Tencent’s Q1 Misses the Mark, Dr. Kissinger Talk Notes

3 Min. Read Time

Key News

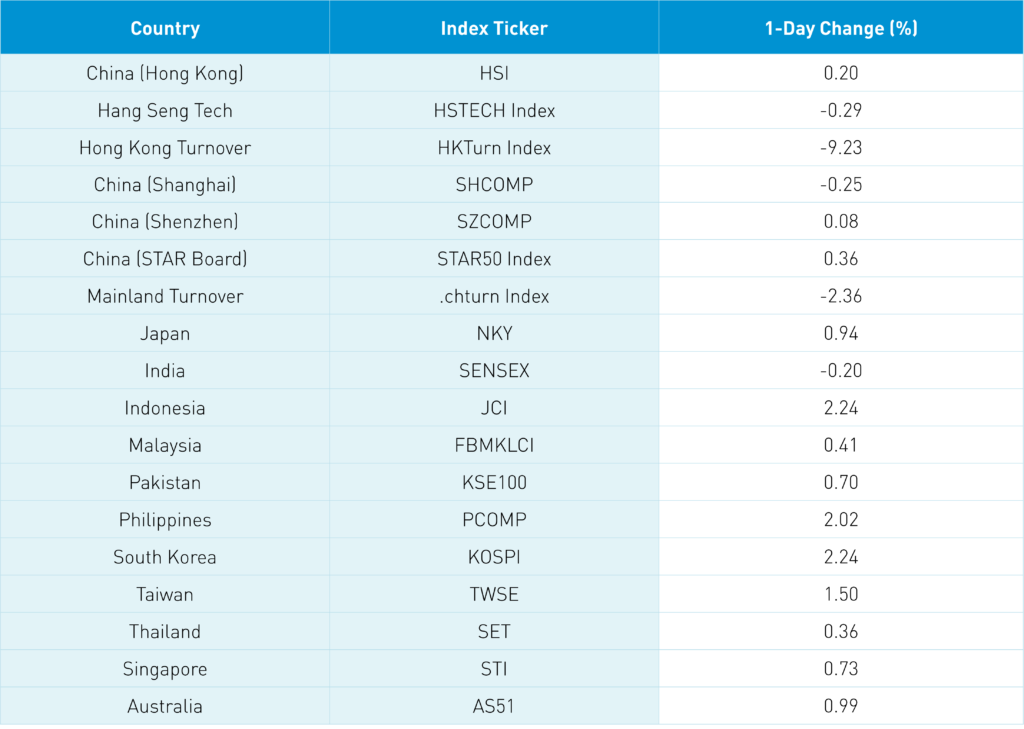

Asian equities followed US stocks higher on light volumes as China and India posted small losses.

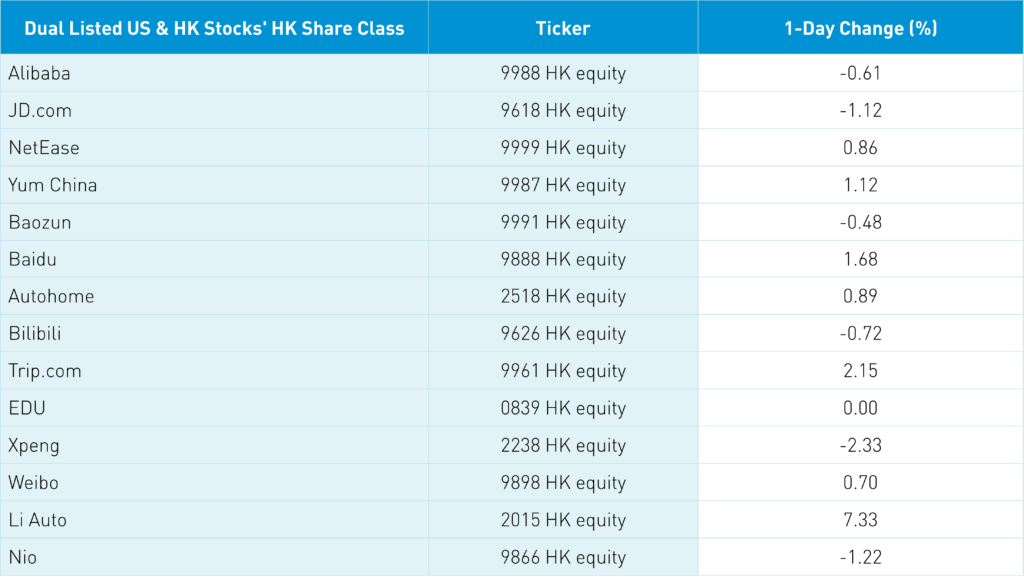

Hong Kong internet stocks were off despite good results from JD.com yesterday and Vice Premier Liu He’s attendance at the CPPCC meeting with internet companies. JD’s Q2 outlook due to Shanghai's lockdown likely weighed on sentiment.

Mainland media noted that this evening Premier Li reiterated support for the “platform economy” and foreign listings similar to what we heard coming out of the CPPCC. Volumes were light overnight as investors waited for Tencent’s post-Hong Kong close earnings release discussed below.

Mainland real estate stocks were off on light sales numbers. Candidly, it was a fairly light night in terms of both news and volumes as investors appear to be focused on the implementation of economic support measures and China’s covid policy. There was a report on the fall in tax receipts due to tax credits to support businesses in a sign of support.

Yesterday, my colleague Henry and I had the chance to hear Dr. Henry Kissinger speak via video at an event followed by a panel discussion that I participated in. It is amazing that Dr. Kissinger will turn 99 next week and can still provide great insights. Dr. Kissinger sees China moving away from its “without limits” cooperation with Russia statement due to the West’s sanctions on Russia post-invasion. Russia and Putin assumed an easy win in Ukraine that hasn’t occurred due to the heroic efforts of the Ukrainian people. He stated that China will not disenfranchise Europe due to the substantial trade between the two regions. Dr. Kissinger also stated his disappointment at the continuing lack of dialogue between the US and China, which he felt was problematic for resolving differences.

Tencent’s Q1 earnings missed analyst expectations across the board as revenue was flat year over year (YoY) at RMB 135.5B though lower than expectations of RMB 141.06B. Net profit declined to RMB 23.7B from Q1 2021’s RMB 47.8B which is a decline of -51% YoY while diluted EPS declined -23% to RMB 262 from RMB 3.41 YoY. In addition to increased general/administrative expenses increasing from Q1 2021’s RMB 18.967 to RMB 26.669B, online advertising revenue declined -18% YoY to RMB 18B from Q1 2021’s RMB 21.8B.

Advertisers dialed back their budgets due to decreased demand due to covid lockdowns. Gaming, which is comprised of both domestic China and international, increased slightly from Q1 2021’s RMB 72.4B to RMB 72.7B. Fintech revenue increased by +10% YoY to RMB42.8B from RMB 39B, in a sign the company has navigated regulation fine. One highlight is the RMB 188.8 billion worth of cash on the books. Another positive from the earnings call was the optimistic tone of management on gaming regulation and the technology sector.

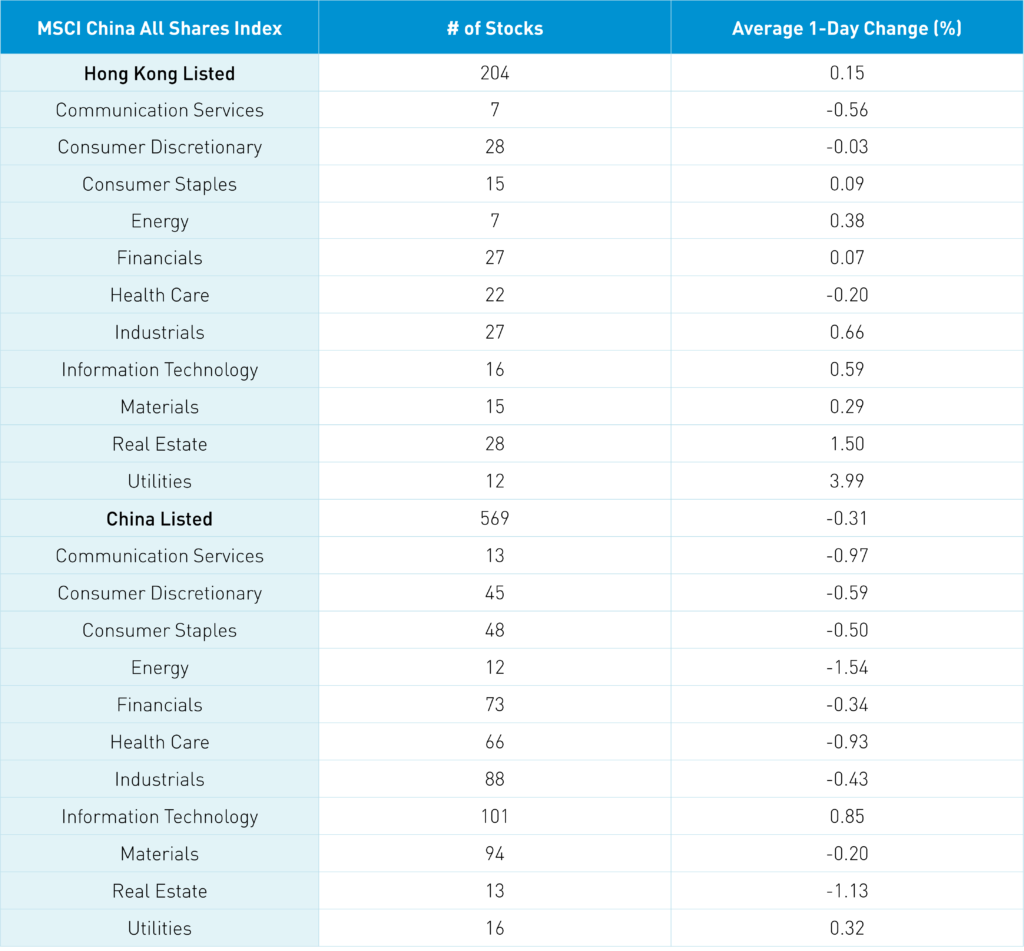

The Hang Seng and Hang Seng Tech diverged to close +0.2% and -0.29%, respectively, on volume that was down -9.23% from yesterday, which is 78% of the 1-average. There were 285 advancers and 189 decliners overnight. Hong Kong short sale volume increased slightly by +0.47%, which is 95% of the 1-year average. Large-cap and growth factors outperformed value though interesting the dividend factor did okay. Top gaining sectors were utilities +3.99%, real estate +1.49% and industrials +0.66% while declining sectors were communication -0.56%, healthcare -0.2% and discretionary -0.03%.

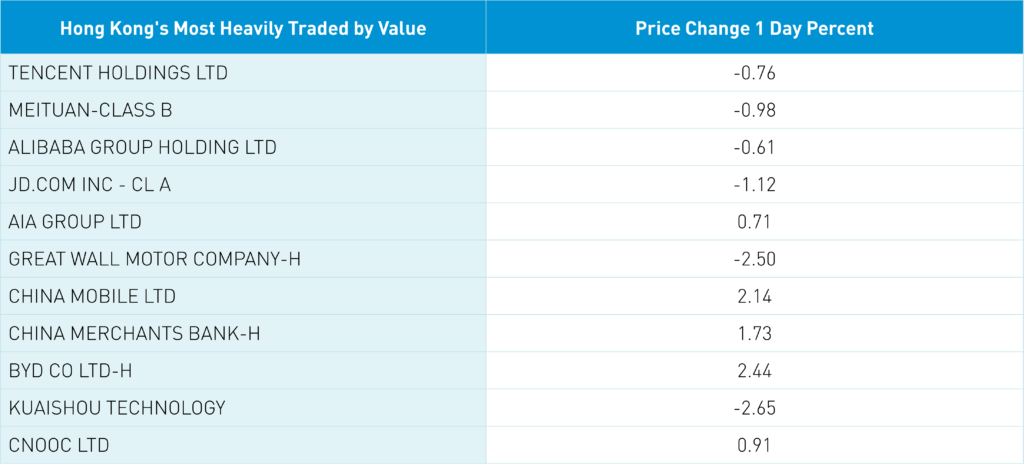

Hong Kong internet stocks dominated the most heavily traded with Tencent -0.76% which was a small net sale via Southbound Stock Connect, Meituan -0.98% which was a small net buy via Southbound Stock Connect, Alibaba HK -0.61% and JD.com HK -1.12%. Mainland investors were net buyers of Hong Kong stocks via Southbound Stock Connect.

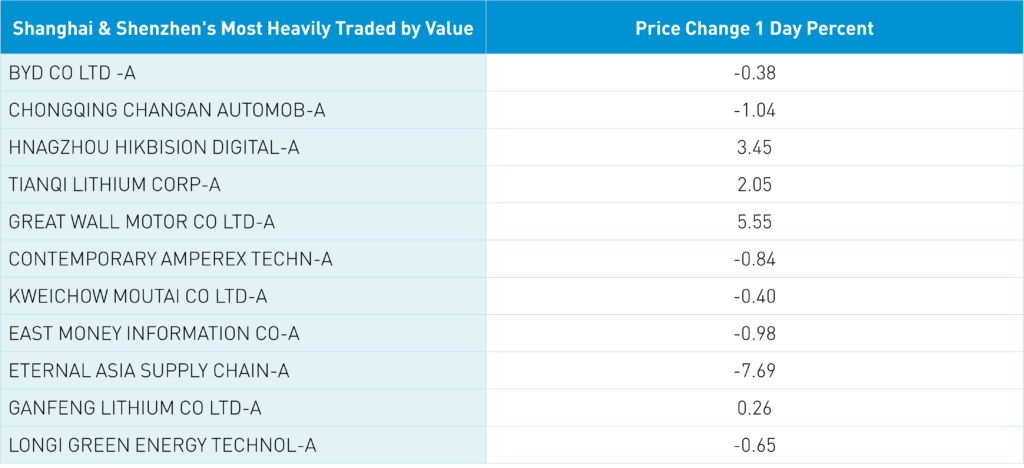

Shanghai, Shenzhen, and the STAR Board diverged to close -0.25%, +0.08%, and +0.36%, respectively, on volume that fell -2.36% from yesterday, which is 71% of the 1-year average. There were 3,131 advancing stocks and 1,231 declining stocks. Growth factors outperformed value factors while small caps outperformed lage caps. The only positive sectors in US $s were tech +0.82% and utilities +0.3% while energy -1.56%, real estate -1.16% and communication -1%. Solar and wind sub-sectors outperformed while coal mining was down. Foreign investors sold -$337mm of mainland stocks via Northbound Stock Connect. Treasury bonds rallied while CNY declined -0.09% versus the US $ and copper managed a small gain of +0.13%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.74 versus 6.73 yesterday

- CNY/EUR 7.09 versus 7.09 yesterday

- Yield on 10-Year Government Bond 2.82% versus 2.82% yesterday

- Yield on 10-Year China Development Bank Bond 2.99% versus 3.00% yesterday

- Copper Price +0.13% overnight