Property Markets Rebound and Tencent Continues Buybacks, Week in Review

2 Min. Read Time

Week in Review

- In this week’s video, Xiabing Su tours Gannan, an autonomous prefecture in southern Gansu Province, where she explores a dream-like landscape hidden within the mountains.

- Asian equities had a mixed week as the Hang Seng and Hang Seng Tech had a down week following further China lockdowns, however, Mainland markets were positive for the week after President Xi's call for domestic production of key technologies.

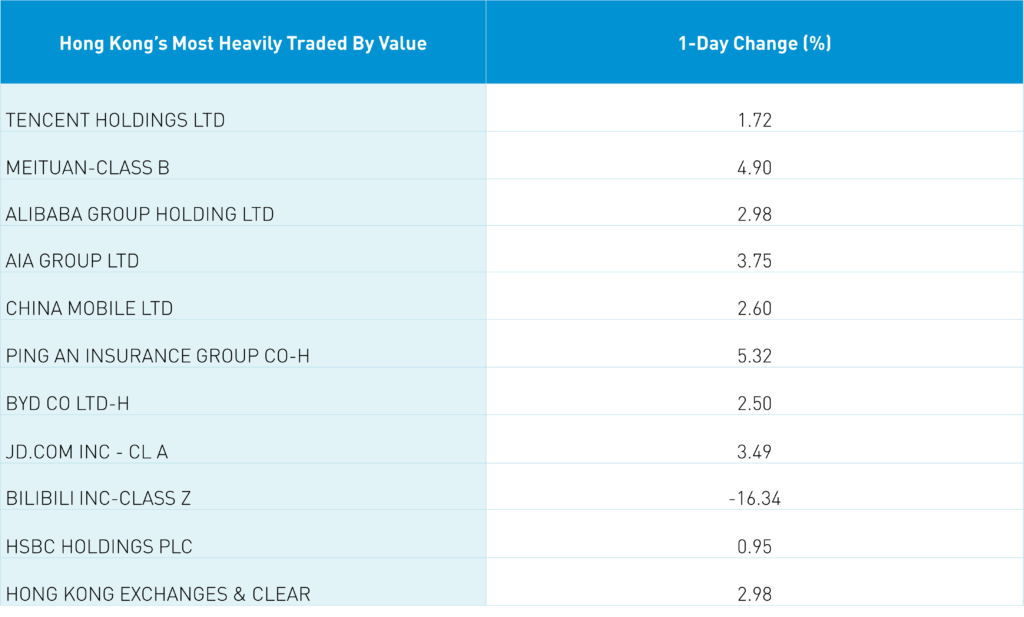

- Tencent had a down week as they had an unknown investor, likely Prosus, who registered to sell $7.6 billion/192 million shares. However, Tencent has continued to buy back 1 million shares a day since August 19th to combat selling pressure.

- Property markets have rebounded on key news of government support which came in response to the lagging of the market as a whole.

Friday's Key News

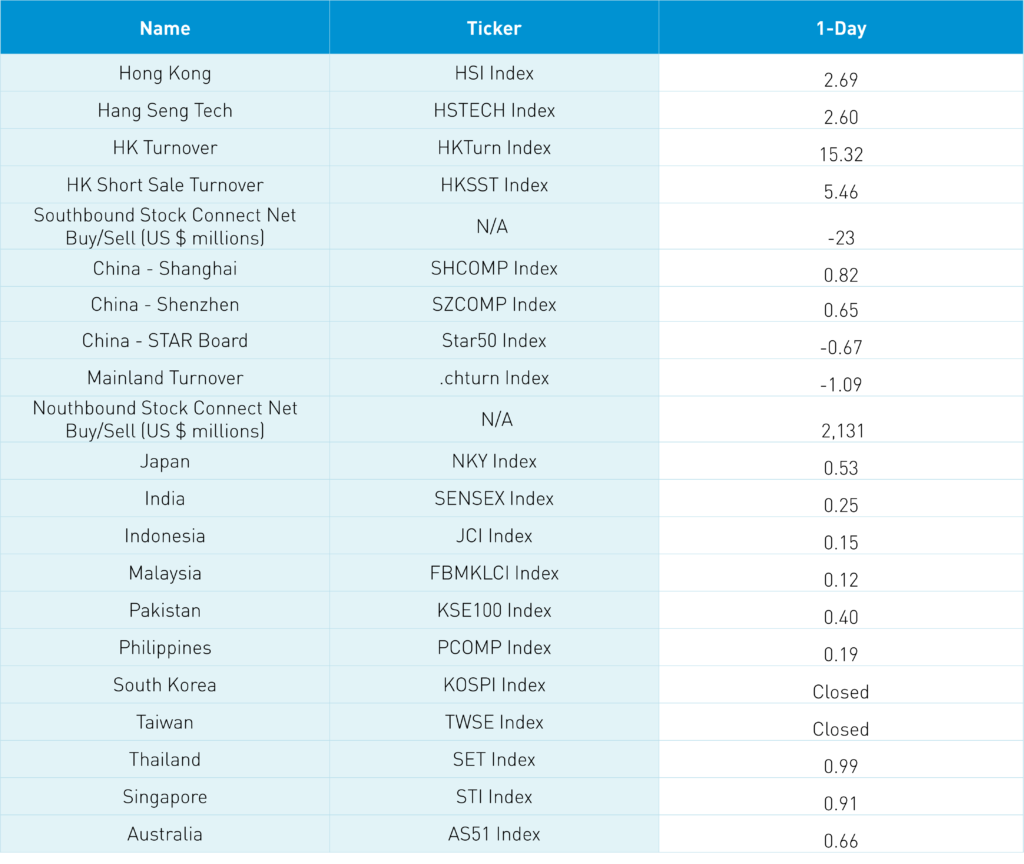

Big move across Asia equities though South Korea and Taiwan equity markets were closed today.

China reported a CPI of 2.5% and a PPI of 2.3% yesterday, weaker than the consensus. The impact of COVID is weighing on demand due to less mobility and frequent testing. The weak inflation could give PBOC more room for further easing. China's money supply M2 YoY growth has picked up to 12.2% in August, while still much lower compared to the 2008 level. The weak data may allow China to further adjust its policy to hedge the economic downside. There has been chatter that China will implement further easing measures but is waiting for the Fed to stop/slow US interest rate hikes to alleviate pressure on CNY. Asia currency index gained +0.37% versus the US $ as CNY gained +0.54% versus the US $ closing at 6.92 from 6.95.

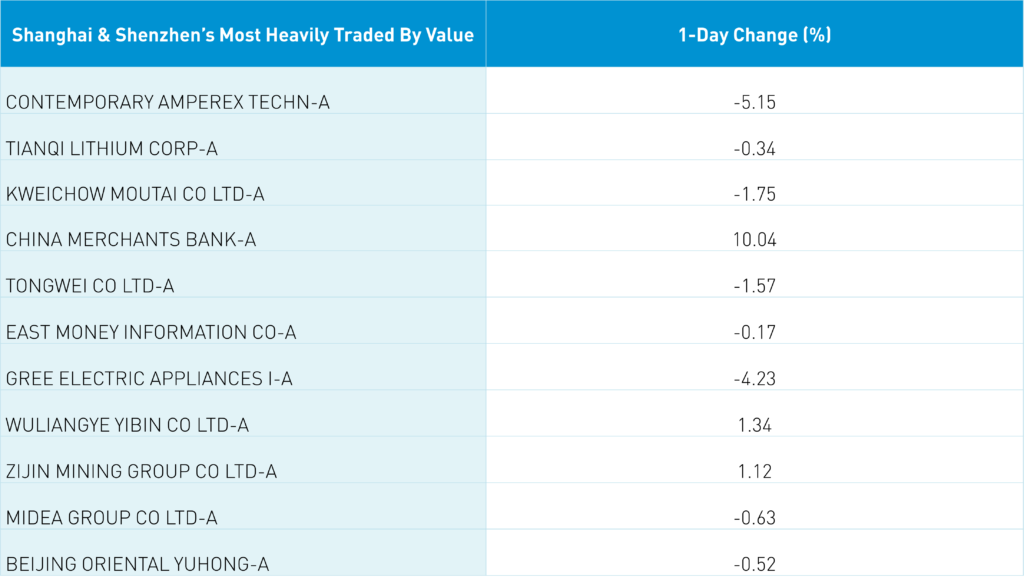

China property stocks were up 3% to 10% across multiple names after Henan local government urged the property developers to guarantee the completion of property projects. Markets are expecting home sales to pick up in the "golden season" of fall. Country Garden (2007 HK) +16.8% stood out after news of a potential issuance of state-backed bonds.

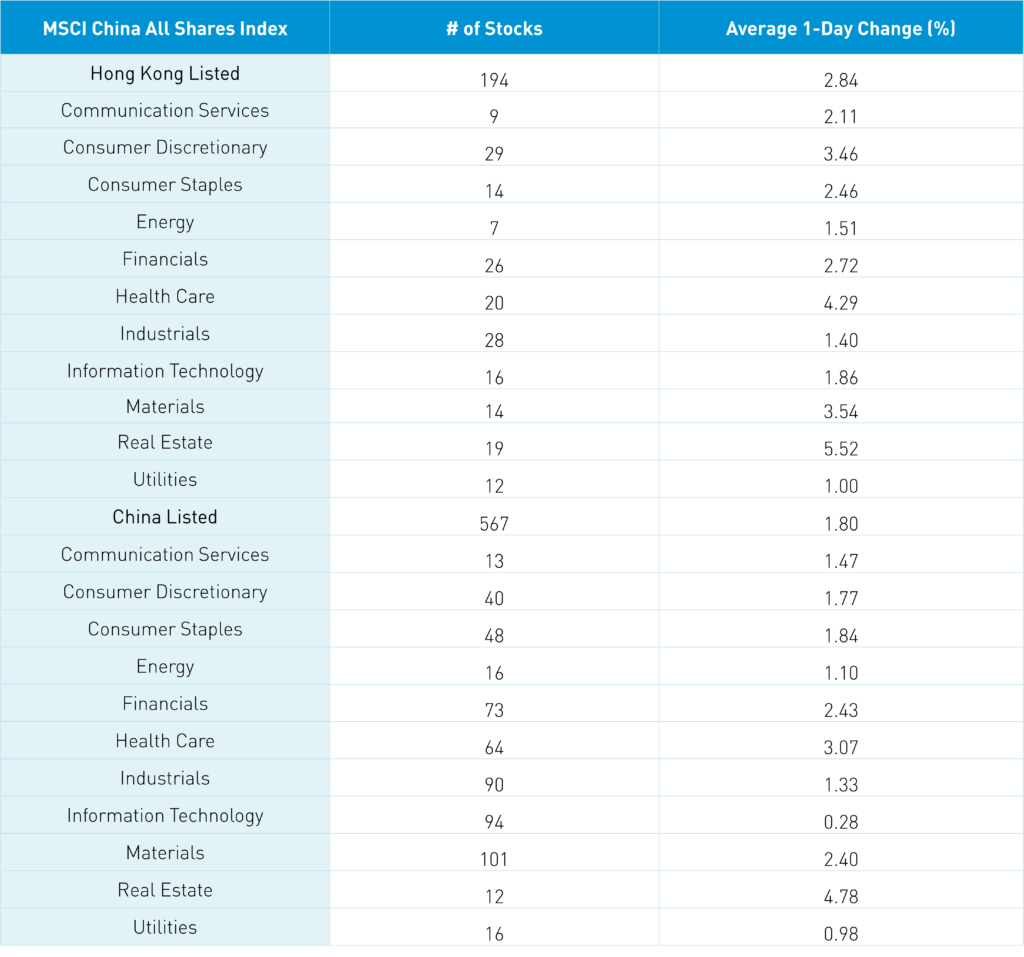

The Hang Seng and Hang Seng Tech gained +2.69% and +2.6% on volume +15.32% from yesterday which is 71% of the 1-year average. 447 stocks advanced with 56 decliners. Hong Kong short sale turnover increased +5.47% from yesterday which is 74% of the 1-year average as short sale trading accounted for 18% of total turnover. Growth and value factors were mixed as small caps outperformed large caps. All sectors were positive with real estate +5.52%, healthcare +4.29%, and materials +3.54% while utilities gained 1%. Top sub-sectors today were biotech, insurance companies, and retailers while semis and online education were among the worst. Southbound Stock Connect volumes were light as Mainland investors sold -$23 million of Hong Kong stocks with Tencent being a moderate buy, Kuiashou and Meituan small buys.

Shanghai, Shenzhen, and STAR Board were mixed +0.82%, +0.65%, and -0.67% respectively on volume -1.09% from yesterday which is 76% of the 1-year average. 2,216 stocks advanced while 2,252 stocks declined. Value factors outperformed growth factors as small caps edged out large caps. All sectors were positive with real estate +4.76%, healthcare +3.05%, and financials +3.05% while tech +0.26%. The top sub-sectors were household products and appliances, healthcare-related, and real estate related while electricity companies, agriculture, and ports were among the worst. Northbound Stock Connect volumes were light/moderate as foreign investors bought $2.131 billion of Mainland stocks today. Treasury bonds were flat, CNY gained +0.54% versus the US $ closing at 6.92 from 6.95, and copper jumped +2.17%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.92 versus 6.96 yesterday

- CNY/EUR 6.98 versus 6.97 yesterday

- Yield on 10-Year Government Bond 2.63% versus 2.63% yesterday

- Yield on 10-Year China Development Bank Bond 2.80% versus 2.79% yesterday

- Copper Price +2.17% overnight