Baidu To Offer Robo Taxis In More Cities, Alibaba Prepares For Southbound Stock Connect Eligibility

3 Min. Read Time

Key News

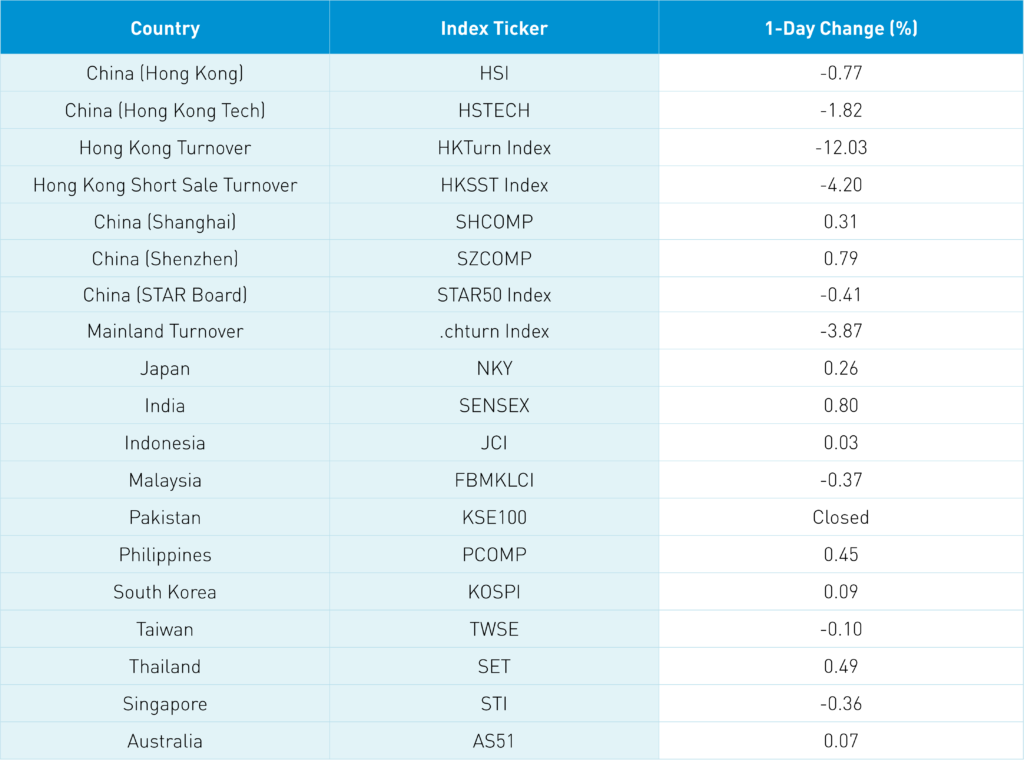

Asian equity markets were largely higher on light summer volumes as Pakistan was closed for Ashura, an important Islamic holiday that occurs on the tenth day of Muharram, the first month in the lunar calendar.

Friday’s strong US Non-Farm Payroll (NFP) release likely confirms another 75 basis point Fed hike though Wednesday’s CPI release will be highly scrutinized.

The big news over the weekend was strong Chinese exports in July, increasing +18% year-over-year (YoY) versus expectations of +14.1% and June’s +17.9%. This is a strong indicator that the global economy continues to power through headwinds. Supply chain issues appear to have subsided as well. However, China's imports grew at only +2.3% YoY versus expectations of 4% and June’s 1%, indicating modest domestic demand. Lower commodity prices were also a factor in the lower import number. Despite the political rhetoric, July trade between the US and China INCREASED by +7.5% YoY to $68.5 billion, while trade with Taiwan fell by -3% to $27 billion.

Hong Kong-listed internet stocks were off following losses in their US-listed counterparts on Friday. Hong Kong’s most heavily traded stocks by value were Tencent, which fell -2.6% despite another day of net buying from Mainland investors via Southbound Stock Connect, Alibaba, which fell -4.41% on layoffs rumors though cutting costs is usually a good thing, Meituan, which fell -2.13%, and JD.com, which fell -3.26%.

Baidu fell -1.81% despite the company being given the approval to operate autonomous taxis in two additional cities: Chongqing and Wuhan.

In addition to the very light volumes due to summer doldrums, reports of Hainan Island experiencing a covid outbreak garnered headlines, which has led to a lockdown in one section of the island. Meanwhile, Japanese investment firm Softbank’s loss of 3.16 trillion Yen weighed on tech regionally.

Following the US Senate’s passage of the clean energy-focused Build Back Better bill, I would have thought the clean technology ecosystem would have had a great day as many of the basic inputs are made in China. Nonetheless, electric vehicle (EV) plays in Hong Kong and Mainland China were off on reports that higher commodity prices for lithium will lead to higher car prices. It is worth noting that the Senate bill does not reduce the Holding Foreign Companies Accountable Act (HFCAA) compliance window from three years to two years. This is a significant positive for China equities.

Mainland markets were less concerned about these issues as the STAR Board was hit with some profit taking. There has been a fair amount of talk about the importance of semiconductors within active funds as the industry becomes a core pillar of asset allocations along with green technology.

Alibaba announced this morning it expects to convert its Hong Kong listing to a primary listing by year-end. This would make the Hong Kong listing eligible for purchase by Mainland investors via Southbound Stock Connect. Back of the envelope, I would expect nearly $20 billion worth of inflow into the company’s Hong Kong-listed shares.

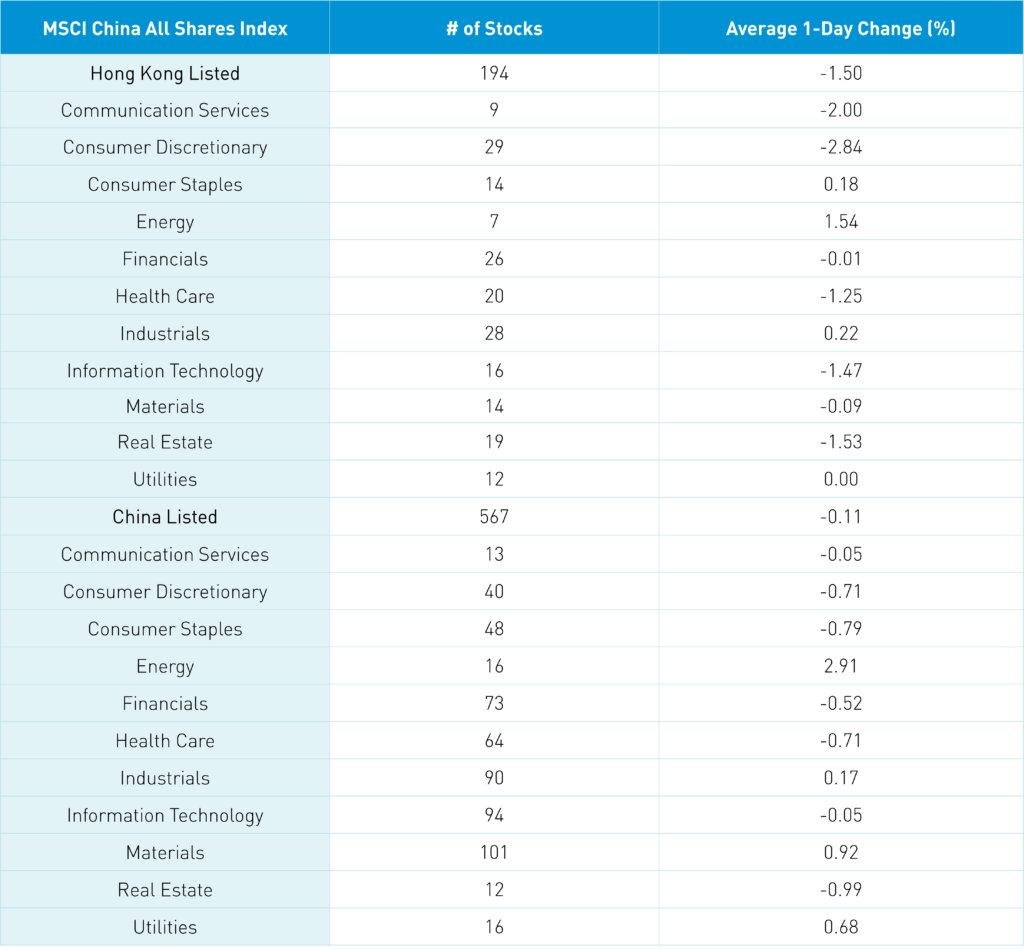

The Hang Seng and Hang Seng Tech indexes fell -0.77% and -1.82%, respectively, on volume that was down -12% from Friday, which is just 55% of the 1-year average. 170 stocks advanced while 290 declined. Hong Kong short sale turnover declined -4.2% from Friday, which is 55% of the 1-year average, as short sale turnover accounted for 16% of total turnover. Value factors outperformed today along with small caps. The top performing sectors were energy, which gained +1.54%, industrials, which gained +0.22%, and consumer staples, which gained +0.18%. Meanwhile, consumer discretionary fell -2.84%, communication services fell -2% and real estate fell -1.53%. The top performing sub-sectors were paper, coal, and defense. Meanwhile, online education, appliance, and Ant Group ecosystem companies were underperformers. Southbound Stock Connect volumes were very light as Mainland investors were slight net sellers of Hong Kong stocks as Tencent was a small net buy while Kuaishou, Meituan, and Geely Auto were all net sold by Mainland investors.

Shanghai, Shenzhen, and the STAR Board had a mixed session, closing +0.31%, +0.79%, and -0.41%, respectively, on volume decreased -3.87% from Friday, which is 89% of the 1-year average. 3,114 stocks advanced while 1,301 stocks declined. Value and Growth factors were mixed, while small caps outperformed large caps. The top performing sectors were energy, which gained +2.91%, materials, which gained +0.92%, and utilities, which gained +0.68%. Meanwhile, real estate fell -0.88%, consumer staples fell -0.79%, and healthcare fell -0.71%. The top performing sub-sectors were coal, wind, and solar. Meanwhile, semiconductors and travel-related stocks such as airlines were underperformers. Northbound Stock Connect volumes were light as foreign investors sold a net -$159 million worth of Mainland stocks as Longi Green Energy was bought while Tianqi Lithium was sold. Treasury bonds were sold, CNY was off versus the US dollar, falling -0.03%, and copper gained +1.44%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.76 versus 2.76 Friday

- CNY/EUR 6.89 versus 6.87 Friday

- Yield on 1-Day Government Bond 1.00% versus 1.00% Friday

- Yield on 10-Year Government Bond 2.74% versus 2.73% Friday

- Yield on 10-Year China Development Bank Bond 2.90% versus 2.90% Friday

- Copper Price +1.44% overnight