Mainland China Gains On Reopen, Economic Daily Editorial Marks Shift In Regulatory Tone

2 Min. Read Time

Key News

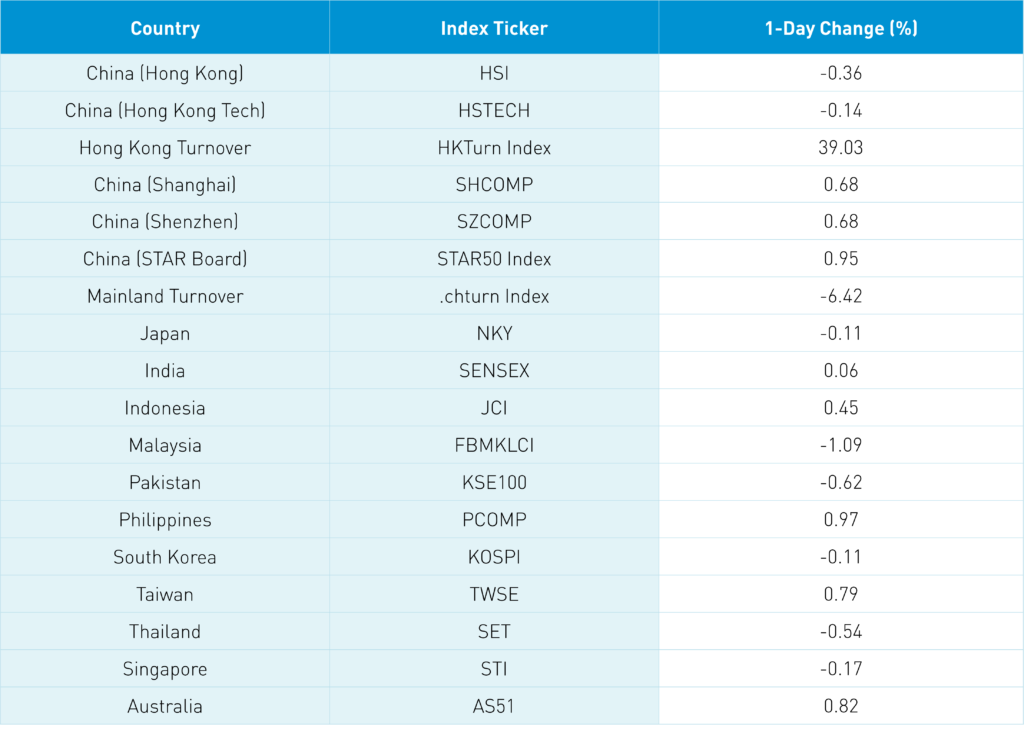

Asian equities were mixed though mostly lower overnight, failing to follow US equities higher, as Hong Kong underperformed. Mainland China markets reopened to outperformance.

An editorial published by the Economic Daily, a Mainland media source, noted new draft policies set to support innovation and sustainable development among internet platforms and the end of the previous regulatory cycle, which focused on addressing excesses and abuse in the industry. A government-sponsored symposium held over the long weekend was meant to reassure technology CEOs of the government's support for their businesses. Internet stocks were mostly flat in Hong Kong overnight.

The political bureau of the CPC Central Committee occurred on April 29th. Key takeaways were the government's focus on structural issues in areas that have been in market news of late, especially real estate, and on the 5.5% GDP growth target, which will require a rebound in consumer spending to achieve.

Online real estate platform KE Holdings has filed for a Hong Kong listing, the latest US-listed Chinese company to do so. While we believe that a solution to the Holding Foreign Companies Accountable Act (HFCAA) could be close at hand, clearly companies still see listing in Hong Kong as a worthwhile undertaking. This is good news for institutional investors who can convert their US shares to Hong Kong.

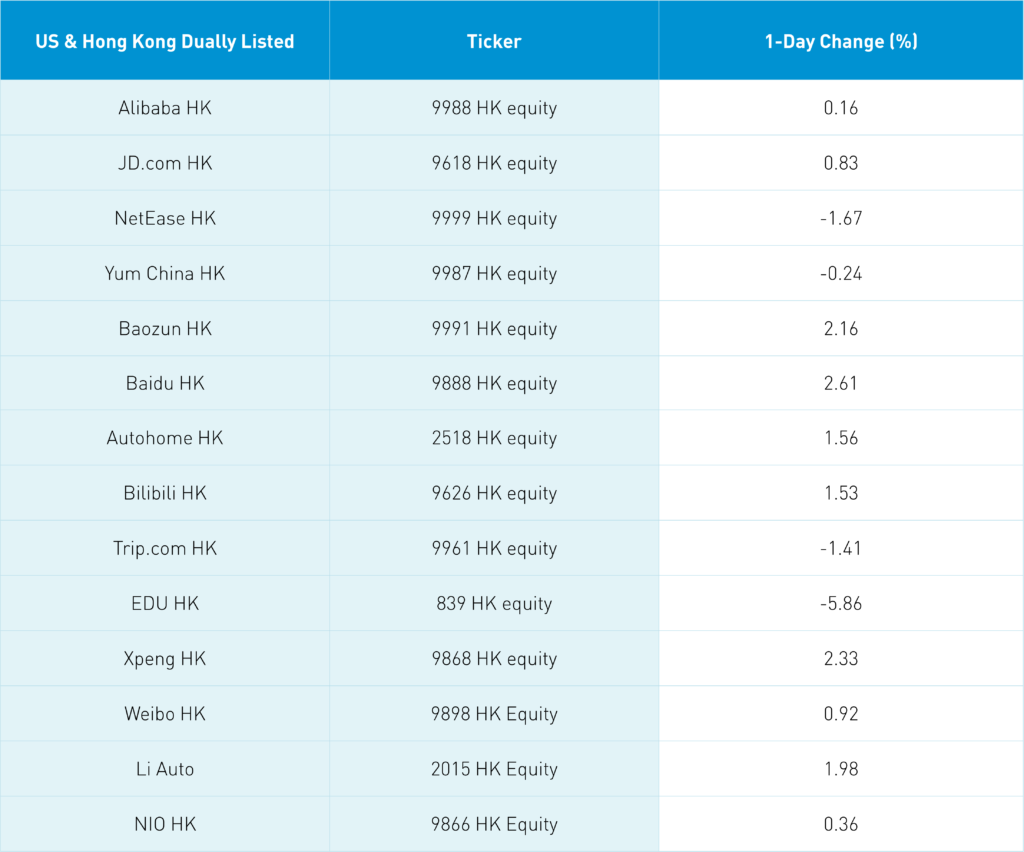

In other delisting news, the SEC has now added over 80 companies to the list of firms that could potentially face delisting. We knew this was coming and, as such, it should surprise no one. The list now includes JD.com and Bilibili, which is what is driving the downdraft in their US shares today.

The Markit/Caixin services PMI was released overnight, indicating a contraction year-over-year and coming in just below analyst estimates. PMIs are diffusion indexes, meaning that readings below 50 indicate contraction and readings above 50 indicate expansion. This is one of the worst readings for the services PMI in years and is directly due to covid-19 lockdowns. Fortunately, we should see these lockdowns abate soon as mRNA vaccines are distributed in China, though it is difficult to say when.

Oil and gas stocks were higher following another rise in commodity prices. Meanwhile, China real estate developers were hit after seeing a comeback over the past few weeks.

The Hang Seng Index and Hang Seng TECH Index both closed lower at -0.36% and -0.14%, respectively, on volume that was +39% higher than yesterday as Southbound Stock Connect reopened. Most sectors in Hong Kong were slightly lower on the day though industrials and utilities saw slight gains as value factors outpaced growth factors.

Shanghai, Shenzhen, and the STAR Board closed +0.68%, +0.68%, and +0.95%, respectively, on volume that was -6% lower than the last session. As in Hong Kong, value factors outpaced growth.

Last Night's Exchange Rates, Prices, & Yields

- CNY/USD 6.65 versus 6.61 yesterday

- CNY/EUR 6.99 versus 6.98 yesterday

- Yield on 1-Day Government Bond 1.44% versus 1.59% on April 29th

- Yield on 10-Year Government Bond 2.83% versus 2.84% on April 29th

- Yield on 10-Year China Development Bank Bond 3.05% versus 3.07% on April 29th

- Copper Price -1.37% overnight