PBOC & State Council Lift Internet and Consumption Plays

2 Min. Read Time

Key News

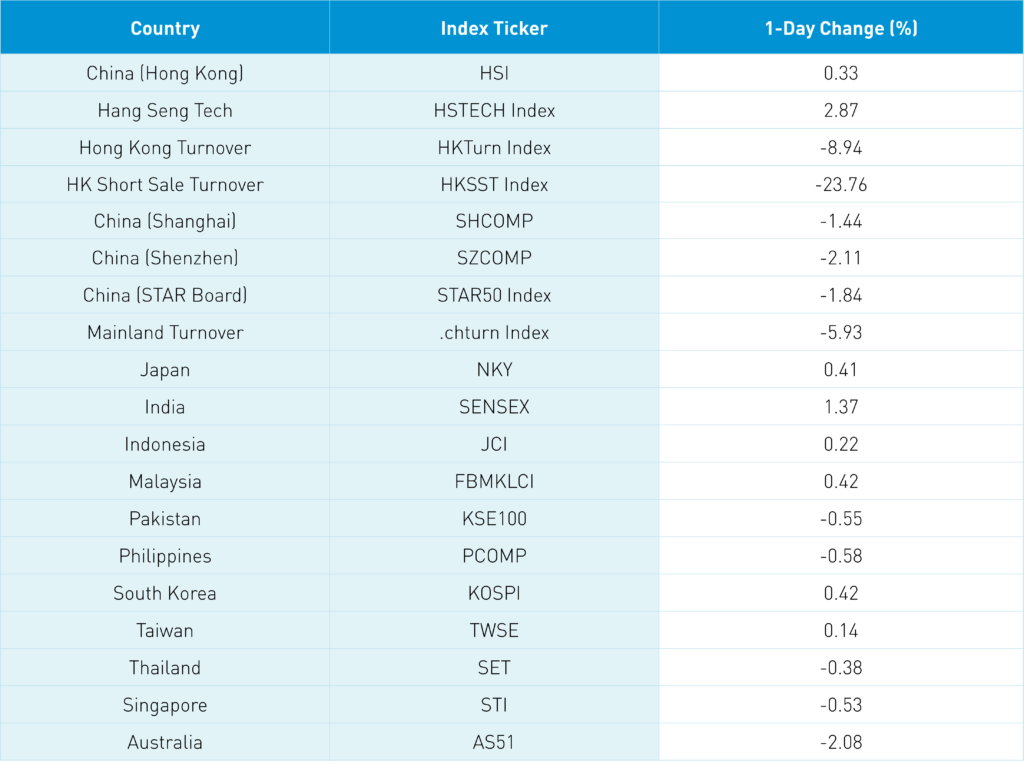

Asian equities were largely higher. Mainland China was off, and Australia returned from yesterday’s holiday off -2.08% as commodity prices retreated. Two key pieces of news drove Hong Kong higher and elements of Mainland China higher.

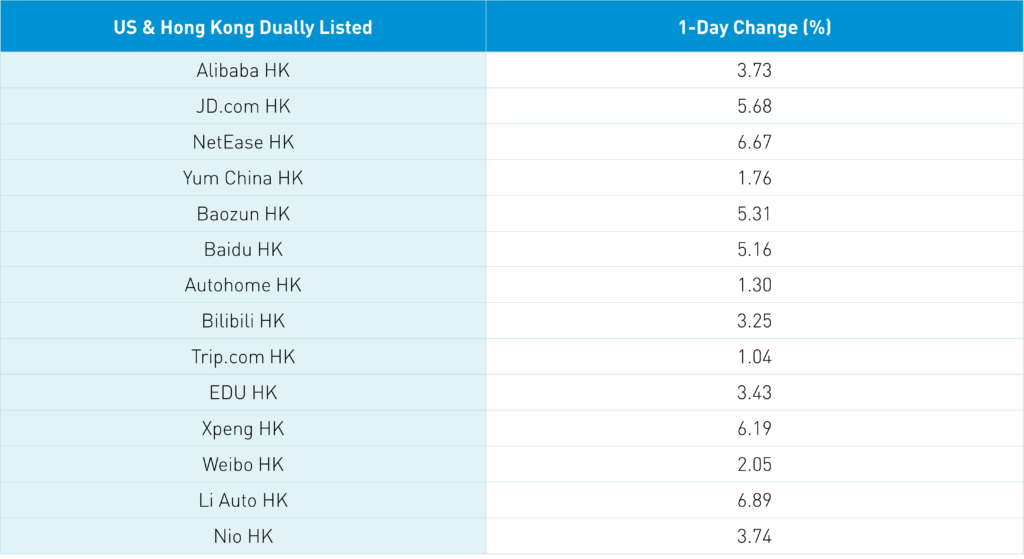

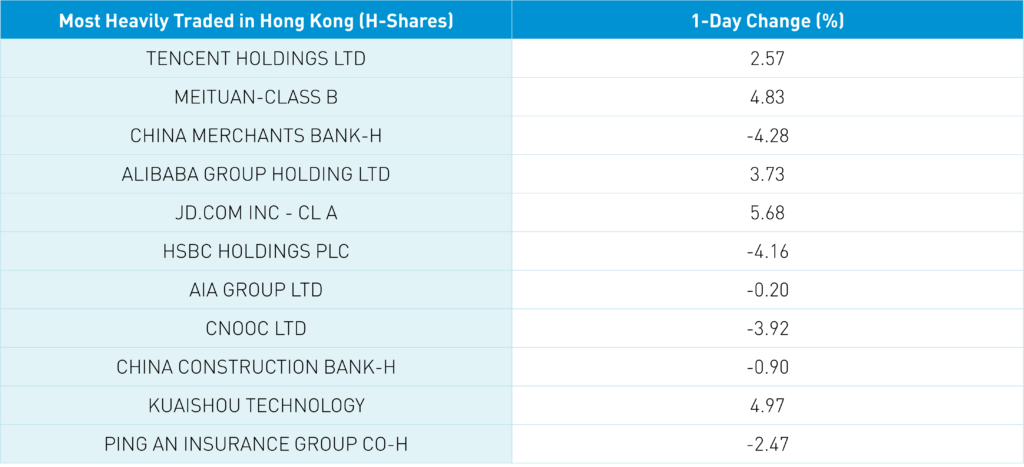

The PBOC stated, “To advance the healthy development of the platform economy, the rectification work of large platform companies will be steadily promoted.” The platform economy references large internet stocks that sent the Hang Seng Tech Index +2.87% as internet stocks had a strong day as Tencent +2.57%, Meituan +4.83%, Alibaba HK +3.73%, JD.com HK +5.68%, and Kuaishou +4.97%.

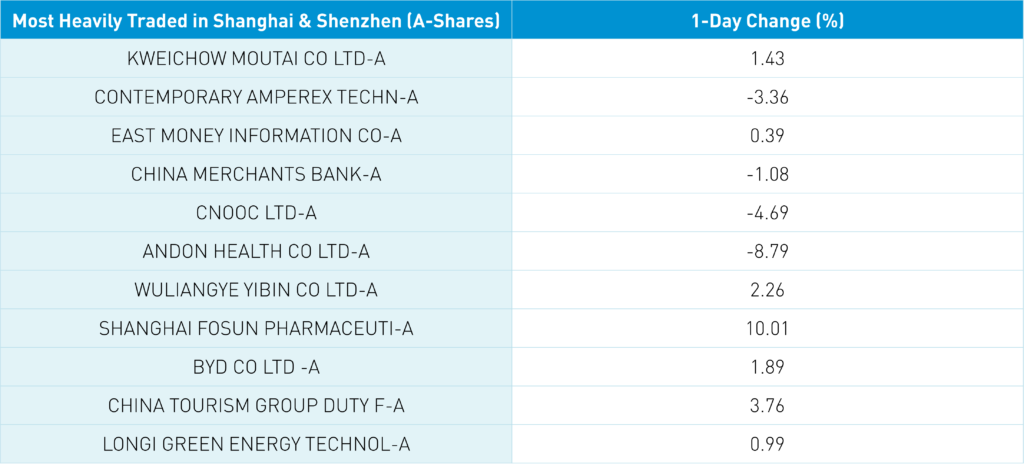

The State Council, which is similar to Biden’s cabinet, named 20 policies to promote consumption, noting that consumer spending accounted for nearly 70% of China’s GDP in Q1. Many internet companies are consumer-oriented, as nearly 1/3 of China retail sales online. The State Council statement lifted the Mainland staples sector +1.39%, led by liquor giant Kweichow Moutai +1.43%, and competitor Wuliangye Yibin +2.26%. There was also talk of policy support for real estate developers as the Hong Kong and China real estate sectors rose +1.02% and +1.14%. Hang Seng, Hang Seng Tech, Shanghai, and Shenzhen were off their intra-day highs of +1.96%, +1.54%, -0.29%, and -0.01% as traders took intra-day gains. Growth sectors outperformed value sectors today. We would like to have seen volumes higher on a rebound day. We still have mass testing in Beijing with 21 confirmed Covid cases, while Shanghai remains in lockdown. Ironically value sectors were pulled down by weakening commodity prices due to China’s lockdown. CNY rebounded versus the US $ +0.25% following the PBOC FX reserve moves overnight.

I noticed that China’s FDA approved a covid-19 vaccine after the close on a Chinese media website. I’ll look into this as a strong Covid vaccine would allow the government to move away from its lockdown/quarantine policy.

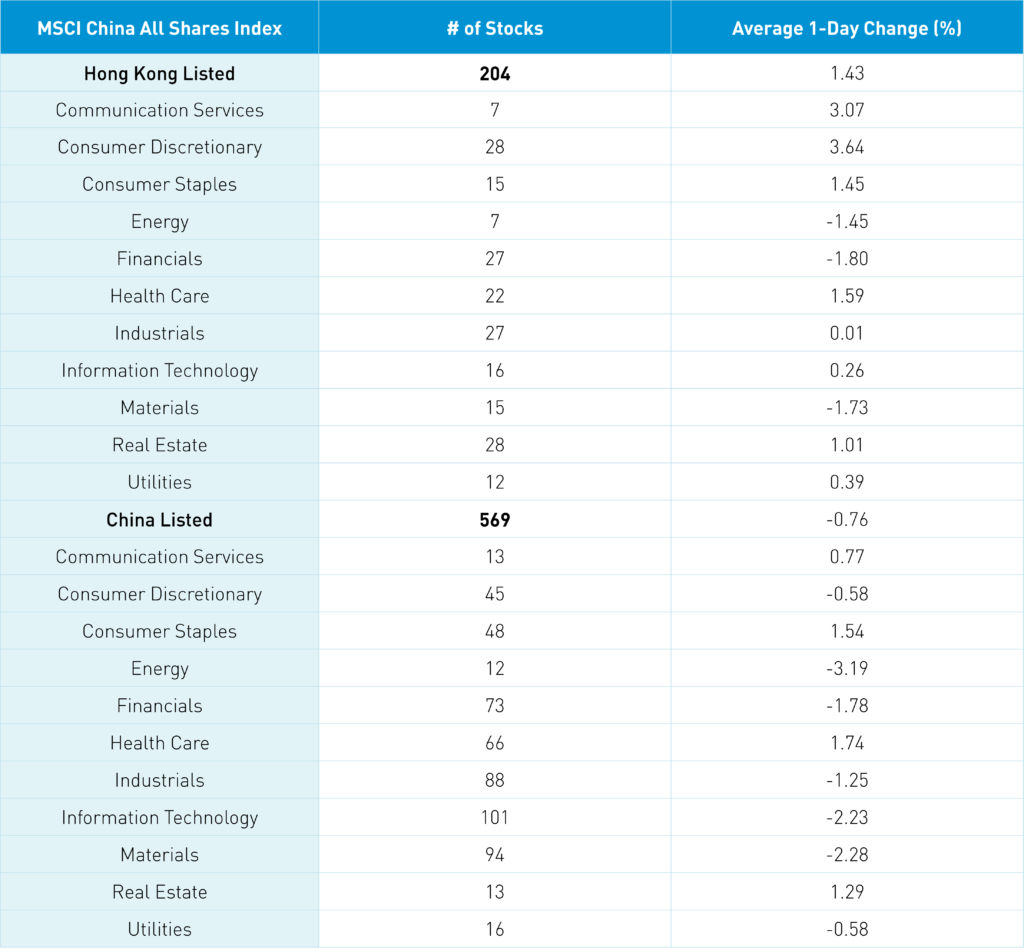

The Hang Seng Index and Hang Seng Tech Index gained +0.33% and +2.87% on volume off -8% from yesterday, 84% of the 1-year average. There were 247 advancers and 224 decliners. Hong Kong short sale volume declined by -23% from yesterday, which is a hair above the 1-year average. Growth stocks led the way as Hong Kong internet posted a strong day as discretionary +3.66%, communication +3.08%, and healthcare +1.61%, while financials -1.79%, materials -1.71%, and energy -1.43%. Mainland investors were a minimal net buy of Hong Kong stocks via Southbound Stock Connect as Tencent was a small net sell while Meituan and Kuaishou were net buys.

Shanghai, Shenzhen, and STAR Board closed -1.44%, -2.11%, and -1.84% on volume -5.93% from yesterday, which is 77% of the 1-year average. There were 950 advancing stocks and 3,461 declining stocks. Large companies and quality factors outperformed today as healthcare +1.64%, staples +1.44% and real estate +1.18% while energy -3.3%, materials -2.39% and tech -2.33%. Consumption plays had a strong day while semis were weak. Foreign investors bought +$235mm of Mainland stocks today via Northbound Stock Connect. Treasury bonds were off slightly, CNY rebounded versus the US $ +0.25%, and copper hit -1.27%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.54 versus 6.57 yesterday

- CNY/EUR 6.99 versus 7.05 yesterday

- Yield on 10-Year Government Bond 2.83% versus 2.82% yesterday

- Yield on 10-Year China Development Bank Bond 3.05% versus 3.05% yesterday

- Copper Price -1.27%