Meituan Motors, EVs Electrify, Didi to Relist in Hong Kong

2 Min. Read Time

Key News

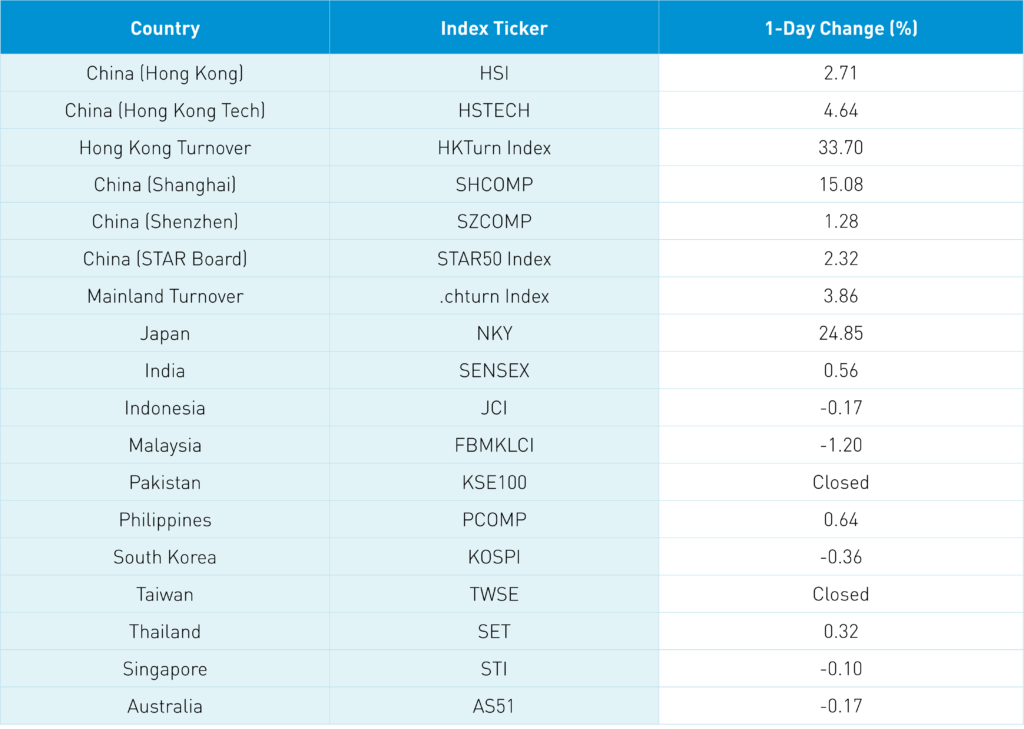

North Asian equity markets outperformed South Asia, led by China and Hong Kong while Malaysia and South Korea were closed.

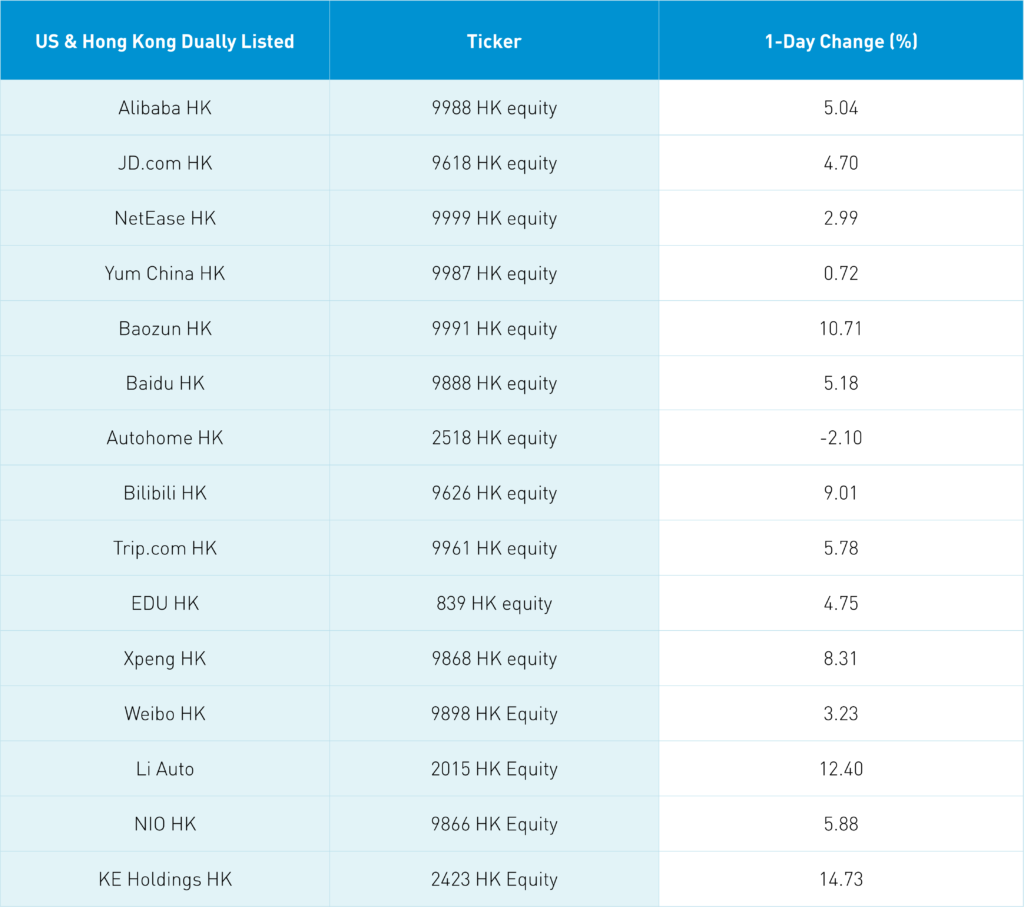

Today’s Wall Street Journal article on Didi’s cybersecurity review concluding came after the close in Hong Kong, though rumors extended the market’s rally into the close. The review’s conclusion should allow Didi, along with Full Truck Alliance, to relist in Hong Kong.

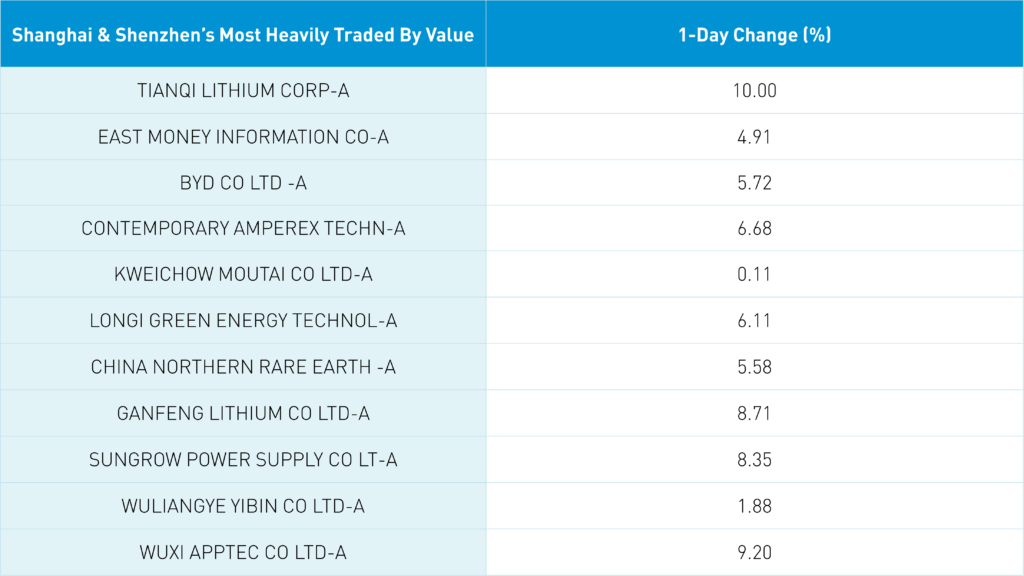

Today was truly a growth rally from stock, sector, and factor perspectives as the clean technology ecosystem had a strong day led by electric vehicles (EVs), lithium names, and rare metals along with health care. The rally was powered by Meituan’s +25% year-over-year revenue increase and smaller net loss, reports of US tariffs coming off to stave off inflation, policies supporting auto sales including EVs, and EV battery and bus maker BYD buying access to lithium mines.

There has also been increased coverage of active asset managers’ China underweight diminishing, driven by low valuations and China’s stable balance sheet versus peers.

China and Hong Kong’s three-day weekend saw a jump back to nearly pre-pandemic spending levels while E-Commerce companies’ 618 sales event kicked off. While 618 is not as well-known as Singles Day, the multi-week event should be a nice catalyst for E-Commerce. All in, it was a strong day on good volumes as sentiment improves. Yes, I am knocking on wood!

I recommend Jocko Willink and Leif Babin’s excellent book titled Extreme Ownership: How U.S. Navy Seals Lead and Win.

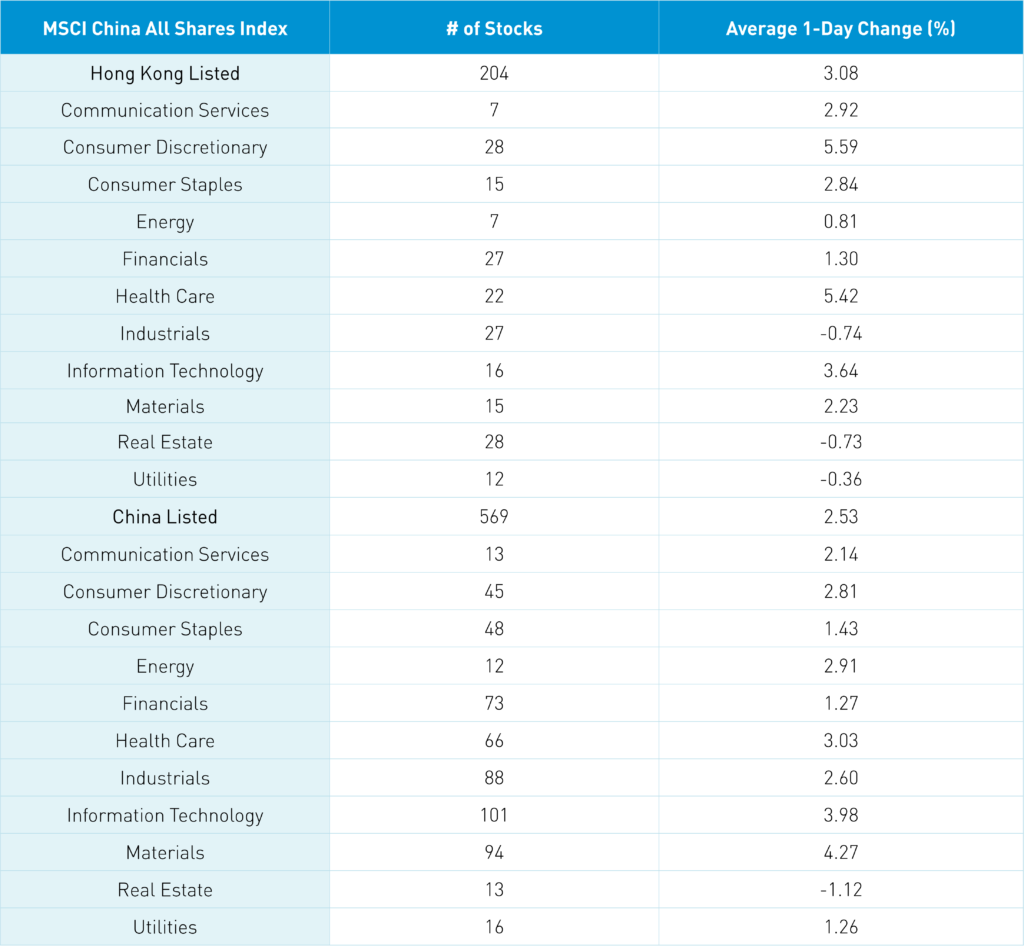

The Hang Seng and Hang Seng Tech gained +2.71% and +4.64%, respectively, on volume that increased +33.7% from Thursday, which is 98% of the 1-year average. There were 299 advancing stocks versus only 172 decliners. Hong Kong short sale turnover increased +15.08%, which is 95% of the 1-year average. Growth and size were outperforming factors while value and dividend factors underperformed. Discretionary, health care tech, and communication outperformed +5.59%, +5.42%, +3.64%, and +2.92%, respectively, while utilities, real estate, and industrials underperformed -0.36%, -0.73%, and -0.74%, respectively. Southbound Stock Connect volumes were elevated as Mainland investors were net buyers of Hong Kong stocks.

Shanghai, Shenzhen, and the STAR Board gained +1.28%, +2.32%, and +3.86%, respectively, on volume that increased +24.85% from Thursday, which is 102% of the 1-year average. 3,403 stocks advanced while 957 stocks declined. Growth factors outperformed dividend and value factors today while small caps outperformed large caps. Outperforming sectors were materials, which gained +4.28%, tech, which gained +3.99%, and healthcare, which gained +3.04% while real estate was the only declining sector, falling -1.11%. Foreign investors bought a healthy +$1.695 billion worth of Mainland stocks today via Northbound Stock Connect.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.65 versus 6.66 Thursday

- CNY/EUR 7.12 versus 7.14 Thursday

- Yield on 1-Day Government Bond 1.20% versus 1.21% Thursday

- Yield on 10-Year Government Bond 2.78% versus 2.76% Thursday

- Yield on 10-Year China Development Bank Bond 3.01% versus 2.99% Thursday

- Copper Price +1.01% overnight