US Dollar Weighs on Global Risk Assets, Hong Kong Opens to Visitors, Week in Review

4 Min. Read Time

Week in Review

- The Public Company Accounting Oversight Board (PCAOB) began the process of reviewing the audit books of US-listed Chinese companies on Monday by meeting with PWC and KPMG in Hong Kong.

- The National Development and Reform Commission (NDRC) of China announced new policies to stimulate consumption, offering particularly favorable treatment for big-ticket items such as vehicles, which sent auto names higher on Tuesday.

- Russian leader Vladimir Putin announced the partial mobilization of reserve forces in the country and reiterated the possibility of using nonconventional weapons in Ukraine on Wednesday, which prompted China’s foreign minister to call for a ceasefire.

- Travel booking site Trip.com reported mixed second-quarter results after the US close on Wednesday, though issued a positive outlook on an expected recovery of travel to and within Greater China.

Friday’s Key News

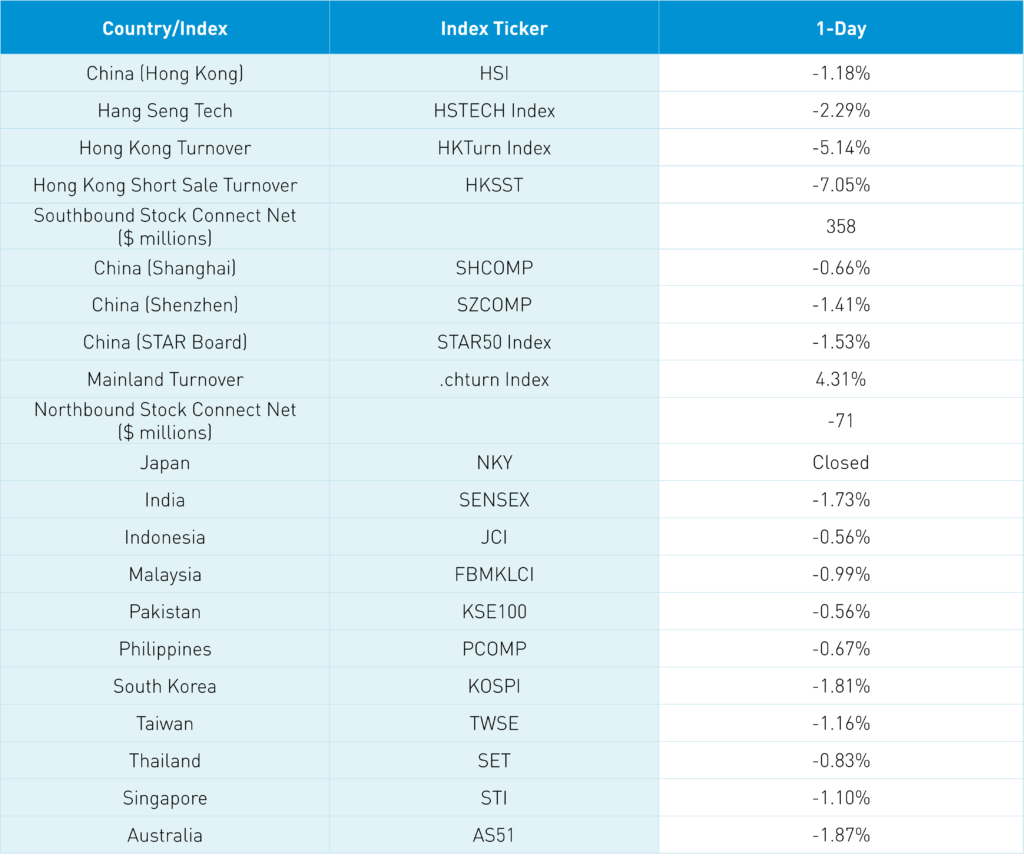

Asian equities ended the week with a thud though Japan was spared due to a market holiday today.

An index of Asian currencies hit a 52-week low for the 5th day in a row as the US dollar index hit a 52-week high for the 5th day in a row. China’s currency declined a further -0.61% versus the US dollar as the exchange rate ended up at 7.12 CNY/USD.

In the late 1990s, I worked for Salomon Brothers Asset Management. We had a great portfolio manager, elder statesmen, and all-around class-act named George Williamson, who started his career at the US Fed before starting to manage money in the early 1970s. George would talk to us youngsters about the 1973 to 1974 bear market and the emotional pain caused by a two-year bear market. George described waking up in the morning knowing the market was going to go down, which made pulling himself out of bed a massive undertaking. I was reminded of this story and George when I noticed that funeral stocks made up one of the only positive subsectors in Hong Kong today! A Mainland China-based financial journalist was in a similar mood when writing about Hong Kong’s decline despite the Hang Seng’s price-to-earnings (P/E) ratio of 8.66, which is “lower than 99% of the past decade”.

Interest rate hikes from the US Fed are making the US dollar a wrecking ball, leading to a risk-off environment globally. A research report noted that over the last three months, emerging market funds have lost more than $10 billion in redemptions, while Europe-focused funds have lost nearly $40 billion. Meanwhile, US equity funds have seen $15 billion in inflows.

We need to remember that Hong Kong has a large structured product or “warrant” market, which makes big round numbers important as breaching these levels forces buying and selling. The Hang Seng Index dipped below 18,000 last night, which created forced selling as structured products with a floor of 18,000 were liquidated.

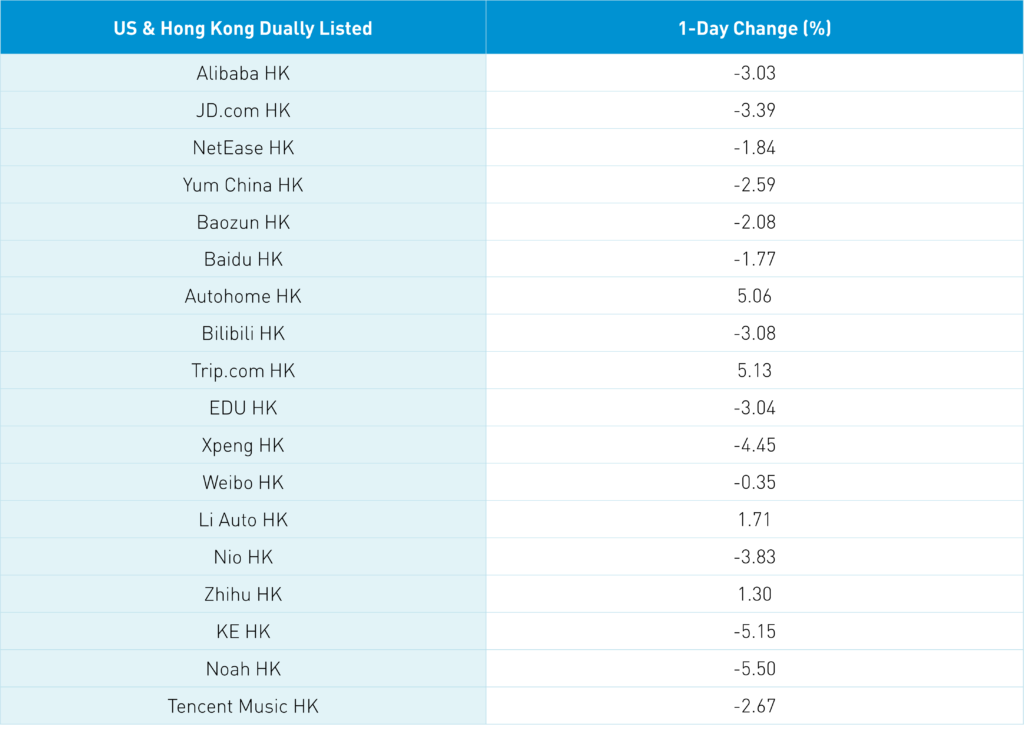

As I have mentioned in the past, we need positive catalysts though the macroeconomic environment remains a challenge. News that Hong Kong will remove the visitor quarantine requirement next week helped Trip.com HK to gain +5.13% along with gains in other tourism plays such as airlines and hotel chains. This is another example of China’s zero COVID policy being watered down.

Hong Kong-listed China internet stocks were off as short sellers pressed their bets again. 39% of JD.com’s total trading was short! Yes,0 we had the PCAOB Chair stating the necessity of full access to China audits, but I take this as a positive. No one wants to go down in history as a modern-day version of Smoot and Hawley, which is what an ADR delisting would be.

Mainland stocks were off on little news as the Shanghai Composite closed below 3,100. The market’s poor mood should be noticed by policymakers as markets. It could be time to press on the policy gas pedal!

I have been on a Malcolm Gladwell kick recently as I loved David and Goliath though Talking to Strangers might be my favorite.

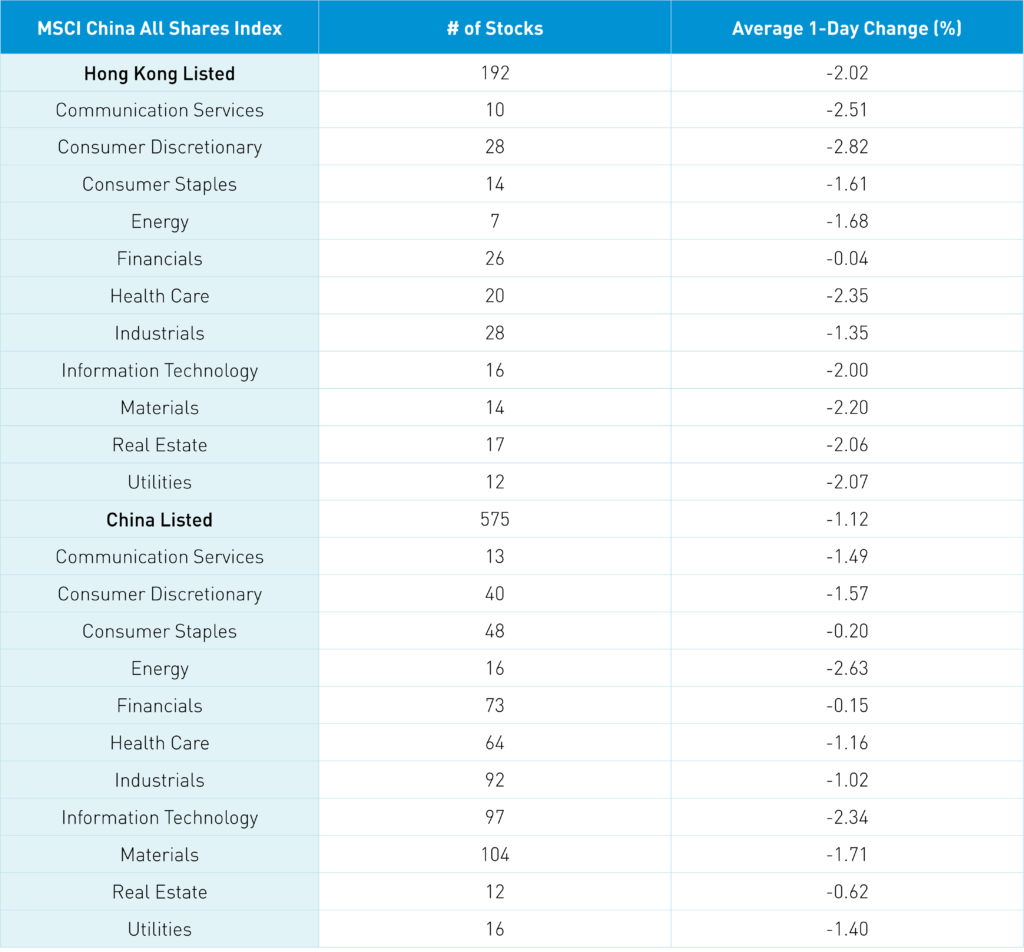

The Hang Seng and Hang Seng Tech indexes fell -1.18% and -2.29%, respectively, on volume that decreased -5.14% from yesterday, which is 64% of the 1-year average. 72 stocks advanced while 415 declined. Mainboard short sale turnover declined -7.05% from yesterday, which is 73% of the 1-year average, as short trading accounted for 20% of total trading. Value factors outperformed growth factors as large caps “outperformed” small caps. All sectors were negative as consumer discretionary fell -2.82%, communication services fell -2.51% and healthcare fell -2.35%. The top-performing subsectors included telecom, funeral stocks, banks, and oil. Meanwhile, e-cigarette/tobacco, retailers, software, and plastic surgery stocks were among the worst. Southbound Stock Connect volumes were light as Mainland investors bought $358 million worth of Hong Kong stocks as Tencent was a strong/moderate buy, China Mobile was a strong buy, Meituan was a small sell, and Li Auto was a very small net buy.

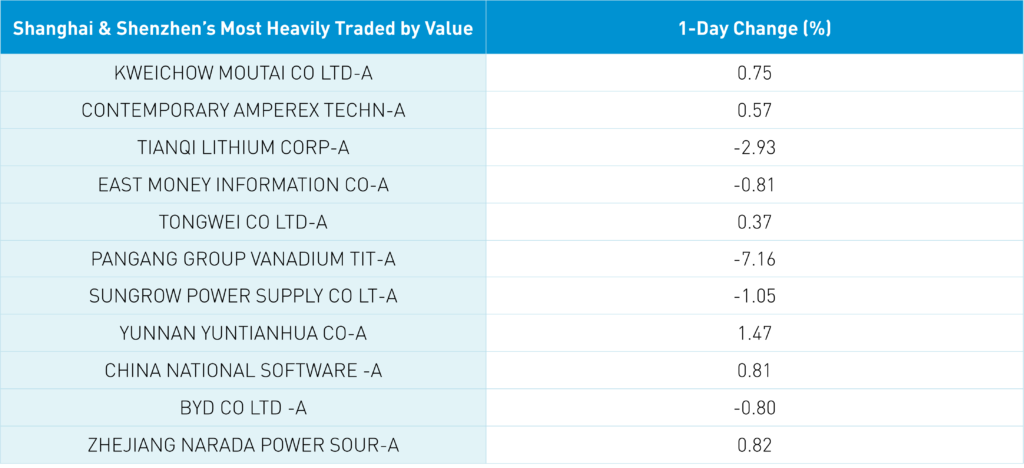

Shanghai, Shenzhen, and the STAR Board were off -0.66%, -1.41%, and -1.53%, respectively, on volume that increased +4.31% from yesterday, which is 66% of the 1-year average. 581 stocks advanced while 4,007 stocks declined. All sectors were down as energy fell -2.63%, technology fell -2.34%, and materials fell -1.7%. The top-performing subsectors included insurance, banks, and liquor stocks. Meanwhile, ports/shipping, education, and coal were among the worst. Northbound Stock Connect volumes were moderate/light as foreign investors sold -$71 million worth of Mainland stocks. Treasury bonds sold off, CNY declined -0.61% to 7.12 CNY/USD, and copper gained +0.22%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 7.12 versus 7.08 yesterday

- CNY/EUR 6.95 versus 6.95 yesterday

- Yield on 1-Day Government Bond 1.03% versus 0.98% yesterday

- Yield on 10-Year Government Bond 2.68% versus 2.65% yesterday

- Yield on 10-Year China Development Bank Bond 2.83% versus 2.80% yesterday

- Copper Price +0.22% overnight