Ant IPO, Bilibili Q1, 618 Event, Nio Q1 & Inclusion

2 Min. Read Time

Key News

Asian equities were lower overnight, less India as Hong Kong internet names pulled back after yesterday’s monster move (or, as my Boston friends would say, Monstah!). Since the March 15th low, Chinese internet stocks and Hong Kong stocks have had a strong move as we saw profit-taking overnight. Let’s see if the dip is bought by active fund managers who are under-weight China in their EM and global portfolios.

This morning, a tennis match ensued on whether or not the Ant Group IPO is coming from public reports followed by denials. Who knows, though? We have pointed out that news articles based on “unnamed sources” need to be taken with a grain of salt. A data-driven approach would argue that stock analysts use Sum of the Parts (SOTP) analysis to fair value Alibaba, including their 1/3ownership of Ant. Mainland China was off despite strong May export of +16.9% year over year and import data +4.1% YoY, which handily beat economist expectations. The data highlights that Shanghai, an important economic, financial, and port city, is only 26mm of China’s 1.4B people. Some chatter on new Covid cases in Shanghai and Beijing was cited as causes for today’s pullback.

Bilibili (BILI US, 9626 HK) reported Q1 financial results post-Hong Kong close/pre-US market open. Revenue (+30% year over year) and adjusted EPS missed expectations, while the company’s Q2 outlook beat expectations. The company announced it would convert its Hong Kong share class from a secondary offering to a dual listed. That change would make the stock eligible for Southbound Stock Connect. Our friend Matt pinged me on data from the 618 sales event. Started by JD.com, the two-week sales event is a spring event similar to Alibaba's November 11th Singles Day sales event. JD.com released on their website that the early look at sales is very strong/+100% year over year in many categories. I see very little press on the 618 event though e-commerce companies are beneficiaries (JD, BABA, PDD, VIPS). Nio (NIO US, 9866 HK) also reported Q1 post-Hong Kong/pre-US market open. Revenue and EPS beat analyst expectations though the Q2 revenue and delivery forecast were missed.

After the close today, MSCI will announce its country classification update. No changes are expected, but in theory, a review of South Korea as a developed market and/or starting China A inclusion could happen. Tomorrow Mainland volumes will be high as domestic Chinese indexes rebalance. We also have Hang Seng indexes rebalancing. Remember Nio will be added to the broad Hang Seng Composite and the Hang Seng Tech index.

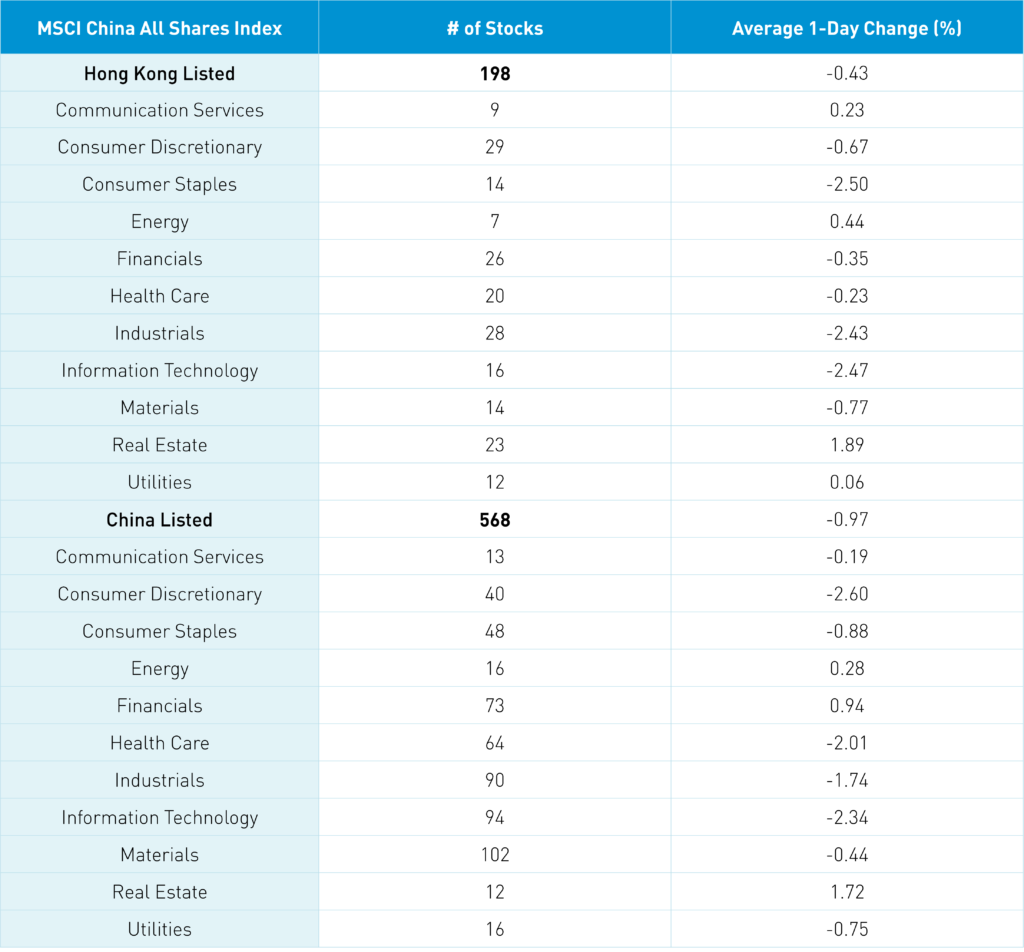

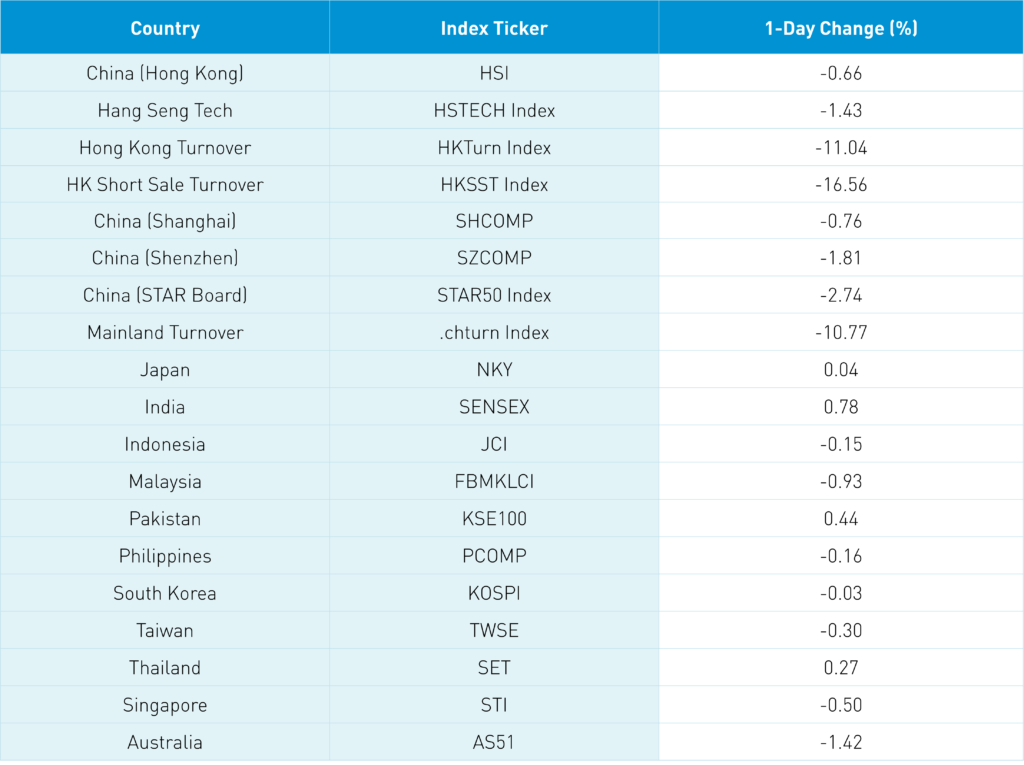

The Hang Seng and Hang Seng Tech closed -0.66% and -1.43% on volume -11.04% from yesterday, which is 115% of the 1-year average. 157 stocks advanced while 316 stocks declined. Hong Kong short sale volume declined by -16.56% from yesterday, which is 118% of the 1-year average. Large caps underperformed small caps while value and growth factors’ performance was about the same. Real estate was the top sector +1.89% followed by energy +0.44% and communication +0.23% while staples -2.5%, tech -2.47% and industrials -2.43%. Education stocks were a top-performing sub-sector while the Apple ecosystem and port stocks underperformed. Southbound Stock Connect volumes were elevated in mixed trading as Tencent was sold small while Kuaishou and Meituan were bought small.

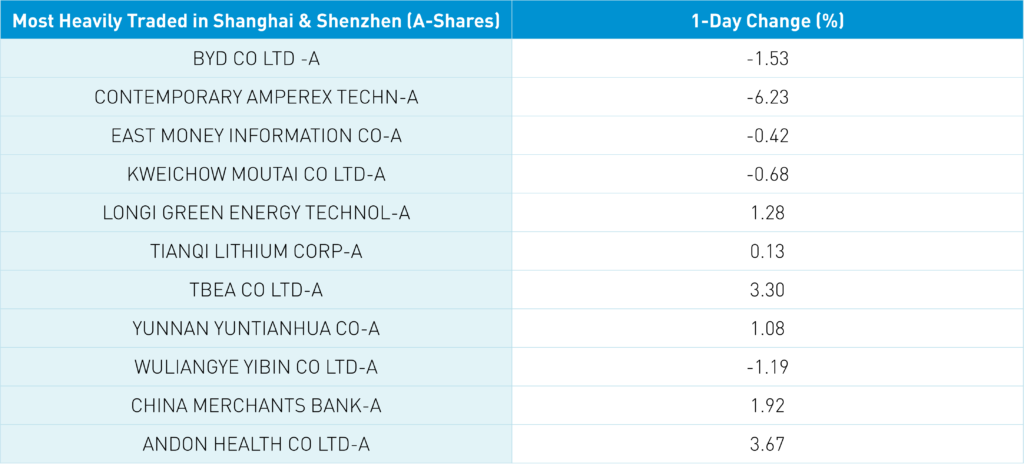

Shanghai, Shenzhen, and STAR Board were off -0.76%, -1.81%, and -2.74% on volume -10.77% from yesterday, which is 90% of the 1-year average. There were only 632 advancing stocks, while 3,825 stocks declined. Value outperformed growth handily while large caps outperformed small caps. Real estate was the top sector +1.67% followed by financials +0.9% and energy +0.24% while discretionary -2.64%, tech -2.38%, healthcare -2.05% and industrials -1.78%. Northbound Stock volumes were moderate as foreign investors bought $536mm of Mainland stocks net of sales. Treasury bonds rallied, CNY rallied versus the US $, and copper +0.18%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.67 versus 6.69 yesterday

- CNY/EUR 7.15 versus 7.18 yesterday

- Yield on 10-Year Government Bond 2.76% versus 2.77% yesterday

- Yield on 10-Year China Development Bank Bond 2.98% versus 2.99% yesterday

- Copper Price +0.18% overnight