Bank RRR Cut Anticipation Lifts Markets

2 Min. Read Time

Key News

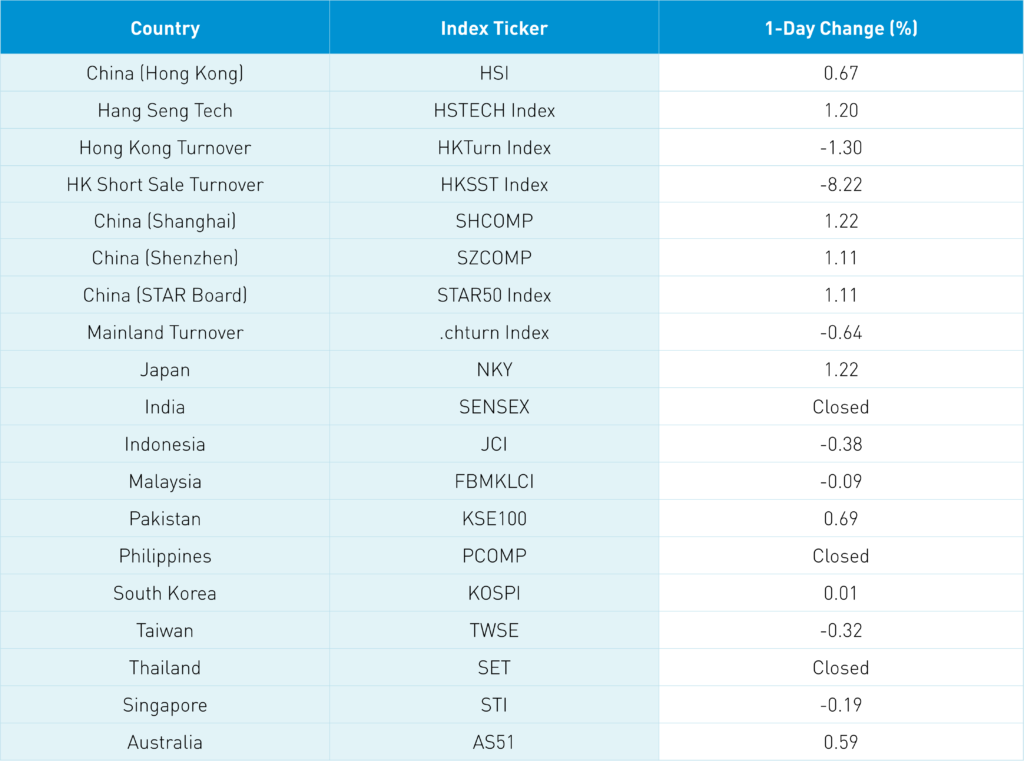

Asian equities had a mixed night, as China, Hong Kong, and Japan outperformed. At the same time, India, the Philippines, and Thailand got an early start to the long weekend ahead of tomorrow’s Good Friday holiday. Mainland media reported that 100 cities have lowered mortgage rates leading to another strong day in real estate stocks in China and Hong Kong. Real estate bonds appear skeptical of the move though its a bit of a sleeper rally and contrarian move to the Evergrande China’s Lehman narrative.

China equities rose in anticipation of the PBOC cutting the bank reserve requirement ratio (RRR), medium-term loan facility, and potentially the loan prime rate tomorrow. After Premier Li and the State Council released statements yesterday, this feels like a done deal. At a post-close press conference reviewing 1st quarter stats, reporters asked about the PBOC’s monetary policy support. Yes, this is being done as the PBOC stated “…the new downward pressure on the economy has increased” driven by covid restrictions and, to a lesser degree, global central bank policy to snuff out inflation by tightening interest rates. Exhibit A: South Korea hiked rates +0.25% overnight. Hong Kong listed internet stocks were largely higher though Alibaba HK was off -3.05% on headlines that Ant Group would be investigated after Hangzhou’s government head was arrested on bribery charges. Alibaba owns 1/3 of Ant though headlines appear worse than any economic impact.

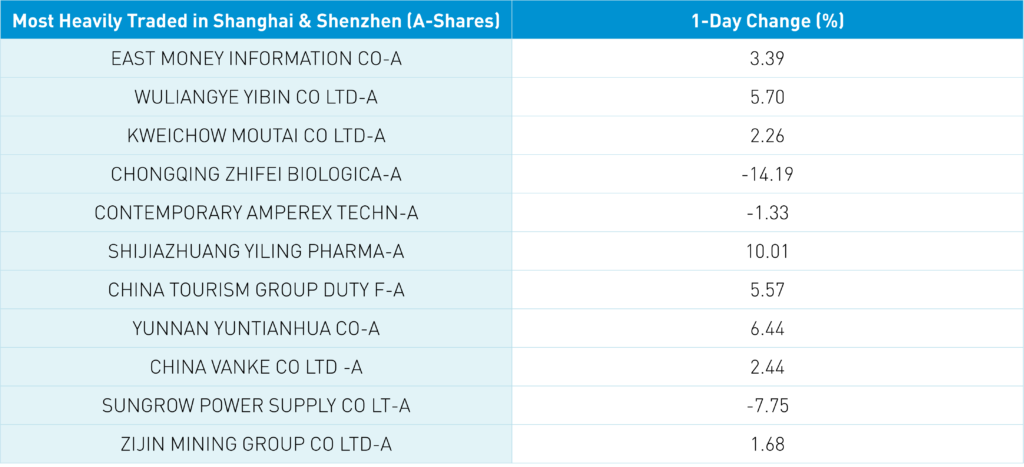

Yesterday we mentioned household appliances, autos and EVs as a focus for supportive policies. No surprise amongst today’s best performers in China, namely Midea +3.8%, Haiser +4.11%, and Gree +1.66%. Policy on raising consumption also lifted staples such as liquor stocks. If we connect the dots, shouldn’t e-commerce be outperforming as well?

I noticed this morning that JD.com’s Hong Kong listing has jumped to 50% of the value traded of its US ADR over the last twenty trading days. If Southbound Stock Connect rules are relaxed to allow secondary offerings, NetEase HK and JD.com HK would be prime candidates based on their above industry average Hong Kong volume.

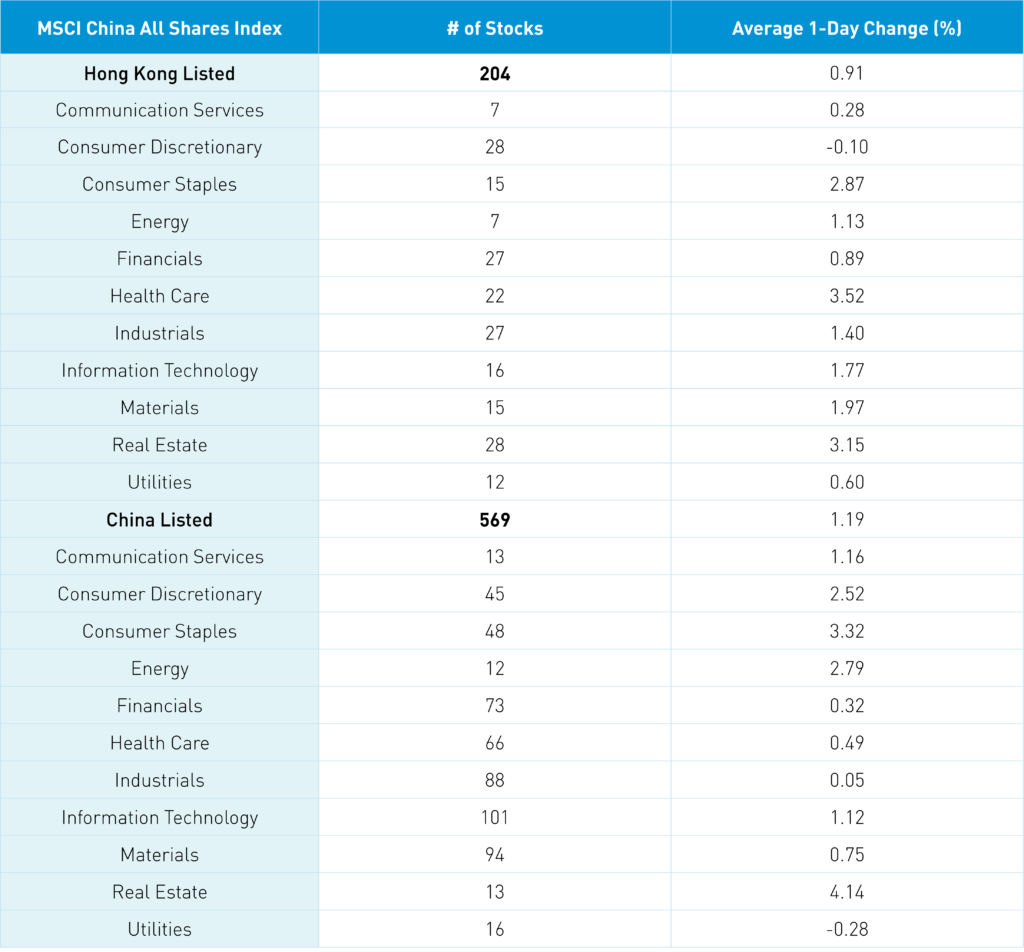

The Hang Seng Index gained +0.67% while the Hang Seng Tech +1.2% on volume -1.3% from yesterday, only 67% of the 1-year average. There were 435 advancers today versus only 48 decliners. Shorts might have covered going into the long weekend as short turnover fell -by 8% from yesterday, which is 87% of the 1-year average. The growth factor outperformed value today as all sectors were positive, less discretionary dragged down by Alibaba HK. EV ecosystem stocks had a strong day. Healthcare, real estate, and staples led the market higher, gaining +3.51%, +3.14%, and +2.86%. Tencent and Meituan saw small net buying via Southbound Stock Connect as Mainland investors were net buyers of Hong Kong stocks.

Shanghai, Shenzhen, and STAR Board gained +1.22%, +1.11%, and +1.11% on volume -0.64% from yesterday, 81% of the 1-year average. Advancers outpaced decliners 3 to 1 as quality factors had a strong day. Real estate +4.07%, staples +3.25%, energy +2.72% and discretionary +2.45% while industrials and utilities were off -0.02% and -0.35%. Northbound Stock Connect was closed today. Treasury bonds rallied, CNY was off versus the US $ by -0.05% and copper +0.03%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.37 versus 6.37 yesterday

- CNY/EUR 6.95 versus 6.90 yesterday

- Yield on 10-Year Government Bond 2.77% versus 2.76% yesterday

- Yield on 10-Year China Development Bank Bond 3.00% versus 3.00% yesterday

- Copper Price +0.03% overnight