Game On as Approvals Lead Internet Names Higher

3 Min. Read Time

Key News

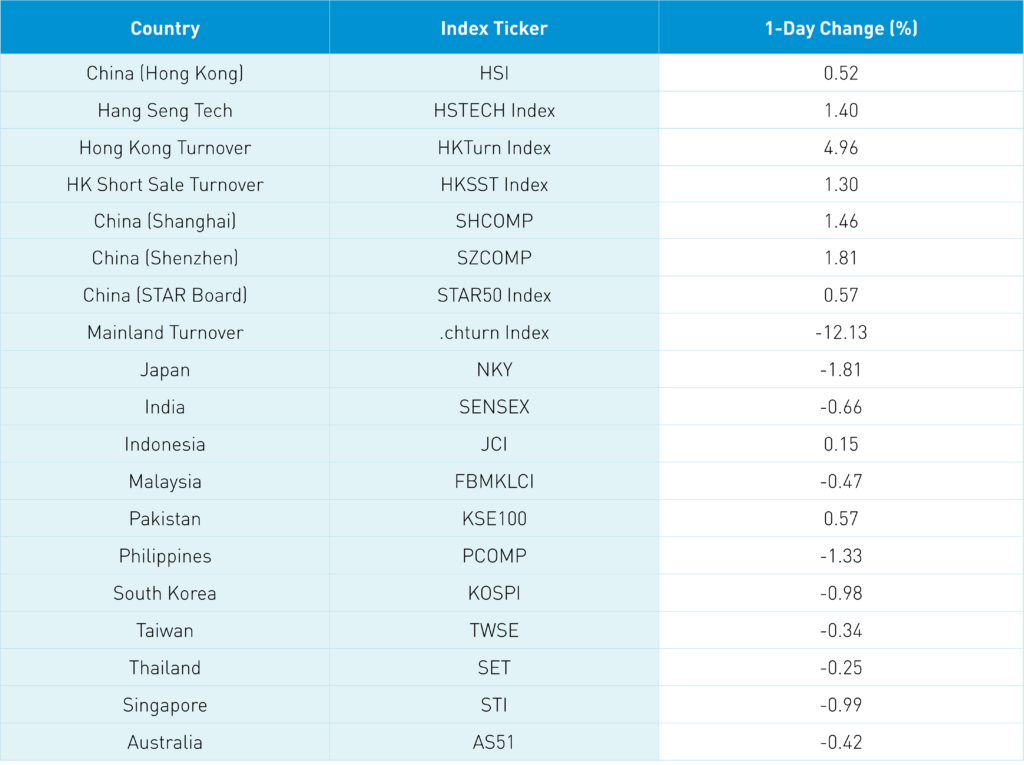

Asian equities were a sea of red, excluding China and Hong Kong, as growth sectors/stocks rebounded/outperformed relative to value sectors/stocks. Both China and Hong Kong had choppy sessions with a late-day rally led by the chatter of China's National Team buying the dip and could also add inflows from foreign investors to the tune of $1.434B via Northbound Stock Connect. The National Team is the term given to China's government-related pension funds, sovereign wealth funds, and other strategic pools of capital.

The skeptic will say this is market intervention. However, central bank interventions in the US (i.e., Fed balance sheet) and Japan (BoJ ownership of ETFs and bonds is simply staggering though they receive shockingly little attention) have become commonplace. One could also argue that these are asset allocators who buy stocks when they are low, like US pension funds rebalancing between stocks and bonds at month-end. All in the eye of the beholder though the truth is likely somewhere in-between.

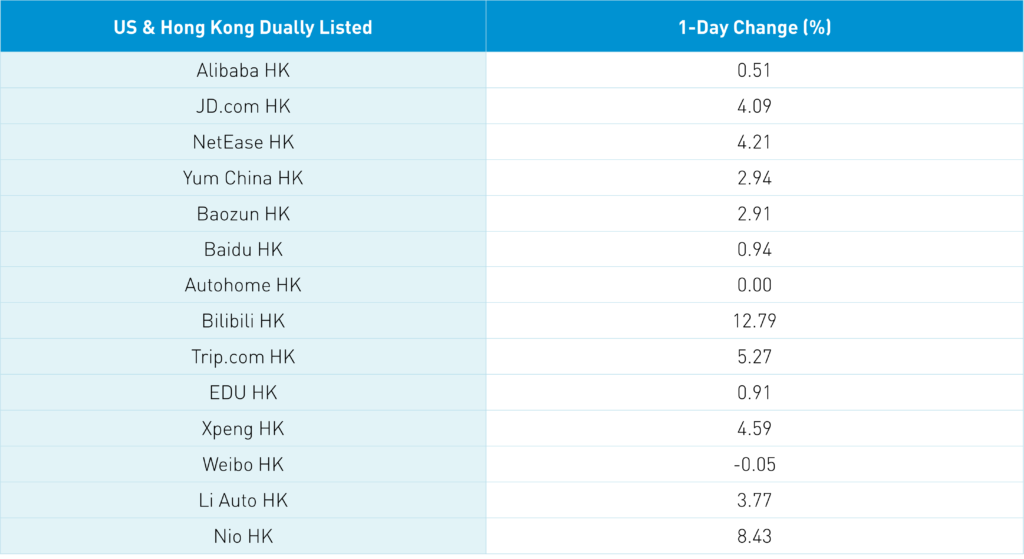

Despite China's covid outbreak and its effect on the global economy, which lower commodity prices reflect, there were also several positive catalysts. Shanghai has outlined a path for lockdowns to be dialed back based on neighborhood testing in a positive sign. After the China/Hong Kong close, the National Press and Publication Administration approved forty-five new games leading to a strong return for US-related ADRs. Investors take the move as a sign of the gaming regulatory cycle ending. Tencent, NetEase, and Bilibili didn't have games on the list but rose on the broader positive sentiment toward the sector. We also had better than expected March new loan and financing data also released after yesterday's Hong Kong/China close. There is also the anticipation that the policy support needs to be applied sooner rather than later. The Ministry of Commerce and Ministry of Transportation stated they would work to ensure freight and logistics were kept running in areas of the outbreak. We would like to have seen today's market action accompanied by solid volumes though we'll take it!

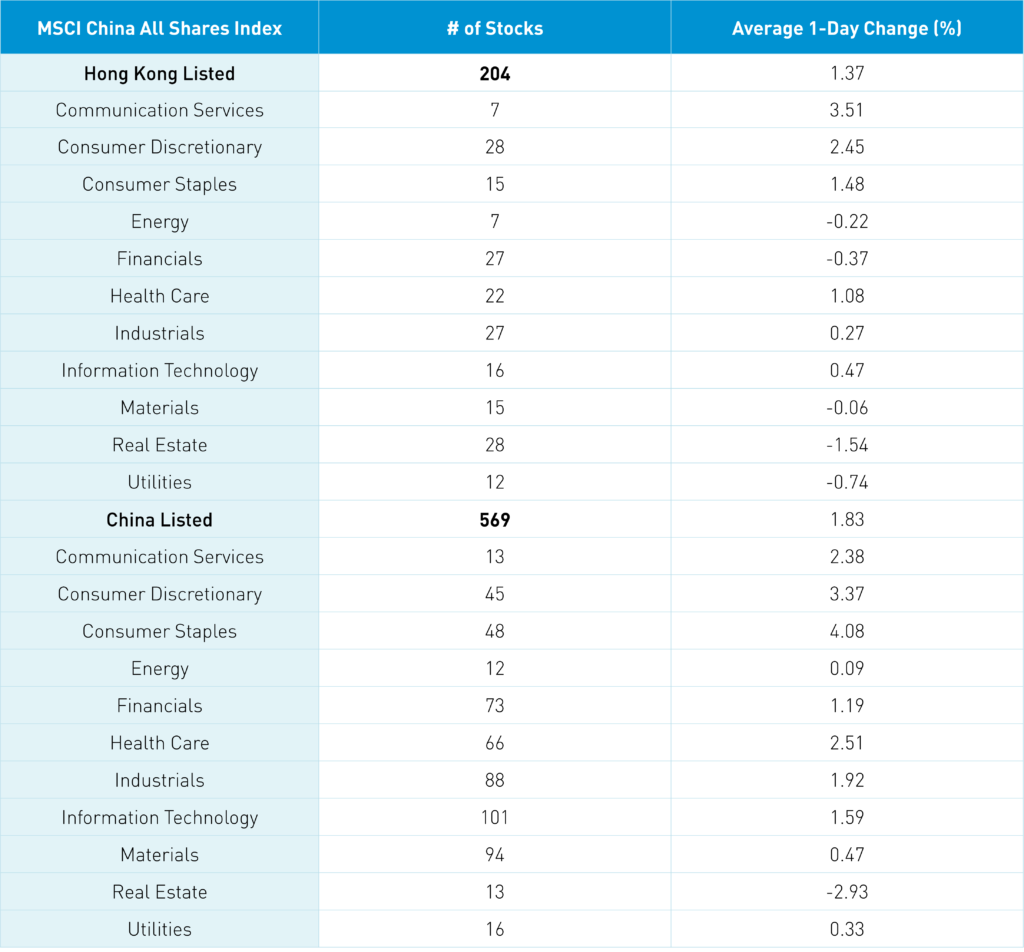

The Hang Seng Index gained +0.45% though the Hang Seng Tech +1.4% on volume +4.95% from yesterday, which is 88% of the 1-year average. Advancers outpaced decliners 254 to 218 while short sale volume rose to 114% of the 1-year average. Hong Kong internet names had a strong day excluding Kuaishou on yesterday's data announcement from the State Council. Tencent and Kuiashou were a small net outflow from Mainland investors via Southbound Stock Connect though Meituan had another net buy day in an aggregate net buying day. Growth sectors outperformed, led by communication, discretionary, staples, healthcare, and tech, while value sectors such as financials, energy, materials, and utilities underperformed.

Shanghai, Shenzhen, and STAR Board gained +1.46%, +1.81%, and +0.57% on volume -5.16% from yesterday, which is 86% of the 1-year average. Breadth had 3,400 advancers versus 942 decliners. Quality and, to a lesser degree, growth were key factors, while dividends and value were the worst performers. Real estate was the only down sector. Foreign investors bought a healthy $1.434B of Mainland stocks today. Treasury bonds, CNY versus the US $, and copper were all off by a small margin.

Our friend Troy asked me last week about the credibility of the US regulators who approved their US-China listings and are now tasked with potentially delisting them. The SEC is simply the enforcement agent of the HFCAA though they did allow these companies to list here knowing they couldn't adhere to PCAOB audit reviews. With that said, there wasn't any rationale for them not to allow them to list. It does bring up an interesting point on the ecosystem that profited from their listings though it bears no consequence for a potential delisting. Private equity managers and their institutional investors made a lot of money by smartly investing early and exiting via a US IPO. That IPO put US investment bankers to work who were paid generously. Law firms and accountants got paid for their work in the IPOs. Exchanges made a lot of money on listing fees.

Who will get left holding the bag on the HFCAA? Individual investors who can't convert their ADRs to the Hong Kong share class are unaware of the HFCAA or forced to sell because they can't or don't want to hold a US listing. Any ounce of idealism has been snuffed out of me helping build a business that competes against massive firms. At the same time, this is another case of US wealth inequality that is entirely preventable—ever seen an interview with a politician who voted for the HFCAA? Me neither. No one has spoken about this narrative, but hopefully, someone will. It isn't just unfair; it is unAmerican!

Last Night's Exchange Rates, Prices, & Yields

- CNY/USD 6.37 versus 6.37 yesterday

- CNY/EUR 6.93 versus 6.96 yesterday

- Yield on 10-Year Government Bond 2.77% versus 2.77% yesterday

- Yield on 10-Year China Development Bank Bond 3.01% versus 3.00% yesterday

- Copper Price -0.23% overnight