Differentiating Private and State-Owned Companies May Be the HFCAA Solution

3 Min. Read Time

| Upcoming Webinar: |

| Join us Wednesday, April 6th for our webinar at 11:00 am EDT. Carbon Reset: Where Allowance Markets Go From Here Click here to register. |

Week in Review

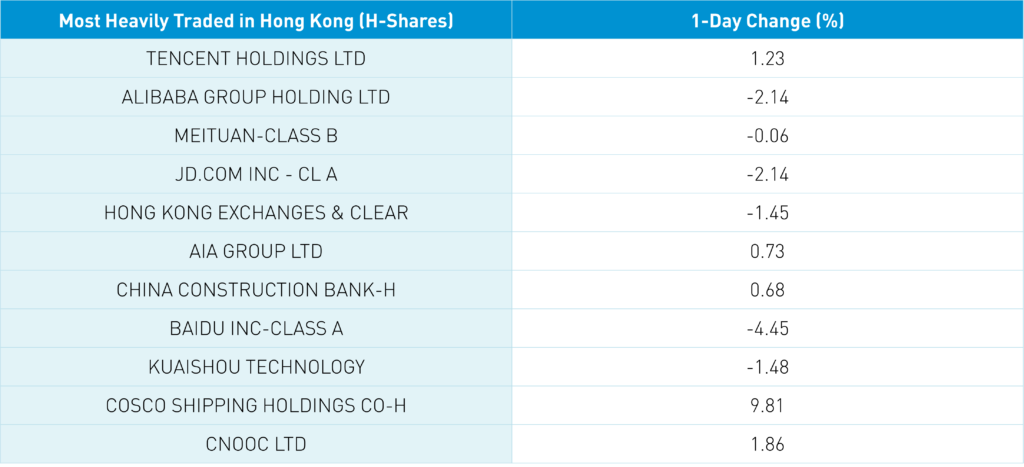

- Meituan (3690 HK) jumped +11.56% after posting better-than-expected financial results on Monday after the Hong Kong close last Friday.

- TikTok rival Kuaishou jumped +4.6% in advance of Q4 financials on Tuesday which were released after the Hong Kong close beating expectations.

- A Mainland media source on Wednesday noted that among the 130 Mainland-listed companies that had reported, 87.69% (114) reported positive results.

- Tencent, Alibaba, and China internet companies on Thursday broadly believed their stocks are cheap and are currently buying back shares.

Key News

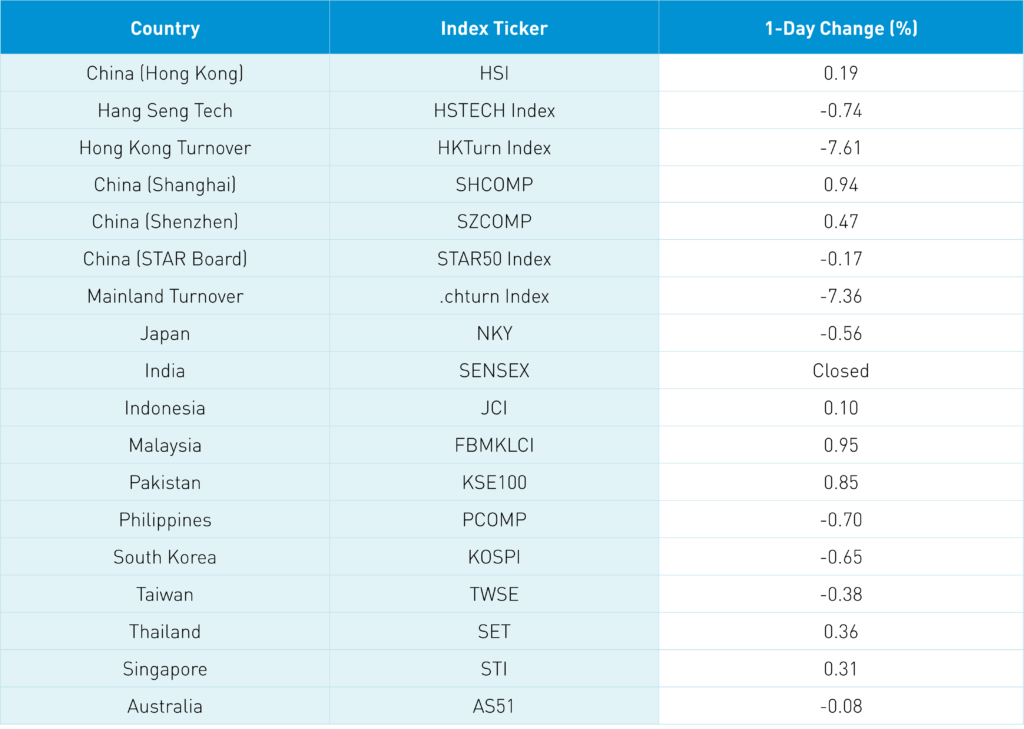

Asian equities had a mixed night. China outperformed while Japan, Taiwan and South Korea were down. India had a market holiday. This morning after the Hong Kong close, Bloomberg News reported that the CSRC, China’s SEC, is working with other Chinese regulators “…to give U.S. regulators full access to auditing reports of the majority of the 200-plus companies listed in New York as soon as mid-this year” according to “people familiar with the process”. The plan would differentiate private companies and State Owned Enterprises (SOEs) as the former has no state secrets/sensitive information while the latter might. We have long advocated this differentiation. Good news though investors will want to see tangible follow through following Vice Premier Liu He’s directive to get a deal done.

With that said, big global mutual fund families can buy the US China ADRs without their investors knowing they did until the end of June when they have to show their top ten holdings. If the names go up, you keep them and the fund families could say look how smart we are! If the stocks go down, one could sell them before the end of June and no one would know you ever owned them. Hedge funds don’t have that problem buying the names because they can hedge their long positions with short positions. Yesterday’s market weakness in the US ADR space could have been driven by big fund families trying to get the ADRs out of their top ten holdings. Regardless, let’s hope this issue gets put to bed!

China is closed Monday and Tuesday while Hong Kong is closed Tuesday leading to light volumes. What’s interesting? Market shrugged off a weak Caixin Manufacturing PMI release of 48.1 versus expectations of 49.9 an Feb’s 50.4. Why? Stimulus coming and effect of covid. Interesting travel related stocks had a good day in China and Hong Kong. Cities with lockdowns won’t be traveling but China is a big country so maybe more folks are traveling more than anticipated. Mainland media reported the State Administration of Taxation is accepting VAT refund requests from small/private companies i.e. stimulus.

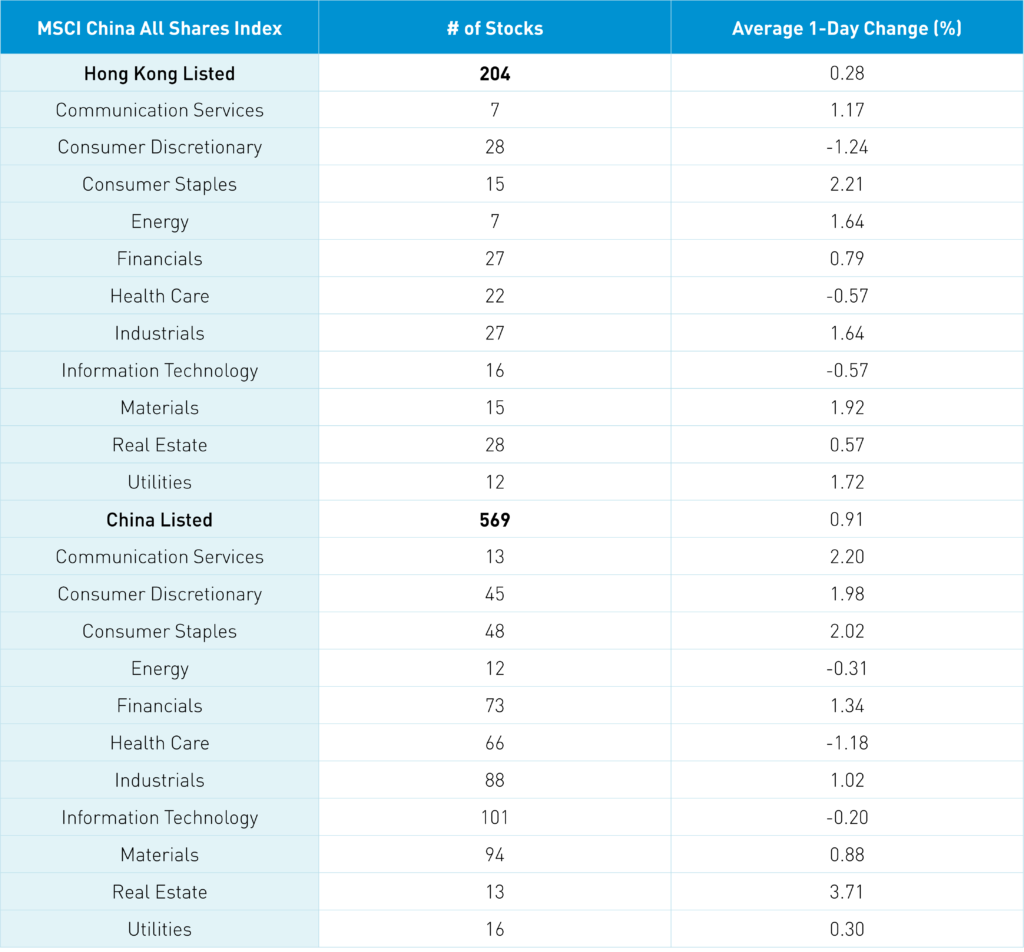

The Hang Seng Index opened -1.38%, reached an intra-day low of -1.99% though grinded higher all day to close +0.19%. Volumes were very light -7.65% from yesterday which is only 63% of the 1-year average as China and Hong Kong have a market holiday early next week. Southbound Stock Connect was closed today which usually accounts for 10% to 14% of Hong Kong turnover. Hong Kong short selling turnover was below the 1-year average. There were 265 advancers versus 213 decliners as value factors outperformed growth factors. Staples was the best performer +2.21% followed by materials +1.92% and utilities +1.73% while discretionary, tech and healthcare were off. The Hang Seng Tech was off -0.74% though Hong Kong internet stocks were not down as much as their US ADRs were yesterday. Tencent bought 807k shares overnight for the sixth consecutive day.

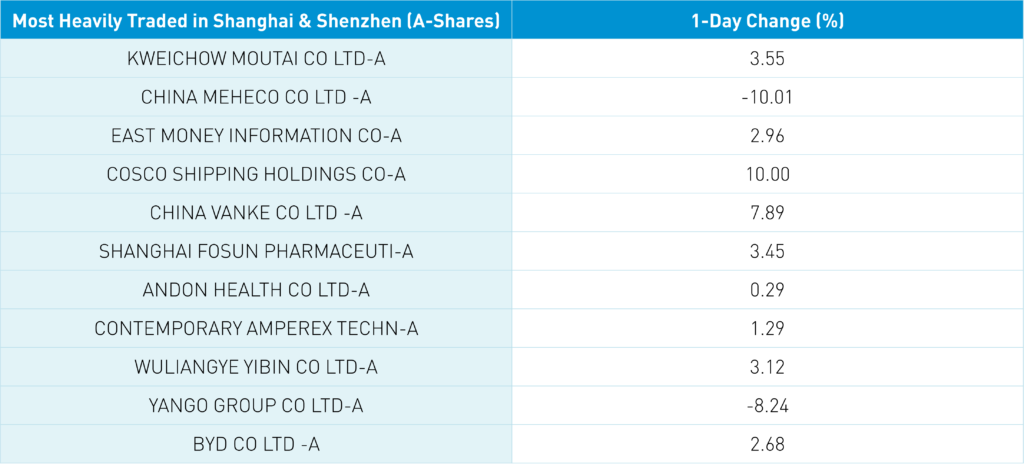

Shanghai, Shenzhen and STAR Board diverged +0.94%, +0.47% and -0.17% on volume -7.36% from yesterday which is 88% of the 1-year average. Large caps, which tend to have a value bias, outperformed today as real estate gained +3.7% while healthcare, tech and energy were off. There were 1,766 advancing stocks versus 2,567 decliners. Foreign investors bought $694mm of Mainland stocks today via Northbound Stock Connect. Treasury bonds rallied, CNY was off versus the US $ and copper -0.23%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.36 versus 6.34 yesterday

- CNY/EUR 7.03 versus 7.04 yesterday

- Yield on 10-Year Government Bond 2.77% versus 2.79% yesterday

- Yield on 10-Year China Development Bank Bond 3.02% versus 3.04% yesterday

- Copper Price -0.23% overnight