Mainland Markets Shake It Off, Hong Kong Holds Up

3 Min. Read Time

Key News

Asian equities had a positive start to the week except for Taiwan, which was off a touch. Mainland China media is reporting Nancy Pelosi is likely to visit Taiwan tomorrow, though this has not been confirmed.

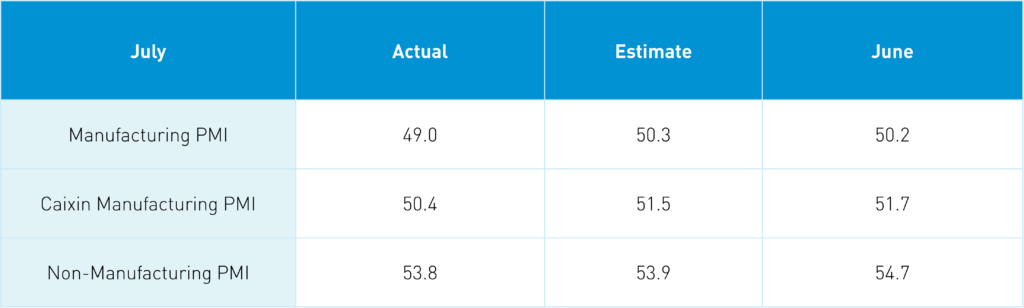

Over the weekend, China released PMI data that was lower than expected. The Mainland took the release as a positive as it shows why the government needs to support the economy. Last week, the State Council stated that while a “massive” stimulus package is not in play, we can expect some incremental stimulus measures.

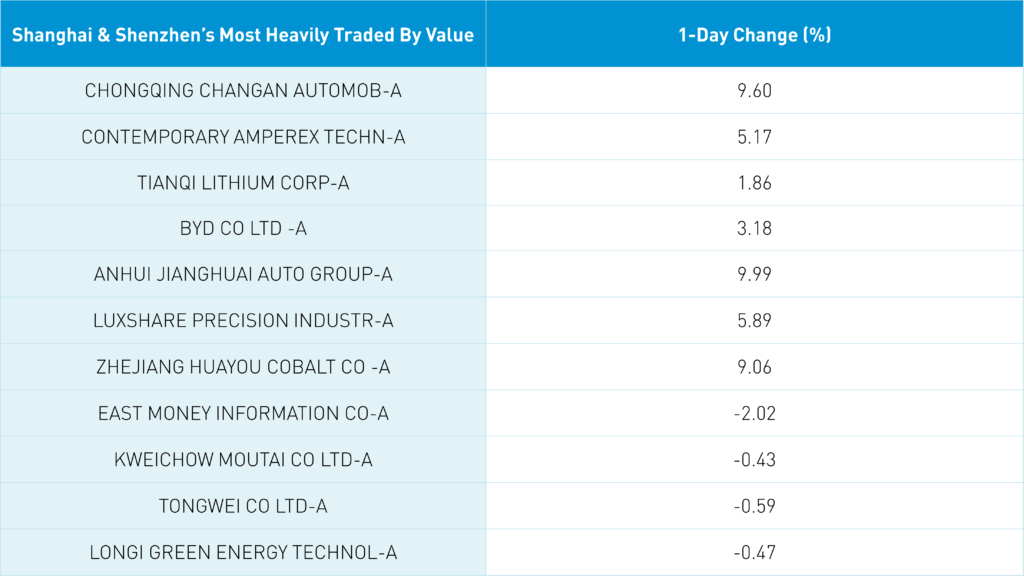

The Mainland market responded positively to policy comments supporting consumption with an emphasis on autos, electric vehicle (EV) support, and favorable policies for home appliances. The Mainland market’s five most heavily traded stocks came from these themes: Chongqing Changan Auto, which gained +9.6%, EV battery maker CATL, which gained +5.17%, Tianqi Lithium, which gained +1.8%, BYD, which gained +3.18%, and Anhui Jianghuai Auto, which gained +9.99%. Kweichow Moutai fell -0.43% though a large foreign asset manager’s China fund added the stock to its top ten holdings.

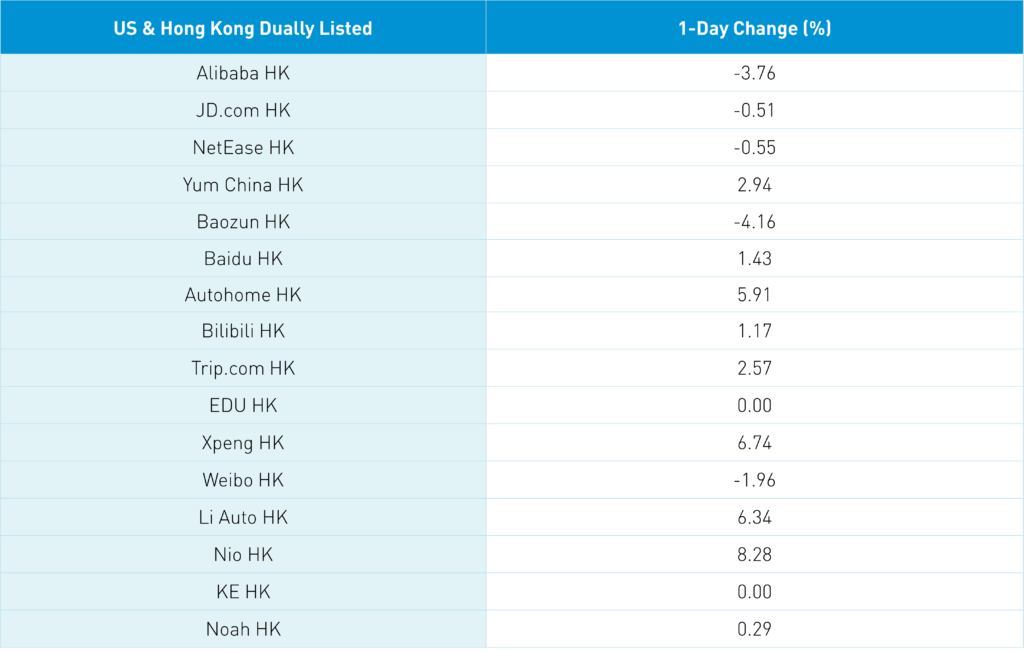

The Hang Seng managed a small gain, overcoming morning losses. However, the Hang Seng Tech Index was off slightly due to weakness in Tencent, which fell -2.35%, and Alibaba, which fell -3.76% in Hong Kong overnight, though other internet stocks managed small gains. There was a great deal of chatter about Tencent’s ADR seeing a big conversion Friday, which could lead to purchases of the stock in Hong Kong. These losses pale in comparison to Friday’s selloff in these stocks’ US-listed counterparts. It is interesting to note that Alibaba’s US ADR was off considerably well in advance of the SEC’s release of its inevitable addition to the Holding Foreign Companies Accountable Act (HFCAA) non-compliant list. I am not a conspiracy theorist, but there are clearly some loose lips.

Over the weekend, Alibaba stated that it is firmly committed to its US listing. I do not see the company’s move to make Hong Kong a primary listing location as an anti-US ADR move because the move also paves the way for Mainland investors to buy the stock via Southbound Stock Connect. Friday’s US move in Alibaba stock was strange as the media only focused on news of restaurant delivery talks with the Hangzhou authority, but totally underreported the government’s positive statements on ending technology and internet regulation. The issue here is a lack of buyers as shorts tend to press their bets on negative news against the backdrop of light summer volumes. In the absence of buyers, shorts, with some help from the negative headlines, are pushing the narrative.

Hong Kong-listed EV and auto-related names also had a strong day, supported by comments from policymakers and decent July sales numbers, which were off month-over-month, but very strong year-over-year.

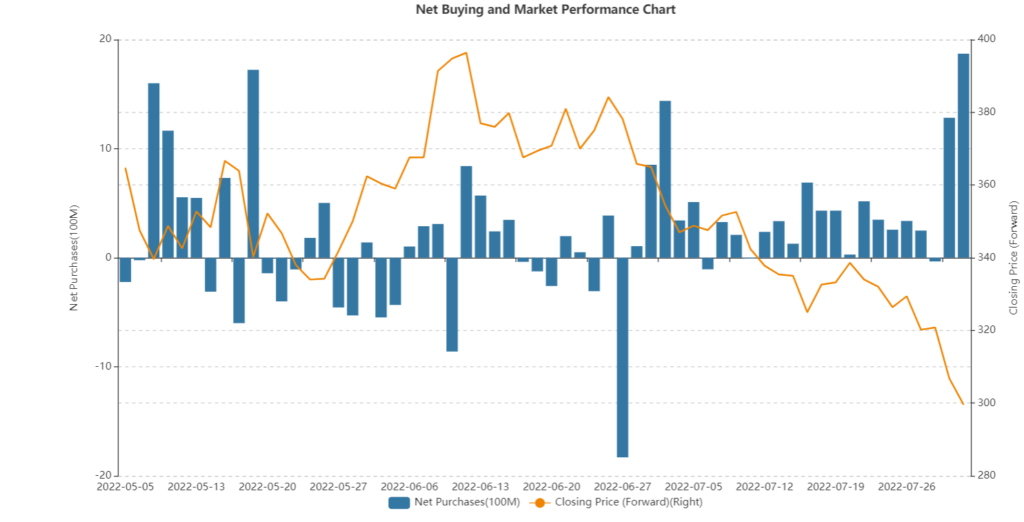

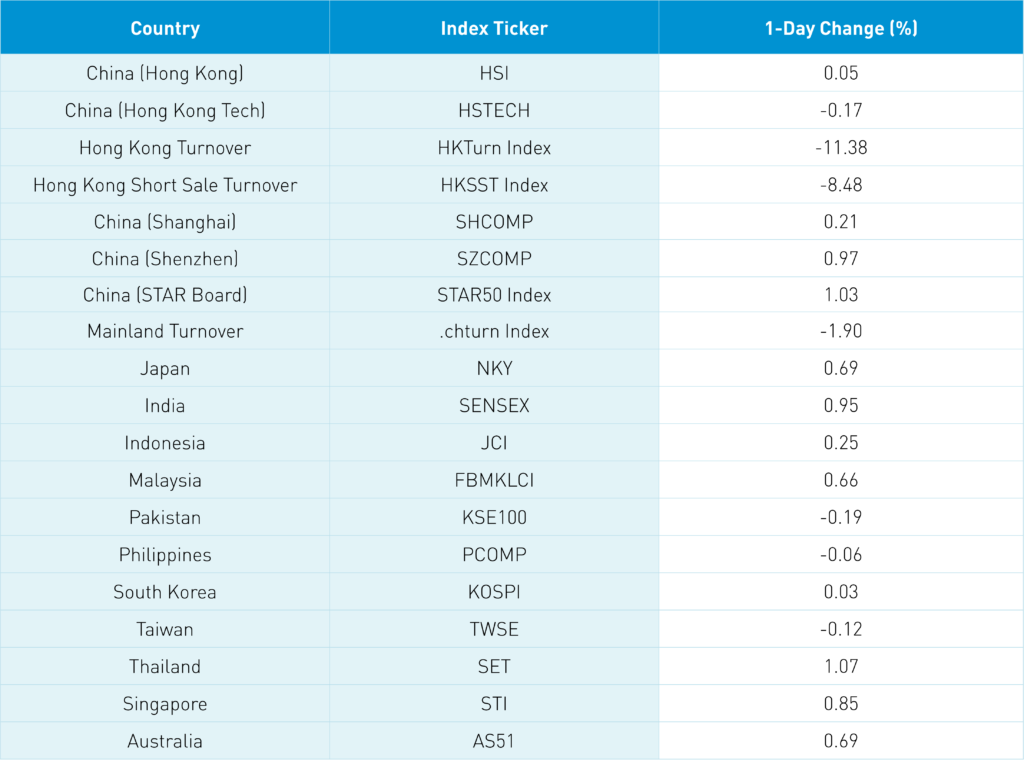

The Hang Seng and Hang Seng Tech Indexes diverged to close +0.05% and -0.17%, respectively, on volume that was down -11.38% from Friday, which is 84% of the 1-year average. Only 116 stocks advanced while 357 stocks declined. Hong Kong short sale turnover was off -8.48% from Friday, which is 99% of the 1-year average, while short sale turnover accounted for 19% of total turnover. Growth and value factors were mixed as large caps outperformed small caps. Only consumer staples and energy were positive, gaining +0.4% and +0.1%, respectively. Meanwhile, industrials fell -1.59%, communication fell -1.56%, and materials and healthcare were both off -1.32%. Autos and EV-related sub-sectors including lithium, were the top performers, along with online travel, while electric utilities and health care were among the worst performing sub-sectors. Southbound Stock Connect volumes were light as Mainland investors were net buyers of Hong Kong-listed stocks. Tencent saw significant Mainland buying along with Meituan and a Hong Kong-listed China ETF, though Kuaishou saw net sales from Mainland investors.

Shanghai, Shenzhen, and the STAR Board gained +0.21%, +0.97%, and +1.03%, respectively, on volume that declined -1.9% from Friday, which is 93% of the 1-year average. Growth factors outperformed value factors today while small caps edged large caps. The top performing sectors were energy, which gained +2.05%, consumer discretionary, which gained +1.64%, and industrials +1.19%, which gained, while real estate fell -2.41%, financials fell -1.27% and utilities fell -0.97%. Autos and EV-related sub-sectors were the top performing sub-sectors, while the real estate and infrastructure sub-sectors were among the worst. Northbound Stock Connect volumes were light as foreign investors bought $354 million worth of Mainland stocks today. CNY was off slightly versus the US dollar while copper gained +1.71%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.77 versus 6.74 Friday

- CNY/EUR 6.93 versus 6.88 Friday

- Yield on 1-Day Government Bond 1.15% versus 1.15% Friday

- Yield on 10-Year Government Bond 2.73% versus 2.76% Friday

- Yield on 10-Year China Development Bank Bond 2.90% versus 2.93% Friday

- Copper Price +1.71% overnight