GM Outsells Tesla in July as Semiconductors & Clean Tech Outperform

3 Min. Read Time

Key News

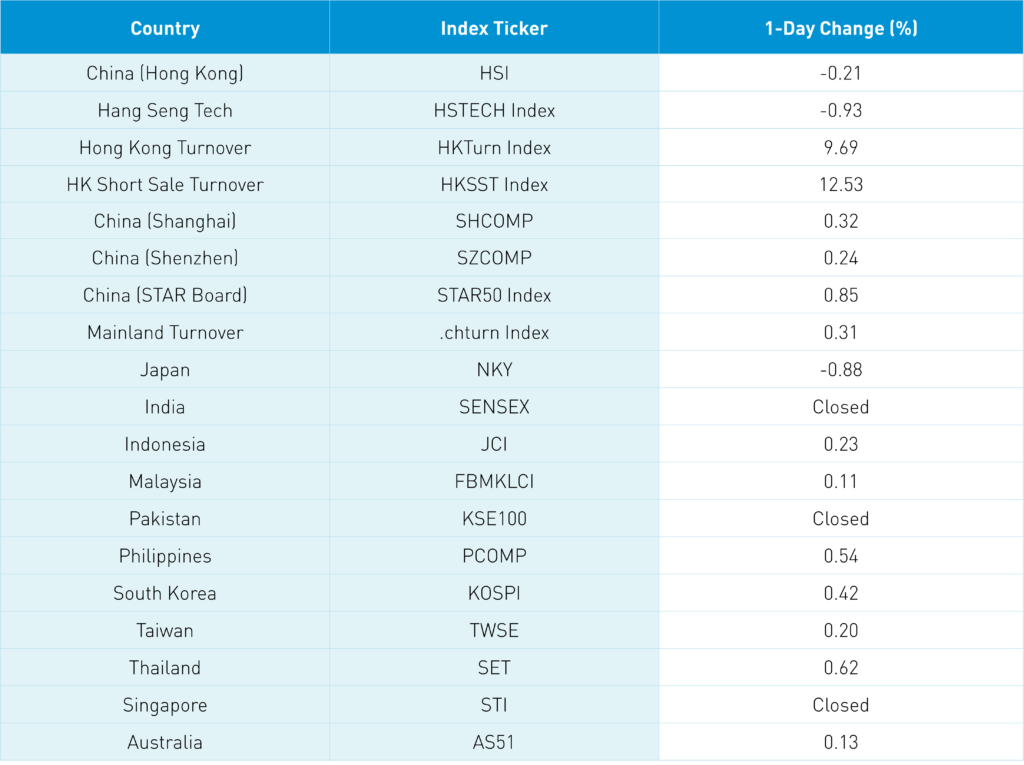

Asian equities were largely higher on light volumes. Japan and Hong Kong were off slightly while India (Moharram), Pakistan (Ashura), and Singapore (National Day) were closed for the holiday. Tomorrow we have the highly anticipated July CPI print. I am referencing China's CPI, which is expected to be 2.9% (tongue in cheek!). As an FYI, that other CPI print tomorrow in the US is expected at 8.7%. Taiwan is dominating the headlines as it's summertime, and nothing else is happening. Am I worried? No, as CNH, China's currency, and Chinese Treasuries are significant risk indicators that aren't freaking out, so nor am I. Also, check out FlightRadar24.com, as you'll notice a lot of flights into and out of Taipei's airport!

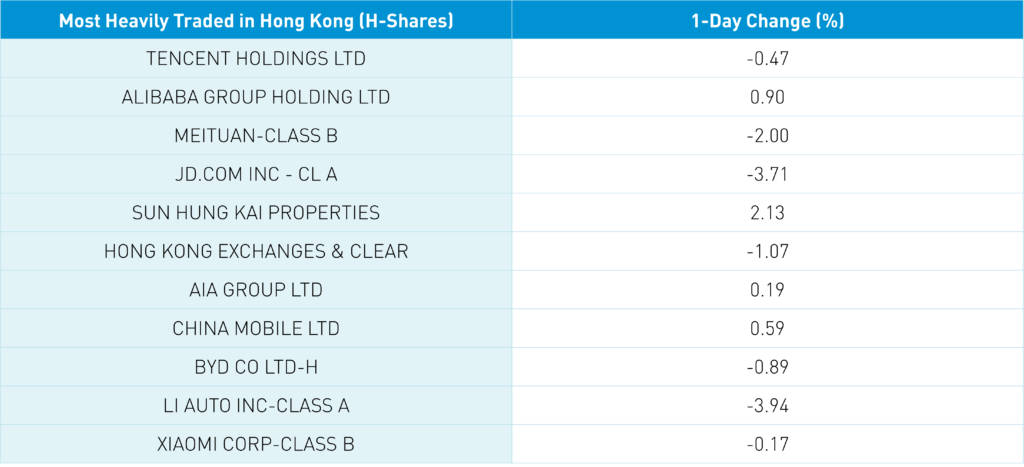

Hong Kong's most heavily traded stocks by value were Tencent -0.47% as Prosus continues to sell shares to fund its buyback, Alibaba HK +0.9% following their filing with the Hong Kong Exchange to make Hong Kong its primary listing which would make it eligible for Southbound Stock Connect, Meituan -2% and JD.com HK -3.71%. Tianqi Lithium's HK share class +5.39% was added to Southbound Stock Connect Monday, only one month after its Hong Kong listing. Today the company had US $27mm of net buying from Mainland investors. The real prize is getting Tencent's 716mm shares, which is 7.44% of total shares held by Southbound investors, with a value of Hong Kong $223B/US $28B.

Amazing that Alibaba's US ADR was DOWN yesterday! It makes no sense! Short sellers noticed that Alibaba HK's volume short percentage fell 11% from its 20-day average (great stat tip/ from my buddies Jonathan and John). In Hong Kong, real estate stocks had a pop on rumors that the local property tax would be eliminated though it was denied. I did see that the Chinese city Langfang in Hebei Province (population 1.1mm) is waiving real estate-related taxes in a likely test of support.

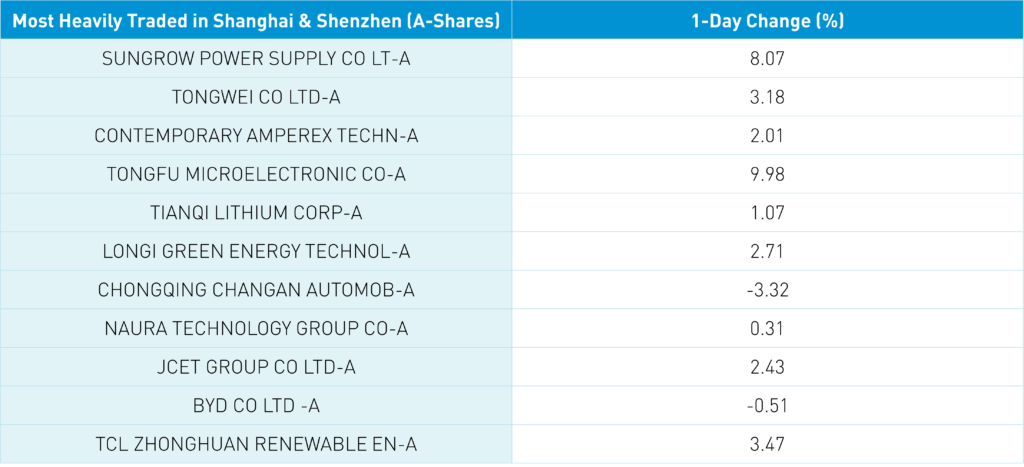

Cleantech plays had a strong day in the Mainland market as evidenced by the most heavily traded stocks by value were Sungrow Power +8.07%, solar company Tongwei +3.18%, battery behemoth CATL +2.01%, semis play TongFu +9.98%, Tianqi Lithium +1.07%, and Longi Green Energy +2.71%. Two key themes for the US and China will be semiconductors and energy independence, with clean technologies playing a big part.

The National Passenger Car Information Exchange Association released July auto data. Passenger vehicle sales increased 40.8% year over year to 2.134mm though off by -2.5% month over month. Top sellers were BYD 162k, SAIC-GM (GM owns 34%) 59k, and Geely 32k, while Tesla sold 28k/-64% MoM from June's 78k. EV retail sales were 486k, which is a YoY increase of 123% though off month over month -1.1%. I do not see this highlighted elsewhere, but pretty cool, right? I need to catch up with our in-house EV expert Anthony!

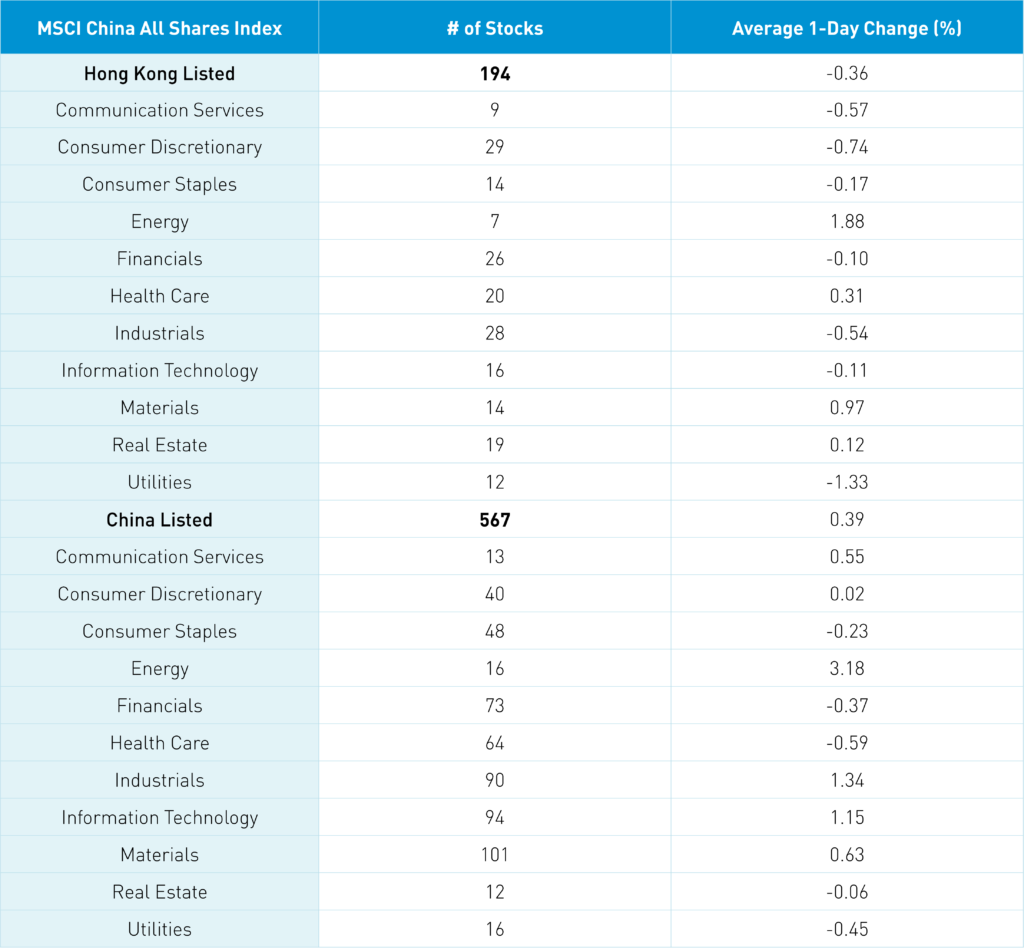

The Hang Seng and Hang Seng Tech fell -0.21% and -0.93% on volume +9.69% from yesterday, which is 61% of the 1-year average. 220 stocks advanced while 243 fell. HK short sale turnover increased 12.53%, 62% of the 1-year average, while short sale turnover accounted for 17% of total turnover. Value factors outperformed growth factors by a small amount as small slightly outperformed large caps. Top sectors were energy +1.88%, materials +0.97% and healthcare +0.31% while utilities -1.33%, discretionary -0.74% and communication -0.57%. The top sub-sectors were coal, property management, and paper stocks, while liquor, education, and power plants were among the worst. Southbound Stock Connect volumes were very light as Mainland investors were small net sellers though Tencent and Tianqi Lithium were net buys. Meituan was a small net sell today.

Shanghai, Shenzhen, and STAR Board gained +0.32%, +0.24%, and +0.85% on volume +0.31% from yesterday, which is 89% of the 1-year average. 1,909 stocks advanced, while 22,534 stocks declined. Growth factors outperformed value factors as large caps outpaced small caps. Top sectors were energy +3.18%, industrials +1.34% and tech +1.15% while healthcare -0.59%, utilities -0.45% and financials -0.37%. The top sub-sectors were semi-related, wind, solar, coal, and lithium, while pork, chicken, and covid drug stocks. Northbound Stock Connect volumes were light as foreign investors sold -$327mm of Mainland stocks today. Shorter maturity Treasuries were off, CNY appreciated +0.02% versus the US $, and copper gained +1.04%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.75 versus 6.76 yesterday

- CNY/EUR 6.90 versus 6.89 yesterday

- Yield on 10-Year Government Bond 2.74% versus 2.74% yesterday

- Yield on 10-Year China Development Bank Bond 2.91% versus 2.90% yesterday

- Copper Price +1.04% overnight