Alibaba & Baidu Beat!

3 Min. Read Time

Key News

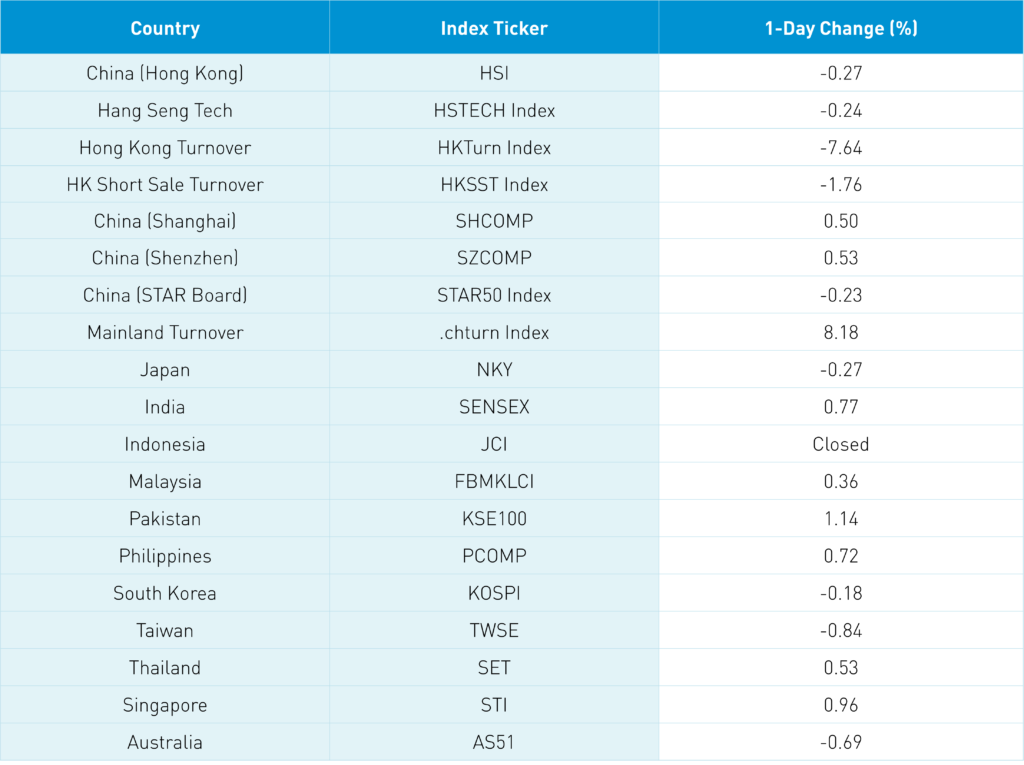

Asian equities were mixed overnight as Indonesia, like many European markets, was closed for Ascension Day.

The State Council held a conference call with a rumored one hundred thousand participants urging them to “…seize the time window and strive to bring the economy back to the normal track.” Policymakers are aware that “…indicators such as employment, industrial production, electricity consumption, and freight have fallen significantly…”. What’s going to be done about it?

We had the State Council outline thirty-three policies and measures meant to stabilize the economy. The PBOC and the insurance regulator (CBIRC) got the memo calling “24 key financial institutions” with emphasis on credit and loan growth while cutting payments for those in affected areas. Once again, onshore China reacted much more positively to the news than offshore China (Hong Kong). Hong Kong internet stocks were mixed overnight in advance of Alibaba and Baidu’s results this morning, discussed below.

Nikkei Asia is reporting that Wang Qishan is visiting Seoul to meet with President Biden to set up a summit. It would be a significant step in creating more dialogue between the two. At the same time, we have Secretary of State Blinken speaking today on China.

Pinduoduo (PDD US) reports tomorrow.

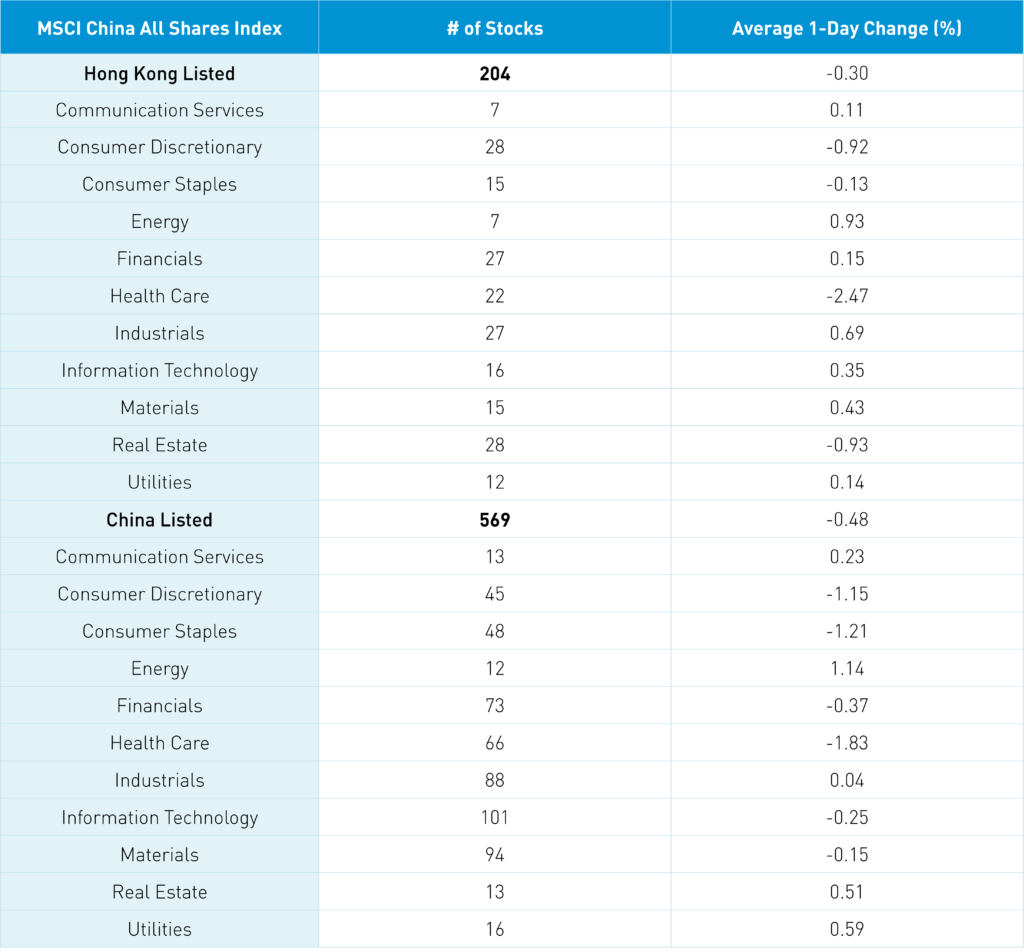

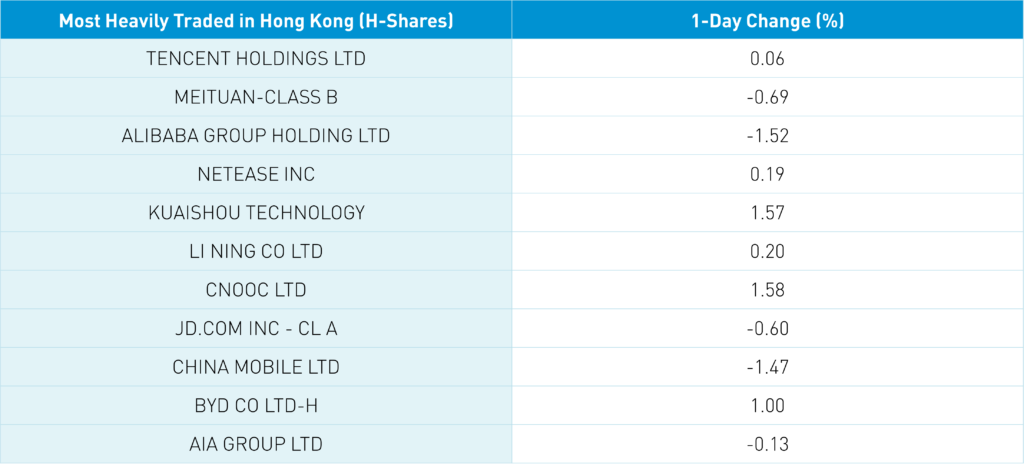

The Hang Seng Index and Hang Seng Tech closed -0.27% and -0.24% on volume -7.64% from yesterday, 67% of the 1-year average. There were 223 advancing stocks and 246 declining stocks. Hong Kong short sale volume -1.76% from yesterday, which is 73% of the 1- year average. Large caps outperformed small caps while value and growth factors were mixed. Top-performing sectors were energy +0.93%, industrials +0.6% and materials +0.43% while healthcare -2.47%, real estate -0.93% and discretionary -0.92%. Mainland investors were net buyers of Hong Kong stocks via Southbound Stock Connect on light volumes, with Tencent and Meituan seeing small net buys and China Mobile a healthy net buy.

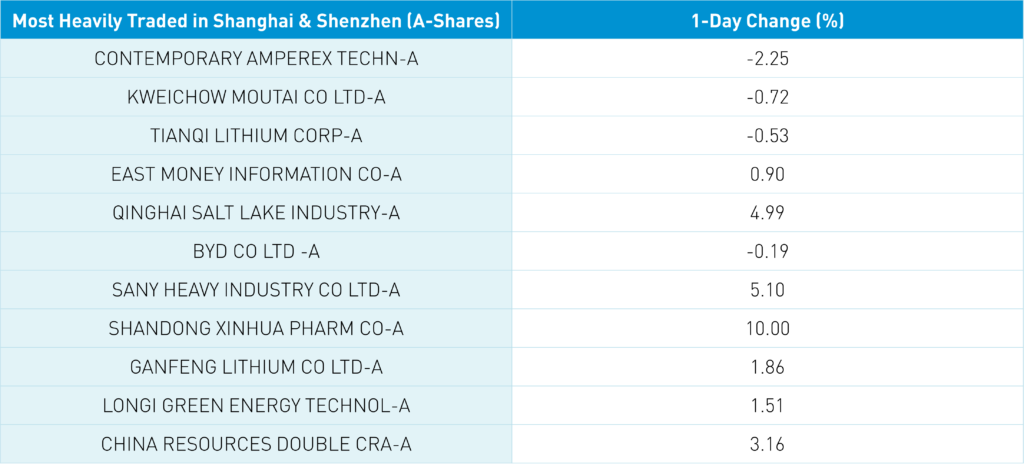

Shanghai, Shenzhen, and STAR Board diverged +0.5%, +0.53%, and -0.23% on volume +8.18% from yesterday, 76% of the 1-year average. There were 3,431 advancing stocks and 1,890 declining stocks. Value factors outperformed growth slightly as mega-caps underperformed large, mid, and small caps. Top sectors were energy +1.18%, utilities +0.63% and real estate +0.54% while healthcare -1.8%, staples -1.17% and discretionary -1.12%. Today, Northbound Stock Connect volumes were light as foreign investors sold -$217mm of Mainland stocks. Treasury bonds rallied while CNY was off -0.57% versus the US $ to 6.37 while copper -0.35%.

Alibaba reported fiscal year Q4 results post Hong Kong close/pre-US market open. Revenue, adjusted net income, and adjusted EPS beat analyst expectations. Yes, adjusted EPS and net income declined year-over-year (YoY) though we knew this was going into the release. Yes, the cloud wasn’t relatively as high but come on. All around solid job considering the circumstances. Hat tip to management as General/administrative expenses plunged. Stock buyback was very strong. The total value of goods solid is an incredible $1.312 trillion, while the total customers are more than 1.3 billion.

- Revenue increased 9% to RMB 204.052B ($32.188B) versus analyst expectations revenue RMB 200.594B

- Revenue breakdown: China commerce +8% to RMB 40.33B ($22.137B), local consumer services +29% to RMB 10.445 ($1.647B) and cloud +12% to RMB 18.971B ($2.993B)

- Annual active customers for the twelve months ended 3/31/2022 increased by 28.3mm to 1.31B, of which more than 1B were in China

- Gross merchandise value (GMV) was RMB 8.317 trillion ($1.312T)

- Adjusted net income declined -24% to RMB 19.799B ($3.123B) versus analyst expectations RMB 18.511B

- Adjusted EPS declined -23% to RMB 0.99 ($0.16) versus analyst expectations RMB 7.10

Baidu (BIDU US, 9888 HK) reported Q1 results to post Hong Kong close/pre-US market open. Baidu’s core search business continued to chug along while this quarter saw strong cloud and AI revenue growth. Like Tencent, advertising revenue was off as households tightened their purses and wallets. The company wisely invested profits from the core search business years ago, which is paying off nicely today. The company’s Beijing driverless/robo taxi has provided 196k rides in Q1 2022. Management did a reasonable job managing costs as Selling/General/Admin expenses declined by -11% YoY though R&D did +10% YoY. The spin-off of online entertainment/video streamer iQIYI weighed on Baidu’s results though it is still additive as the IQ beat expectations. At these levels, I’m surprised Baidu doesn’t buy iQIYI.

- Revenue increased +1% to RMB 28.411B ($4.48B) versus analyst expectations revenue RMB 27.859B

- Baidu Core revenue +4% to RMB 21.4B ($3.37B), online marketing revenue decreased -4%to RMB 15.7B ($2.47B), non-online marketing which includes AI and cloud +35% to RMB 5.7B ($903mm), revenue from iQIYI decreased -9% to RMB 7.3B ($1.15B)

- Total costs & expenses decreased significantly to RMB 4.072B from RMB 25.345B

- Adjusted net income RMB 3.9B ($612mm) versus analyst expectations of RMB 1.767B

- Adjusted EPS RMB 11.22 ($1.77) versus analyst expectations RMB 5.174

- Cash on the books is RMB 191B ($30.13B)

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.73 versus 6.69 yesterday

- CNY/EUR 7.19 versus 7.14 yesterday

- Yield on 10-Year Government Bond 2.71% versus 2.76% yesterday

- Yield on 10-Year China Development Bank Bond 2.93% versus 2.96% yesterday

- Copper Price -0.35% overnight