NetEase Surges on Game Approval, Baidu Introduces Fully Autonomous SUV

3 Min. Read Time

Key News

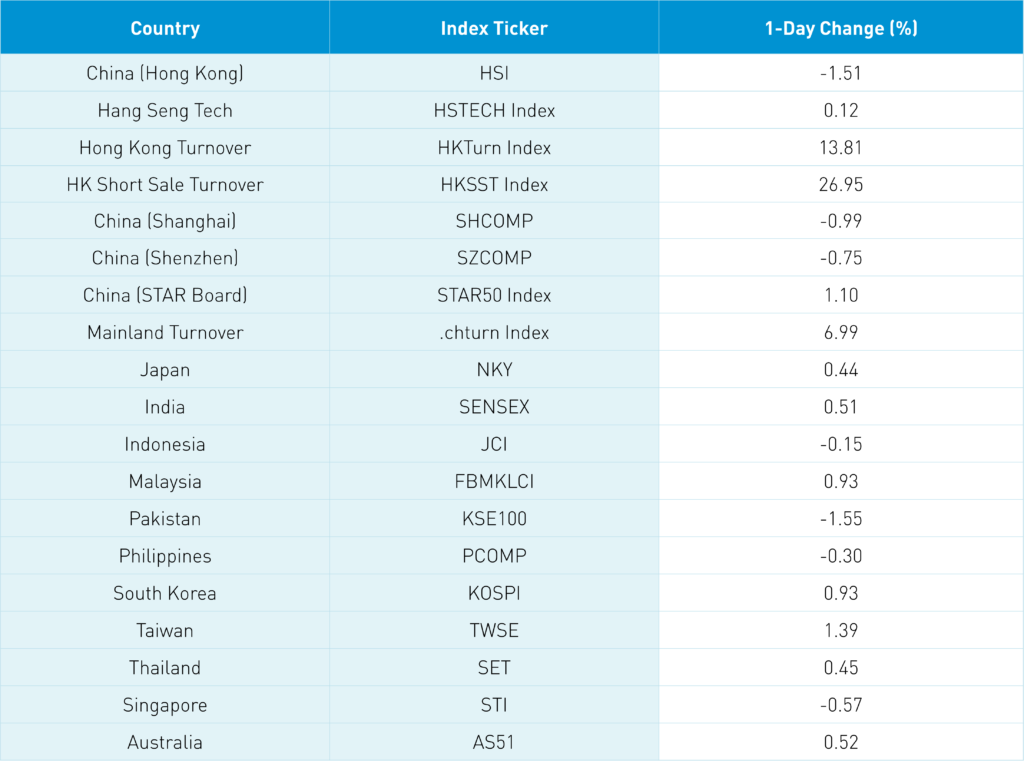

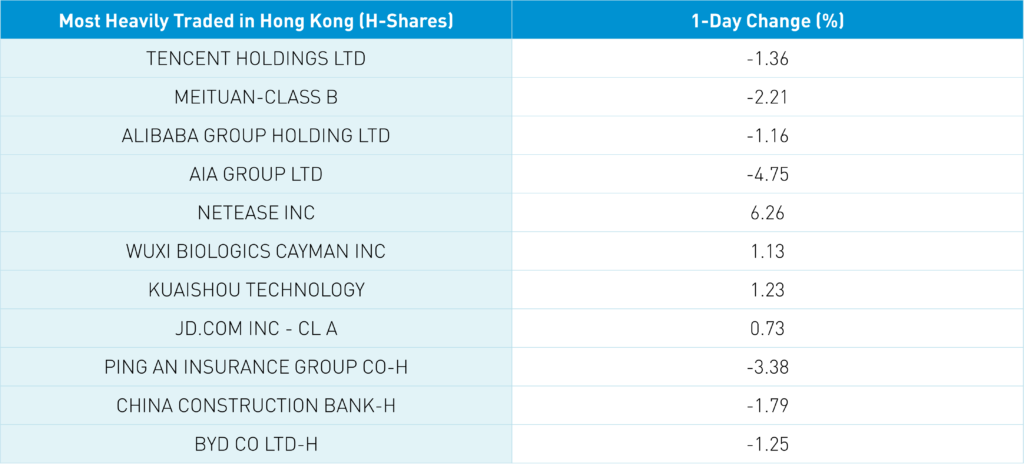

Asian equities were mixed overnight on light volumes as the summer lull is in full effect. Hong Kong was largely down, led by Tencent -1.36%, Meituan -2.21%, and Alibaba HK -1.1% though the Hang Seng Tech gained +0.12%, led by NetEase +6.26% on reports its immensely popular Diablo Immortal video game will be approved in China. Yes, I felt old writing that! I am a little surprised Tencent was off overnight as the opening up of online game approvals should be a tailwind. Tencent's issue is that we don't know how many shares Prosus sells, leading to a sentiment overhang. Also a little surprised online gaming TV/video provider Bilibili HK was up only +0.69%. Same on Baidu HK -1.07% as Baidu World kicked off overnight with the company announcing the Apollo RT6 autonomous EV. The vehicle has a detachable steering wheel which is cool and disconcerting (Look, Ma, no hands!).

We also had Didi's fine confirmed at $1.2B, which was a great scoop by the WSJ earlier this week.

Early indications show that the US semiconductor subsidy bill doesn't include shortening the HFCAA delisting window. Yesterday's news of a Mainland star portfolio manager buying Alibaba and Tencent should be good news. We did see Tencent, Meituan, and Kuaishou seeing small net buying from Mainland investors via Southbound Stock Connect. Ultimately it was an off-night as shorts pressed their bets a bit though more focused on real estate plays than the internet. The Mainland market was off though semiconductor stocks had a great day lifting STAR Board +1.1%. Overall the market was off as Premier Li's speech yesterday noted that "incremental" stimulus was coming. This weighed on real estate, financial and discretionary stocks which would be beneficiaries of the stimulus.

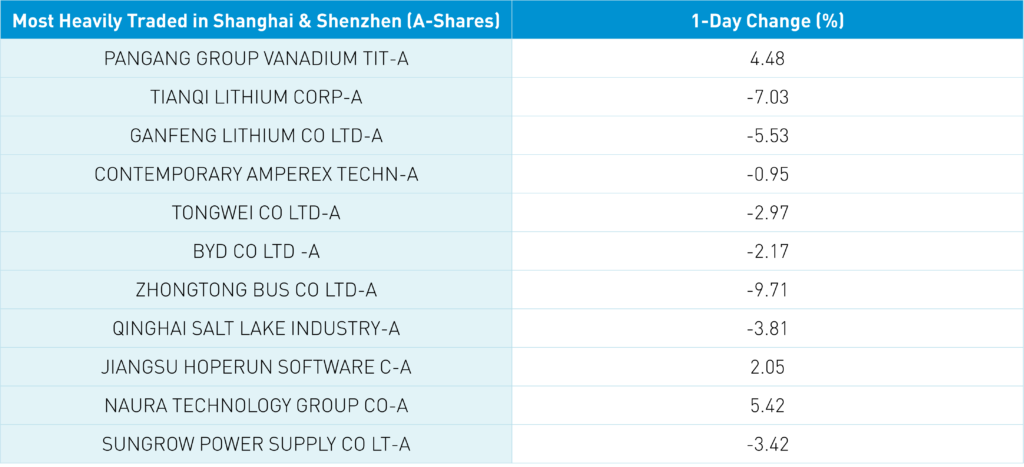

Stimulus is coming but incrementally and not massively. The clean tech ecosystem was off despite the World Power Battery Conference that started overnight in Yibin with positive comments from battery powerhouse CATL (300750 CH) -0.95%. CATL's Chairman stated the company has a 34% global market share for EV batteries and operations in 55 countries. Nancy Pelosi's trip to Taiwan may have weighed on Mainland sentiment. President Biden and President Xi will have a call likely due to the announced trip. Today, foreign investors were net sellers of Mainland stocks -$406mm. CSI 1,000 futures will list tomorrow for the first time, with several ETFs anticipated to be launched. According to my colleague Derek, 9 of the 1,000 stocks are STAR 50 Index listed stocks. A total of 67 STAR Board-listed stocks are in the CSI 1,000.

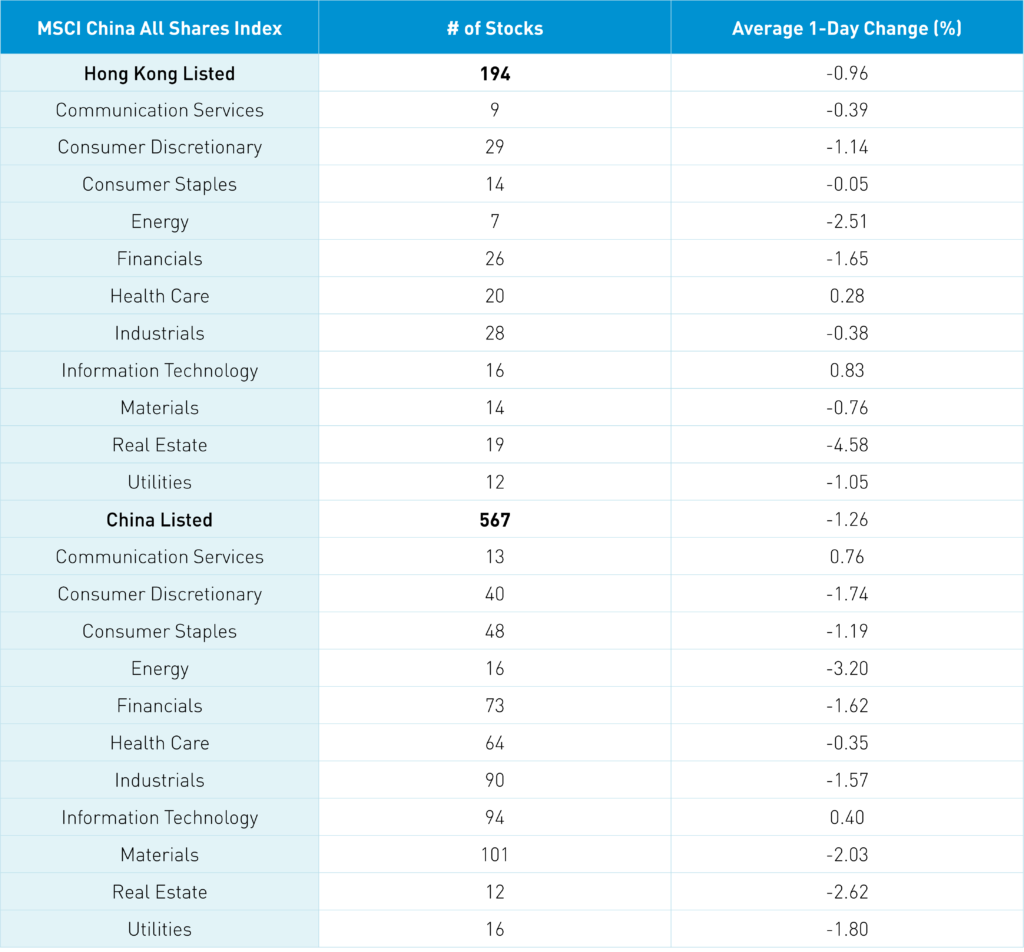

The Hang Seng and Hang Seng Tech diverged by -1.51% and +0.12% on volume +13.81% from yesterday which is 72% of the 1-year average. 148 stocks advanced while 324 declined. Hong Kong short sale turnover increased +26.96% which is 72% of the 1-year average as Hong Kong short sale turnover accounted for 16% of total turnover. Value and growth factors were down equally as small caps outperformed large caps. Tech and healthcare were the only positive sectors +0.83% and +0.28% while real estate -4.58%, energy -2.51%, and financials -1.65%. Top sub-sectors were cobalt, Tik Tok-related stocks, Apple-related stocks, liquor stocks and ominously funeral stocks, coal stocks, real estate sub-sectors, and associated industries such as property management and construction companies. Southbound Stock Connect volumes were light as Mainland investors were net buyers of Hong Kong stocks with Tencent, Kuiashou, and Meituan net small buys while Li and BYD were net small sells.

Shanghai, Shenzhen, and STAR Board diverged -0.99%, -0.75%, and +1.1% on volume +6.99% from yesterday which is 94% of the 1-year average. 1,975 stocks advanced while 2,436 stocks declined. Growth outperformed value but not significantly as small caps outperformed large caps. Communication and tech were the only positive sectors today +0.78% and +0.41% while energy -3.19%, real estate -2.61%, and materials -2.01%. The top sub-sectors were semiconductor, SMIC-related companies, and online game stocks while lithium, coal, and electricity were among the worst. Northbound Stock Connect volumes were light as foreign investors sold -$406mm of Mainland stocks. Treasury bonds rallied, CNY eased -0.22% to 6.77 versus the US $ and copper gained +0.23%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.77 versus 6.76 yesterday

- CNY/EUR 6.90 versus 6.90 yesterday

- Yield on 10-Year Government Bond 2.76% versus 2.77% yesterday

- Yield on 10-Year China Development Bank Bond 3.03% versus 3.04% yesterday

- Copper Price +0.23% overnight