Algorithm Angst, Value Outperforms Growth, Week in Review

3 Min. Read Time

Week in Review

- Asian equities saw another choppy week of trading as earnings season wrapped, and investors assessed the risks presented by covid lockdowns in China. However, Mainland China markets were closed on Monday and Tuesday, and Hong Kong was closed on Tuesday.

- The China Securities Regulatory Commission (CSRC), China’s primary securities regulator, proposed a rule change on Monday that would allow for audit inspections by foreign regulatory agencies, removing a major hurdle for US-listed Chinese companies in complying with the Holding Foreign Companies Accountable Act (HFCAA).

- The US Federal Reserve’s indication that it may speed up its rate hike schedule weighed on equity performance in Asia and the US this week.

- The March Caixin Services PMI came in at 42 on Wednesday, well below expectations of nearly 50, indicating a contraction month-over-month. Covid lockdowns likely played a role in the disappointing release, which underscores, yet again, how important raising domestic consumption will be in achieving the government’s 2022 GDP growth target of 5.5%.

- In our latest video, cultural analyst Xiabing Su outlines the government meetings planned for 2022, an important political year for China, and their objectives.

Friday’s Key News

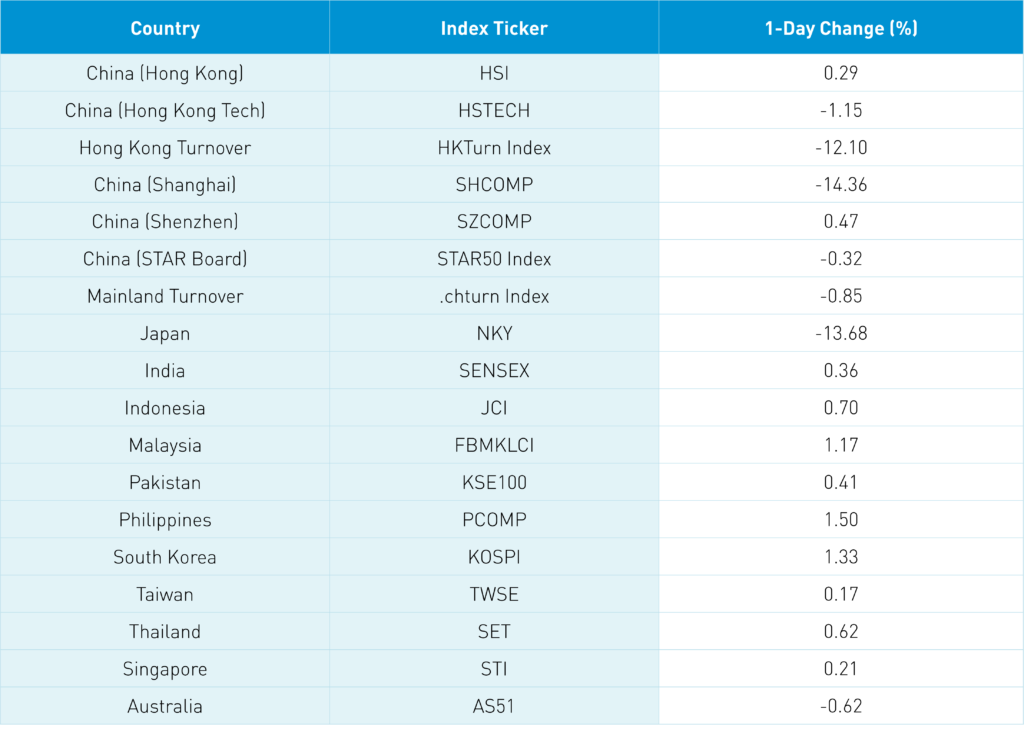

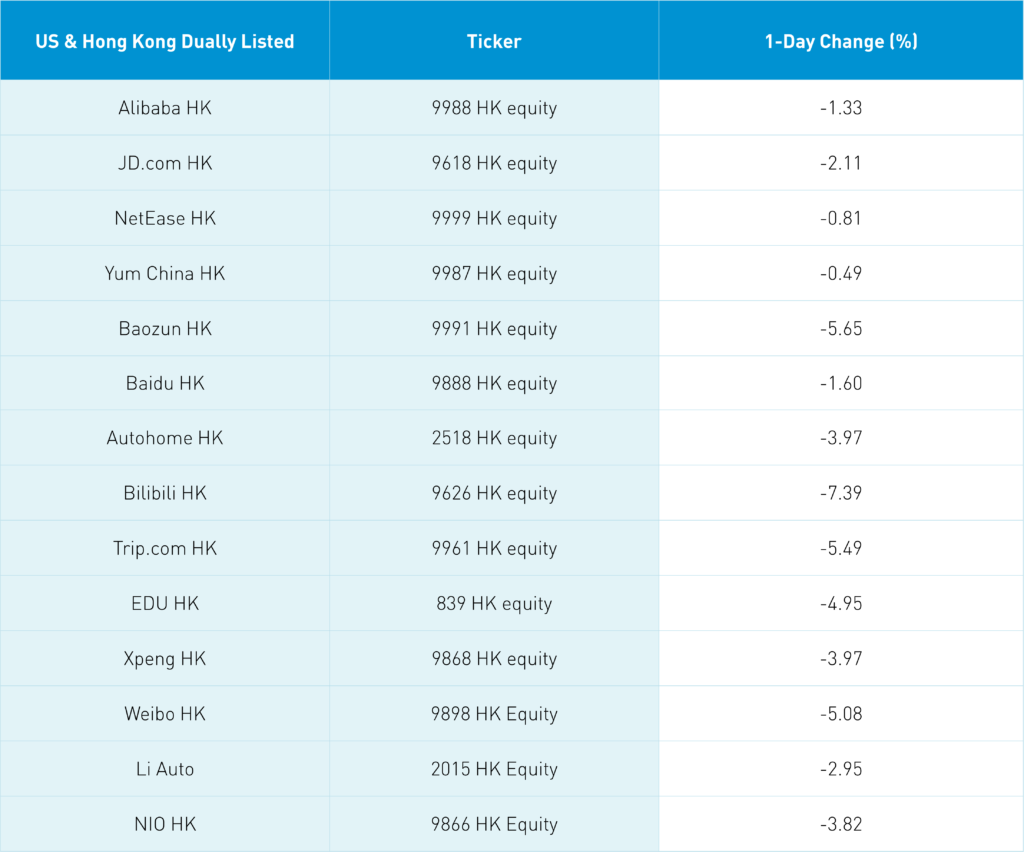

Asian equity markets enjoyed a mild rebound overnight on light volumes as the Philippines outperformed, gaining +1.33%. Value stocks and sectors were performance leaders in Hong Kong and Mainland China overnight. Hong Kong-listed internet stocks fell again, but not nearly as far as their US-listed counterparts fell yesterday.

Volumes in US-listed China internet stocks (ADRs) were LIGHT yesterday as three developments gave buyers pause: Tencent shutting down its e-sports unit, the Cyberspace Administration of China (CAC) releasing a notice on algorithm governance, and Nancy Pelosi’s proposed trip to Taiwan, which was subsequently “postponed.” These are not necessarily negative, though they are decidedly not the Vince Lombardi motivational speech that investors have been waiting for. We need positive catalysts to draw buyers back into the market. One could argue investors are looking at all things China through a microscope.

Today’s Wall Street Journal article on China tech includes a quote from a large asset manager’s Asia strategist. The strategist said he needs “clarity around regulations” before coming back into the names. 100%!

We are eight days away from the end of the comment period for the CSRC’s proposed rule change to allow the PCAOB to perform onsite audit inspections. The change would, in theory, pave the way for US-listed Chinese companies to comply with the Holding Foreign Companies Accountable Act (HFCAA). Fingers crossed that this issue gets put to bed!

Chatter around supportive economic policies is picking up. Another bank reserve requirement ratio (RRR) cut is the leading candidate. The RRR represents the amount of deposits (i.e. cash) that banks need to keep on the books rather than lend out.

The difficult covid situation in Shanghai was also a factor in today’s price action. However, it is important to remember that China’s geography is similar to its economy (i.e. BIG!). I don’t mean to downplay the importance of Shanghai to the economy, but its population represents less than 2% of China’s total population. Yes, as a percentage of GDP, Shanghai is significantly bigger.

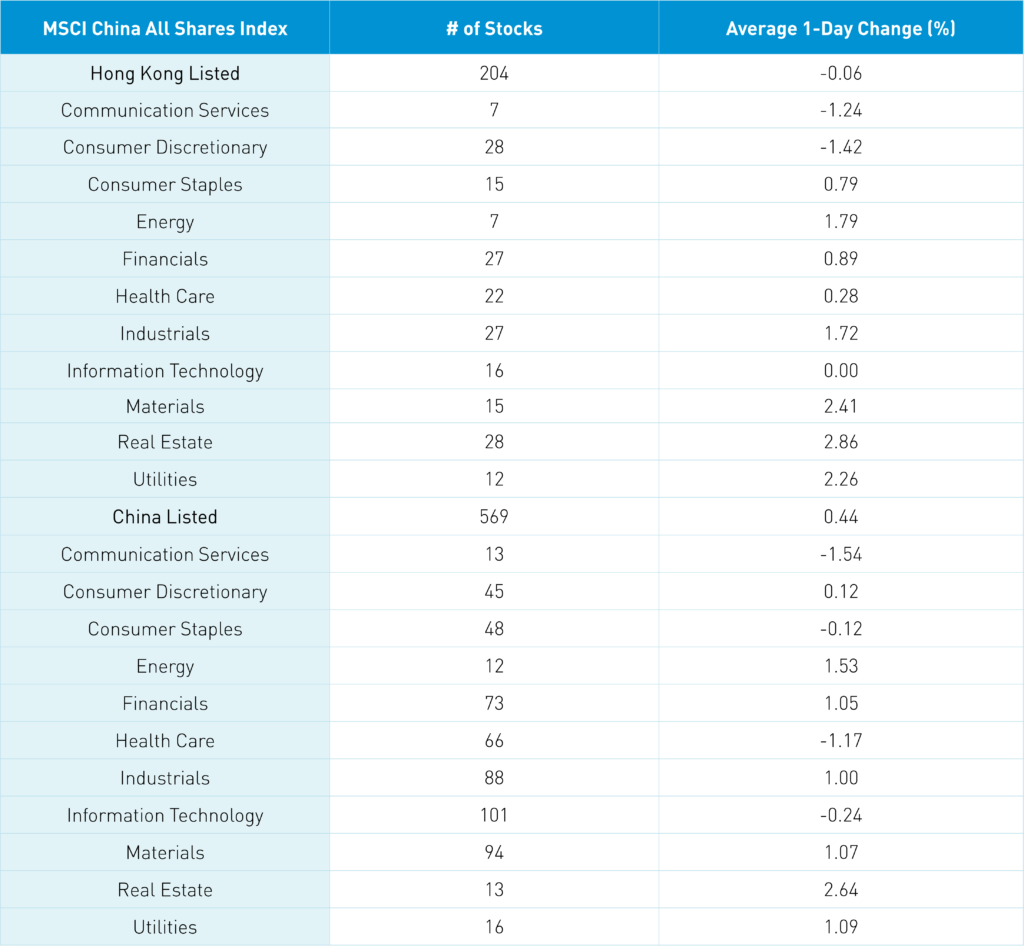

Real estate was the best performing sector in Mainland China overnight, gaining +2.59% on the Mainland and +2.85% in Hong Kong. Investors appear to be anticipating supportive policies for the sector. We’ve seen this already, but so far only at the margin. I find it entertaining that the “China’s Lehman moment” sector has started to perform well so soon. Year-to-date (YTD), real estate equities are up +13% and +5% in Mainland China and Hong Kong, respectively. However, real estate bonds are still down significantly YTD.

The Hang Seng Index gained +0.29%, while the Hang Seng TECH Index was off -1.15% on volume that was -12% lower than yesterday, which is only 70% of the 1-year average. Breadth was positive as advancers outpaced decliners by 2 to 1. Short sale volume was off -14% from yesterday, 85% of the 1-year average. Value sectors outperformed, led by real estate, which gained +2.85%, materials, which gained +2.4%, utilities, which gained +2.24%, energy, which gained +1.77%, and industrials, which gained +1.70%. Meanwhile, tech was down -0.01%, the communication services sector was down -1.26%, and consumer discretionary was down -1.44%. Energy giant CNOOC gained +2.64%, which sums up overnight trading. Mainland investors were net buyers of Hong Kong stocks via Southbound Stock Connect, while Tencent saw a light outflow for the 4th day in a row while Meituan saw net buying for the 6th day in a row.

Shanghai, Shenzhen, and the STAR Board diverged to close +0.47%, -0.32%, and -0.85%, respectively, as value outpaced growth and large caps outperformed small and mid-caps. Volume was -13% lower than yesterday, 87% of the 1-year average, while decliners outpaced advancers by 2 to 1. Like Hong Kong, real estate, energy, utilities, materials, and financials all outpaced growth sectors, including communication services, which fell -1.58%, healthcare, which fell -1.21%, and tech, which fell -1.21%. Foreign investors trimmed their Mainland holdings by -$98 million via Northbound Stock Connect. Chinese Treasury bonds sold off, CNY was unchanged versus the US dollar, and copper was off -0.05%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.36 versus 6.36 yesterday

- CNY/EUR 6.91 versus 6.93 yesterday

- Yield on 1-Day Government Bond 1.64% versus 1.64% yesterday

- Yield on 10-Year Government Bond 2.75% versus 2.74% yesterday

- Yield on 10-Year China Development Bank Bond 3.00% versus 2.99% yesterday

- Copper Price -0.05% overnight