China Economic Data Improves in August, Asian Equities Continue Slide, Week in Review

2 Min. Read Time

| Upcoming Webinar |

| Join us Wednesday, September 21st at 11:00 am EDT for our webinar with WealthShield & Mount Lucas Management: Trend Following and Uncorrelated Assets – A Strategy for Uncertain Times Click here to register. 1 CIMA/CFP credit available. |

Week in Review

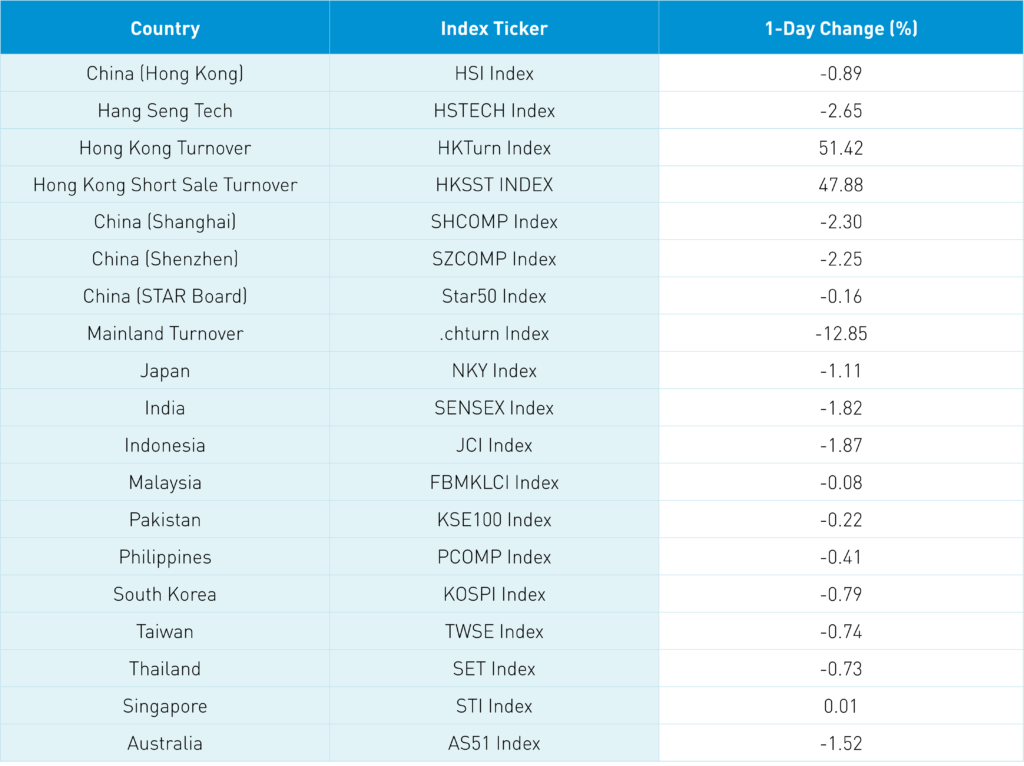

- Asian equities ended a down week mostly lower as fears of further rate hikes from the US Fed after a higher-than-expected US inflation print in August weighed on investor sentiment globally.

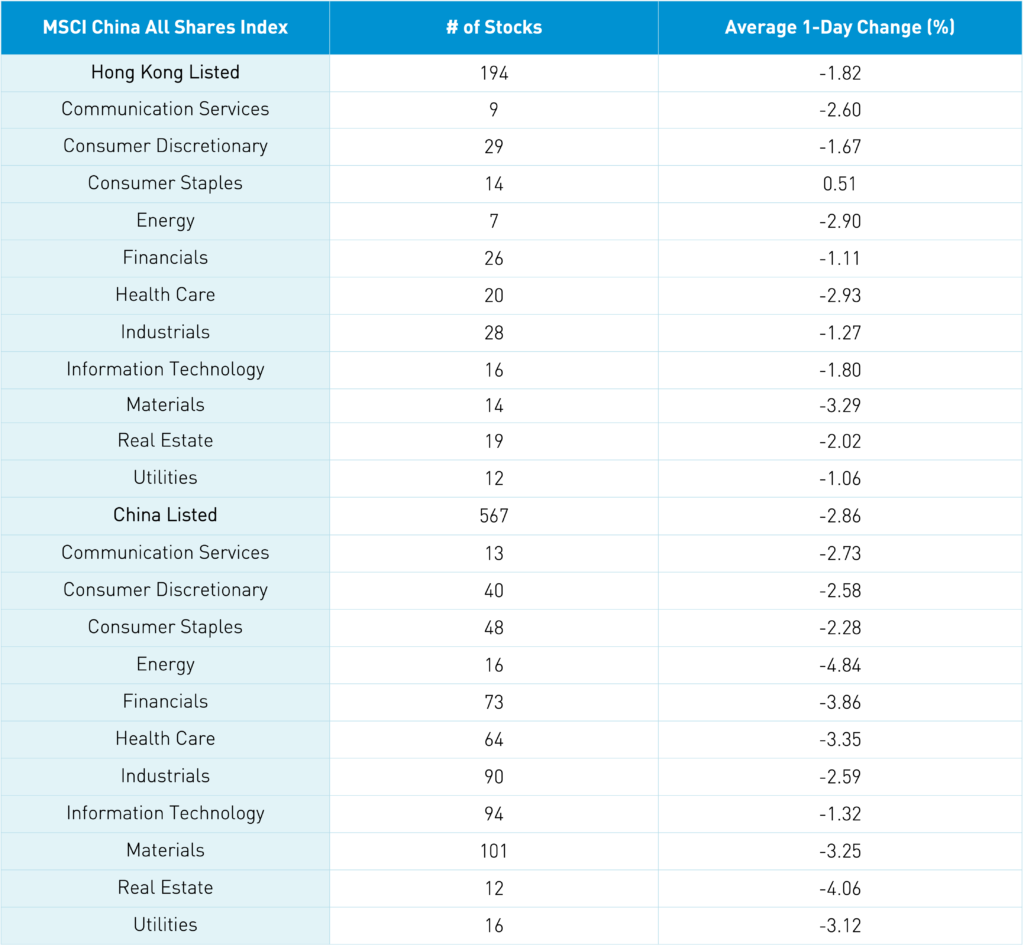

- Hong Kong and Mainland listed biotech stocks were hit hard after the announcement of President Biden’s Cancer Research "Moonshot" initiative on Tuesday, presenting the potential for onshoring contract research that is currently done by Chinese firms.

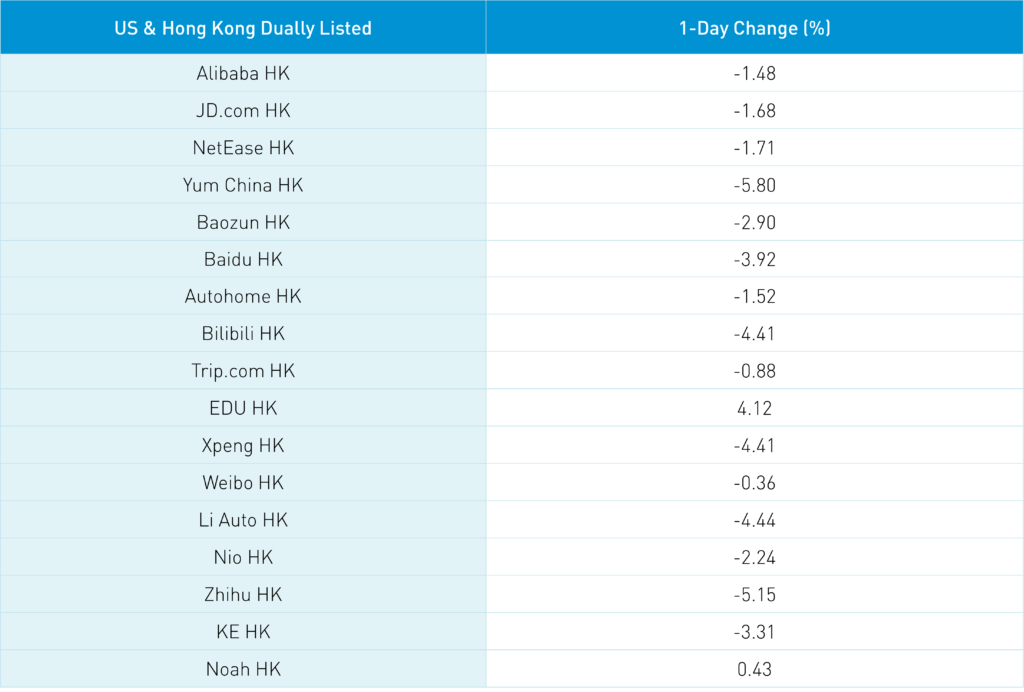

- Tencent and NetEase both confirmed they received 73 new game approvals, further evidence that China’s internet regulatory cycle, as it applies to gaming, may have ended.

- A team from the US Public Company Accounting Oversight Board (PCAOB) arrived in Hong Kong this week to review the audit books of China-based firms listed in the US from the latest financial year.

Friday’s Key News

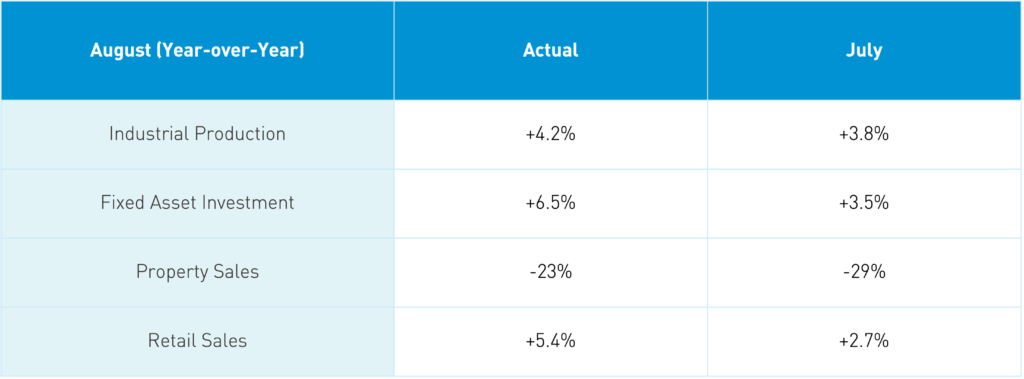

Nearly all major Asian equity indexes were lower overnight despite better-than-expected economic data coming out of China for the month of August.

August economic data was much improved from July, especially retail sales, as China’s consumer economy continued to recover from lockdowns. However, the recent lockdown in Chengdu and travel restrictions for certain areas that are slated to last through October may weigh on retail sales in September. Most notably, property sales saw a marked improvement in August as support for the sector has led to a rebound in equity prices, though today's market action saw real estate lose significant ground.

The city of Zhengzhou, Henan Province, has ordered developers to restart all projects by October 6th. This comes just after a recent emphasis by central government leaders on affordable housing construction.

Auto sales were an impressive element of today’s release, up +15.9% year-over-year as the tax incentive for auto purchases begins to take effect. Electric vehicle sales were up a whopping +104% year-over-year as EV adoption continues unabated after the extension of the tax credit for electric vehicle purchases.

The Renminbi weakened to 7 CNY/USD. The People’s Bank of China (PBOC), China’s central bank, is likely to attempt to stabilize the currency, keeping its value in the upper end of a flexible range. The focus of the PBOC is still stimulus and aid for the domestic market. The country’s depreciating currency reflects slowing overseas demand for exports.

Bytedance's "Pico 4", a virtual reality (VR) headset competitor to Meta’s Oculus, will be launching in stores on September 22nd. Bytedance’s TikTok has been gaining market share from Meta in ads. VR and Metaverse could be another potential space for ByteDance to catch up with its US-based, publicly traded competitor.

The Hang Seng and Hang Seng Tech indexes fell -0.89% and -2.65%, respectively, overnight on volume that increased by +51% from yesterday. Short sale turnover increased by +48% from yesterday. The top performing sectors were consumer staples and utilities, as value factors slightly outperformed growth factors. Meanwhile, the worst performing sectors were energy and health care.

Shanghai, Shenzhen, and the STAR Board fell -2.30%, -2.30%, and -0.16%, respectively, overnight on volume that decreased by -13% from yesterday. The top performing sectors were information technology and consumer staples, as growth factors outperformed value factors. Meanwhile, the worst performing sectors were energy and real estate.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 7.01 versus 6.99 yesterday

- CNY/EUR 6.98 versus 6.98 yesterday

- Yield on 10-Year Government Bond 2.67% versus 2.66% yesterday

- Yield on 10-Year China Development Bank Bond 2.83% versus 2.82% yesterday

- Copper Price -0.45% overnight