Mainland Market Gets Its Growth Stock on

3 Min. Read Time

Key News

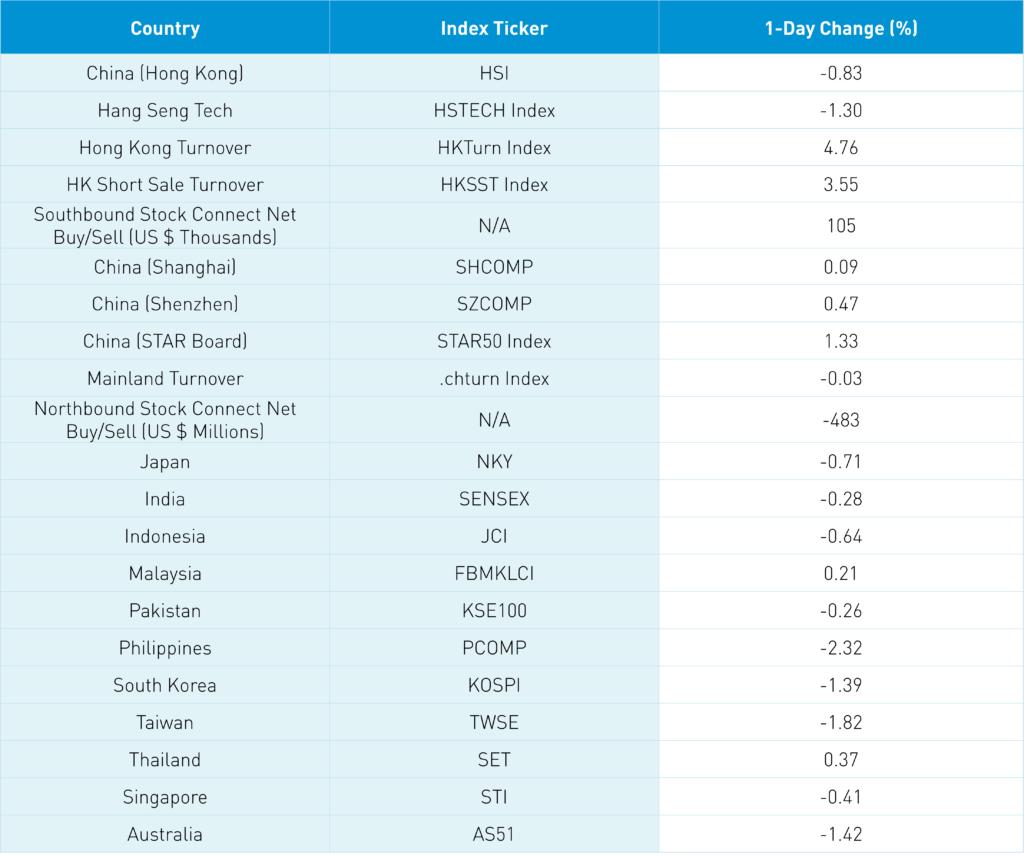

Asian equities had an off day except for China, Malaysia, and Thailand as the Asian currency index posted another 52-week low versus the US dollar. Today was another divergence between onshore China and offshore China. Based on your definition of China, you could have made money or lost it today. The vast majority of China benchmarks have little exposure to onshore China, so you need to get it if you want it. We have advocated pairing onshore and offshore China exposure together.

Mainland China moved higher following President Xi's call for domestic production of key technologies, which lifted Mainland growth stocks with the STAR Board outperforming +1.33%. August import/export numbers were lighter than anticipated as US $ exports rose year over year by +7.1% and imports by +0.3% versus expectations of +13% and +1.1% and July's +18% and +2.3%. In renminbi/CNY, exports rose +11.8% YoY and imports +4.6% versus expectations of +18.5% and +6.3% and July’s +23.9% and +7.4%. Hopefully, the US Fed notices that US imports from China fell by -3.8% in August following July's +11% as it indicates the US economy is slowing as stimulus/free money to buy stuff goes away.

China's exports were largely higher elsewhere, including the European Union (+11% YoY) though I'm not Sherlock Holmes suggesting that they will decline in September. Export data is a key global economic indicator. At the same time, China's imports are a commodity indicator as import volumes increased, but imports' value fell as commodity prices rolled over.

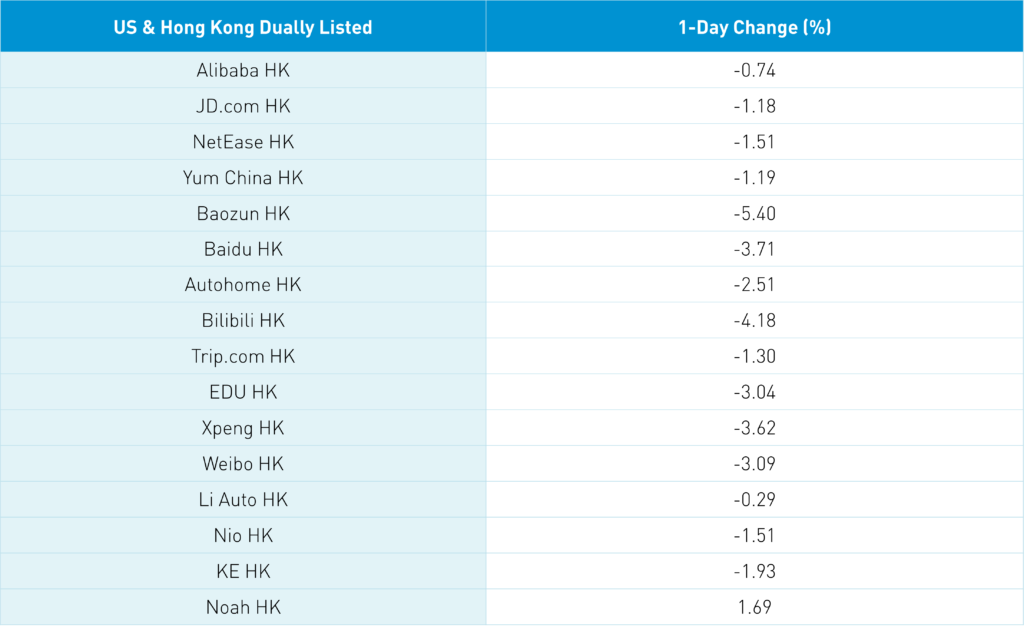

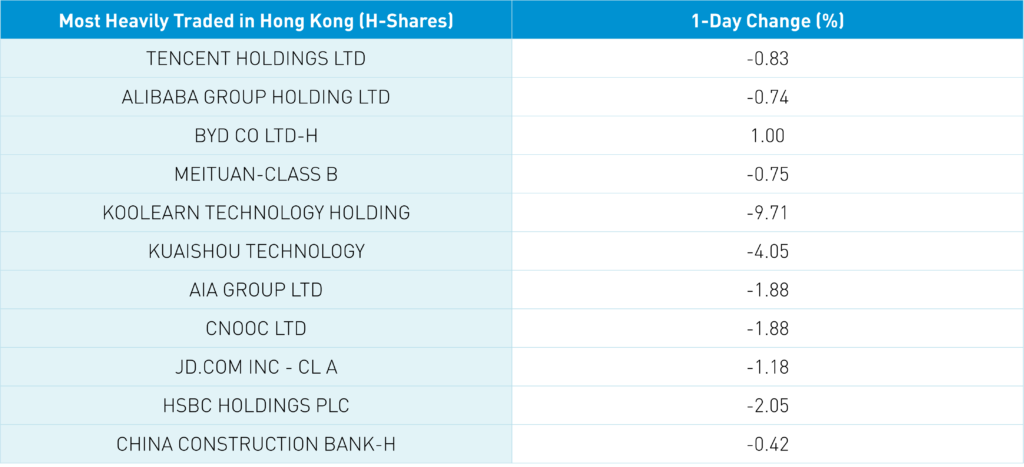

In a pyrrhic victory, Hong Kong didn't fall nearly as far as the US-listed Chinese ADRs yesterday. US ADRs fell on Baidu spin-off IQiyi -13.88% yesterday on revenue sharing with its online users. This appeared to weigh on the Hong Kong share classes of Kuiashou-4.05% and Bilibili HK -4.18%. Other factors yesterday in the US and weighing on Hong Kong include chatter/rumor the Biden administration will expand the Executive Order ban on semiconductor investments, the SEC's mid-afternoon release on Chinese companies switching auditors would be watched, and a member of the House proposing anti-Tik Tok legislation (I assume US tech rivals would love it). I haven't even mentioned lockdowns yet! Yes, Chengdu's 21 million are in lockdown though I recall China's population is 1.4 billion.

Hong Kong's short volume came off a touch while internet names saw mixed short volume today versus yesterday. Another minor pyrrhic victory. Yesterday Hong Kong hosted the hedge fund idea pitch conference called Sohn Hong Kong. Of the six hedge fund managers who spoke in the afternoon, no one mentioned Hong Kong or Chinese stocks! This is an investment conference in Hong Kong! Worth noting the world's largest hedge fund manager said on CNBC that they recommend a China position for geographic diversification. The host almost fell out of her chair as she rattled off the China risks. Yes was the reply, but Chinese equities already embed all that risk! China's interest rate easing makes Chinese equities more compelling, while higher interest rates make US stocks less compelling. Think about it this way: are US stocks more/less compelling as bank interest and bond yields rise? No, because why would I take that risk if you are getting paid more in a bank account? The opposite is happening in China. Throw in valuation metrics, and the China argument only gets stronger. Remember, asset classes, compete with one another! More to come on this, as my colleague Anthony has been working on this. EV maker Nio reported post the Hong Kong close with outlook and EPS loss likely to weigh on the stock.

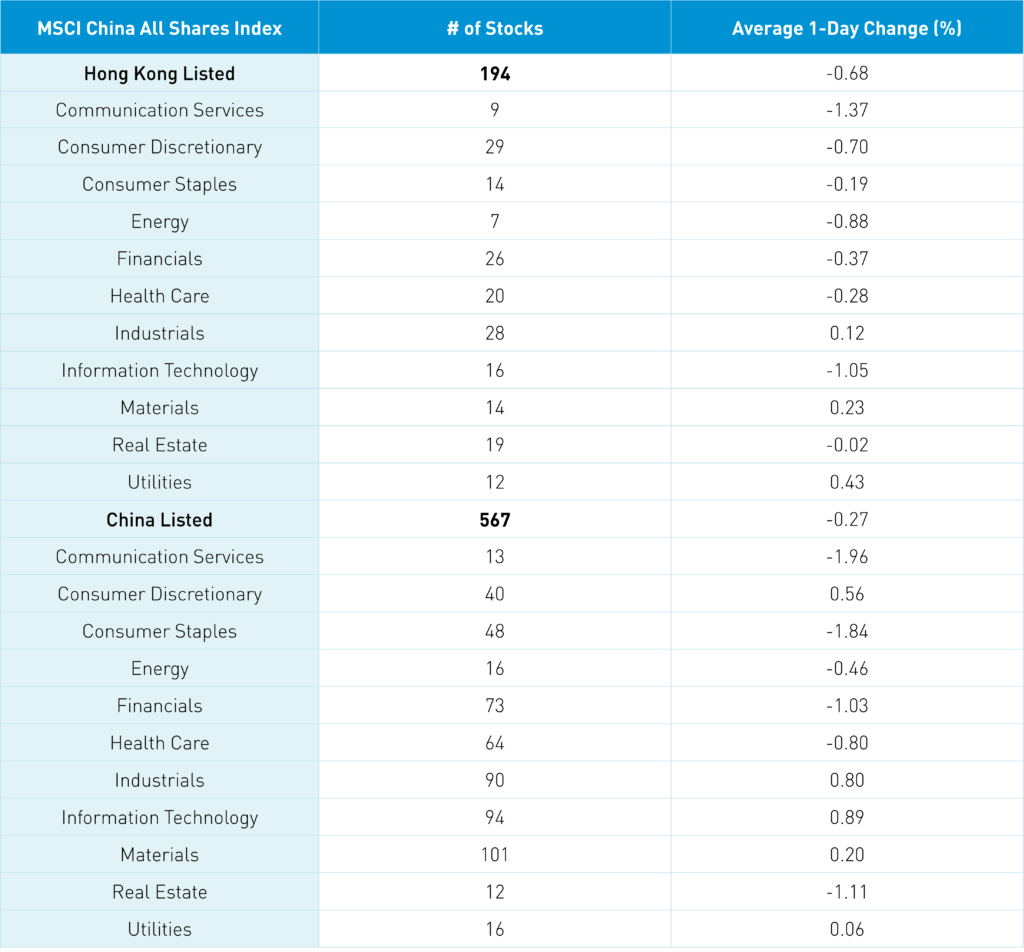

The Hang Seng and Hang Seng Tech fell -0.83% and -1.3% on volume +4.76% from yesterday, 66% of the 1-year average. 153 stocks advanced, while 316 declined. Hong Kong short turnover increased 3.55% from yesterday, 74% of the 1-year average, as short trades accounted for 19% of the total turnover. Value factors outperformed growth factors as large caps outperformed small caps. Top sectors were utilities +0.43%, materials +0.23% and industrials +0.12% while communication -1.37%, tech -1.05% and energy -0.88%. The top sub-sectors were rare earths, power equipment, and nuclear power, while online video, online education, and software were among the worst. Southbound Stock Connect volumes were light as Mainland investors bought $105mm of Hong Kong stocks, with Tencent seeing another moderate buy, Meituan a small net buy for the first time in a long time, and Kuaishou was a moderate sell.

Shanghai, Shenzhen, and STAR Board gained +0.09%, +0.47%, and +1.33% on volume -0.03% from yesterday, which is 84% of the 1-year average. 1,933 stocks advanced while 2,573 stocks declined. Growth factors outperformed value factors today as small caps outperformed large caps. Top sectors were tech +0.86%, industrials +0.77% and discretionary +0.53% while communication -1.99%, staples -1.87% and real estate -1.14%. The top sub-sectors were aluminum, semiconductors, thermal power, and auto parts, while online gaming, Tik Tok ecosystem, and cement were among the worst. Northbound Stock Connect volumes were light as foreign investors sold -$483mm of Mainland stocks. Treasury bonds declined today, as CNY depreciated -0.32% to 6.97 versus the US $ and copper +0.05%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.98 versus 6.96 yesterday

- CNY/EUR 6.91 versus 6.91 yesterday

- Yield on 10-Year Government Bond 2.62% versus 2.61% yesterday

- Yield on 10-Year China Development Bank Bond 2.78% versus 2.78% yesterday

- Copper Price +0.05% overnight