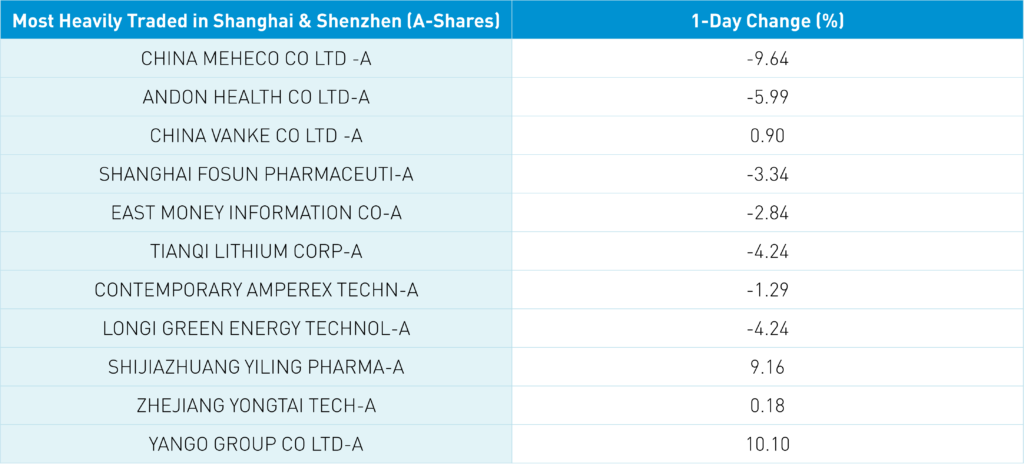

Shanghai, Shenzhen, and STAR Board eased -0.44%, -0.92%, and -1.93%, respectively, as volume increased +5% from yesterday, which is 95% of the 1-year average. Decliners outpaced advancers 2.450 to 1,878. Energy +1.64% led by coal stocks, real estate +1.06% and financials +0.63% while tech -2.19% as value stocks outpaced growth stocks. The market is expecting supportive policies on real estate. Bloomberg reported that the PBOC is leading efforts to create “a new fund to backstop troubled financial firms, according to people familiar with the matter.” Real estate was mentioned in Vice Premier Liu He’s speech, so this could happen. The clean energy ecosystem was off, led lower by lithium names and battery names, including popular stocks like Tianqi Lithium, which fell by -4.24%, CATL, which fell by -1.29%, and Longi Green Energy, which fell by -4.24%. Today, foreign investors bought $166 million worth of Mainland stocks via Northbound Stock Connect. Treasury bonds eased, CNY gained versus the US dollar, and copper -0.18%

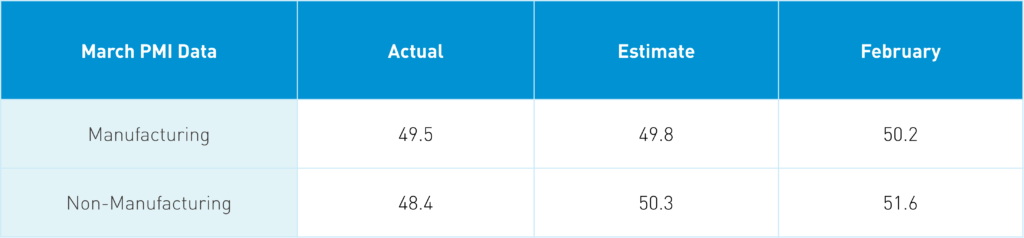

March Manufacturing PMI data was released overnight. We’ve noted export orders continue to slow as the global stimulus-driven buying of iPhones, Pelaton bikes, laptops and computers continues to slow. Many of these goods are either manufactured in China or inputs in their manufacture are made in China. This is why policy needs to get domestic consumption going to offset further manufacturing weakness. The market didn’t seem overly concerned with the release.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.34 versus 6.35 yesterday

- CNY/EUR 7.04 versus 7.07 yesterday

- Yield on 10-Year Government Bond 2.79% versus 2.77% yesterday

- Yield on 10-Year China Development Bank Bond 3.04% versus 3.02% yesterday

- Copper Price -0.18% overnight